As small modular reactors (SMRs) move from concept to commercialisation, one of the least visible yet most critical enablers of deployment is insurance. Property and liability coverage for nuclear are not only a financial safeguard, they are also a regulatory requirement. However, nuclear insurance is highly specialised, capacity constrained, and dependent on early engagement with underwriters.

Insurance requirements for SMRs and microreactors may vary based on reactor size, design, fuel forms, coolant types, and power levels. Existing regulatory frameworks establish baseline liability and financial protection requirements, but these were developed for large, traditional light water reactors. As a result, regulators and insurers may apply a more risk-informed approach when determining appropriate insurance levels for smaller or non-traditional designs.

The US liability insurance framework

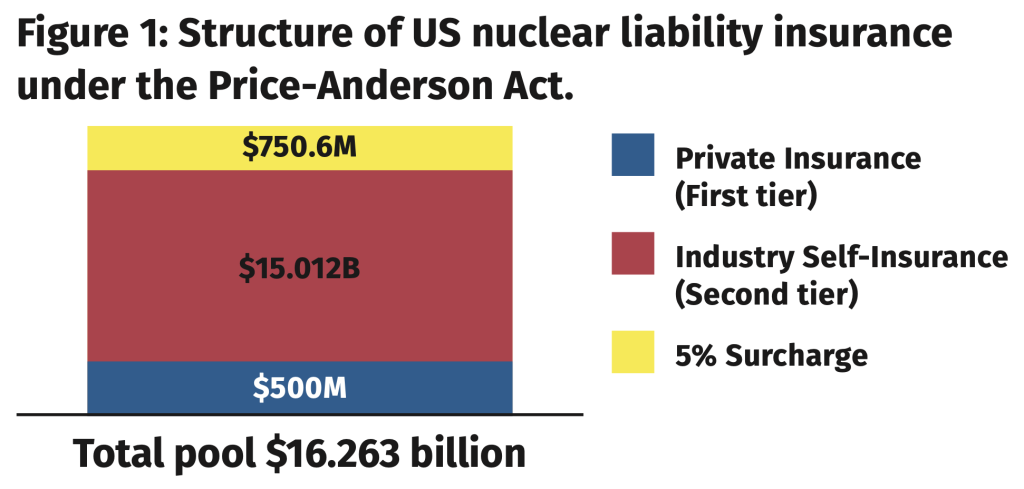

In the United States, nuclear liability insurance is governed by the Price-Anderson Act, a federal programme designed to ensure compensation to the public following a nuclear incident. The Act establishes a two-tier structure.

Primary layer: Each reactor operator must carry the maximum available private insurance, currently approximately $500m per reactor site. This coverage is provided through the American Nuclear Insurers (ANI) pool.

Secondary layer: In the event of a major incident, all US reactor operators contribute to an industry-wide retrospective pool, with potential contributions of up to approximately $158 m per reactor. This brings total available liability protection to more than $16bn per incident.

This framework is designed to cover third-party claims for bodily injury, property damage, and certain environmental losses, while providing a predictable compensation mechanism. For SMRs, which may involve new ownership models, siting approaches, and supply chains, aligning these coverages with regulatory expectations may present additional challenges.

In addition to the Price-Anderson Act, Nuclear Regulatory Commission (NRC) regulations in 10 CFR Part 140 establish detailed financial protection requirements based on reactor size and operating status. These regulations differentiate between nuclear power plants with a rated capacity of 100 MWe or greater and those with lower electrical output, a distinction that is particularly relevant for small modular reactors (SMRs) and microreactors. For smaller units, required liability coverage may be reduced or determined on a case-specific basis, reflecting their lower potential risk profile. The regulations also include provisions for multiple reactors located at a single site. This allows the NRC to evaluate financial protection requirements on a site-specific basis. This introduces additional flexibility for SMR deployments but also creates complexity in structuring appropriate liability coverage for multi-unit configurations.

Building on this framework, the NRC’s proposed rulemaking for microreactors under 10 CFR Part 57 further reinforces a risk-informed approach to financial protection. The proposal recognises that microreactors and other reactors with comparable risk profiles may present substantially lower radiological risks than traditional large reactors and therefore may warrant reduced levels of required liability coverage. Under this approach, the NRC would retain discretion to determine appropriate financial protection requirements on a case-by-case basis, considering factors such as the type, size, location, and hazard profile of the facility, as well as the availability and cost of private insurance. The rulemaking also contemplates the potential for reduced indemnification obligations for certain licensees, aligning Price-Anderson financial protection requirements more closely with the actual risks posed by advanced reactor designs.

Additional nuclear insurance

Unlike liability insurance, which protects the public, nuclear property insurance focuses on the facility itself. Coverage typically includes physical damage to the plant, equipment, and infrastructure, as well as stabilisation, decontamination, and recovery costs following an incident. In the United States, reactor licensees are generally required to maintain approximately $1.06bn in onsite property insurance per reactor site. This coverage is provided by Nuclear Electric Insurance Limited (NEIL), a mutual insurer specialising in nuclear risks.

Globally, nuclear liability is governed by a set of international conventions, including the Convention on Supplementary Compensation for Nuclear Damage (CSC), the Paris Convention and Brussels Supplementary Convention, and the Vienna Convention and Joint Protocol. While implementation varies by jurisdiction, these frameworks share core principles: liability is channelled exclusively to the operator, with liability caps supplemented by public funds.

For SMR developers pursuing international deployment, this creates a jurisdiction-by-jurisdiction insurance strategy that often requires coordination across multiple national insurance regimes.

Most countries maintain domestic nuclear insurance pools that provide or coordinate coverage within their jurisdictions. Examples include Nuclear Risk Insurers (UK), Assuratome (France), Deutsche Kernreaktor-Versicherungsgemeinschaft (Germany), and the Japan Atomic Energy Insurance Pool.

Because no single national pool can absorb the full risk of a nuclear accident, these entities participate in international reinsurance arrangements and reciprocal risk-sharing agreements with other pools and a limited number of specialist reinsurers. Coverage typically includes physical damage, as well as decontamination and stabilisation costs.

A constrained market and specialised brokerage

Existing insurance frameworks were developed for large, traditional reactors, creating added complexity for SMR deployment. Unlike conventional insurance markets, nuclear insurance is provided by a small number of highly specialised pools and mutual insurers. Global underwriting capacity is limited, and participation is tightly controlled.

This dynamic is particularly relevant for SMRs, as developers may pursue multi-unit deployments, novel reactor designs, or non-traditional ownership structures – all of which introduce new risks from an underwriting perspective. In practice, access to insurance capacity – not reactor design – may become a gating factor for deployment. Given the complexity of the nuclear insurance market, engaging a broker with demonstrated experience in nuclear insurance is essential. Nuclear insurance is not transacted in a broad, competitive marketplace; rather, it is concentrated among a small number of insurers each with distinct underwriting requirements and processes.

An experienced broker can facilitate early engagement with these markets, advise on appropriate coverage structures, and help align project risk profiles with underwriting expectations. They are also better positioned to anticipate capacity constraints, identify potential coverage gaps, and structure placements that satisfy both regulatory requirements and lender expectations. For SMR and microreactor developers, these capabilities are particularly important. Emerging technologies, multi-unit deployment strategies, and evolving regulatory frameworks introduce uncertainties that must be translated into insurable risk. Without specialised expertise, projects may face delays, higher costs, or challenges in securing adequate coverage.

The critical role of early engagement

Insurance cannot be treated as an afterthought. Developers who engage with brokers and underwriters early in the project lifecycle are better positioned to validate the insurability of their designs and align engineering, safety, and risk management decisions with market expectations. This approach helps avoid late-stage surprises that could delay licensing or financing.

Delayed engagement with insurance markets can expose developers to significant risks, including coverage exclusions, insufficient limits, or, in extreme cases, an inability to secure required insurance. Coverage is not guaranteed to be available in the necessary amount, form, or timeframe. As the SMR market grows, competition for limited insurance capacity is likely to intensify.

Insurance has historically been a key enabler of nuclear energy, providing financial assurance necessary for public acceptance and private investment. For SMRs, it will play an equally pivotal role.

For developers, early engagement with nuclear insurance brokers, designing for insurability, and planning for constrained capacity will be critical. In the race to deploy the next generation of nuclear technology, those who treat insurance as a strategic priority rather than a compliance exercise will have a decisive advantage.