We’ve long been promised a nuclear renaissance. And now it seems to have finally arrived. The reasons for this shift in public opinion will be familiar. In April 2025, Europe experienced its most serious and extensive power cut in decades, leaving millions of people in Spain and Portugal without electricity. With the cause still largely unexplained, attention has naturally turned towards the grid and its ability to cope with a range of different challenges that will emerge as significant influences in the near future, not least climate change and the ongoing electrification of society.

But there’s another, arguably more pressing challenge on the horizon: highly power-hungry AI. It’s well known the high-density server racking required for this type of computing demands far more energy to keep data halls cool. Yet grid infrastructure is unable to keep pace with the industry’s seemingly unlimited growth, leaving almost everyone open to a world in which access to secure and reliable power is far from guaranteed.

Given this situation, it’s unsurprising to find governments touting small modular reactors (SMRs) as a route forward. The UK government, for example, has announced plans for a ‘large nuclear expansion’, calling on tech firms to support the development of SMRs to help meet the huge demand AI has and will place on the country’s aging transmission network.

This is a strategy of reinvention – it’s about taking a technology born of the 20th century and reimaging it for an industry very much tied to the 21st. Given there is already a great deal of development taking place within this space, many of these plans seem odds on for success.

Reaching this point, however, will require much closer collaboration with manufacturers that have existing knowledge of nuclear engineering and critical service in general. This is especially true given that delivery times, timely qualification and public safety remain important issues on the way to full-scale deployment.

Nascent signs of success

One of the most pressing challenges in the current SMR market is its lack of maturity. With around 100 SMR designs currently in development – each employing different reactor types and cooling methods – the sector is marked out by innovation but also fragmentation. While this level of activity is encouraging, it also highlights a critical absence of standardisation that will be vital to making SMRs economically viable.

Standardisation isn’t just a financial concern. It’s central to the original appeal of SMRs: flexibility and accessibility. Modular designs are ‘pilotable’ and therefore have the potential to bring nuclear energy to locations where traditional, large-scale plants would be too expensive or impractical. Some even envision SMRs being deployed as temporary or emergency power sources, supporting regional growth or serving crisis response efforts. But without a dependable, scalable design, many of these use cases remain out of reach.

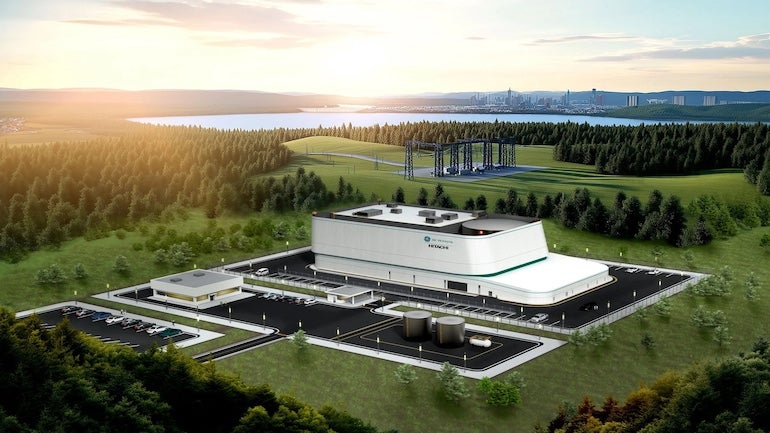

Despite the lack of a unified standard, there are encouraging developments. GE Vernova Hitachi’s BWRX-300, for instance, is a promising 300 MW water-cooled reactor based on the company’s previously licensed Economic Simplified Boiling Water Reactor (ESBWR). Built on existing technology and infrastructure, the BWRX-300 includes design optimisations, such as fewer safety relief valves and increased design pressure. The first prototype for this design will be built in Canada and could be operational before 2030, well ahead of the mid-2030s timelines projected for many competing designs.

Rolls-Royce SMR is another design based on existing reactor technology which shows how crucial commercial awareness is key to SMR success. As the company’s chief executive Tufan Erginbilgiç points out, however, standardisation will only be possible with the right suppliers in place, in part because of the time it typically takes for projects of this type to get up and running successfully. Established suppliers with a history in the industry will be essential in this respect – not only to eliminate manufacturing bottlenecks but also to comply with the qualification and nuclear quality control of the products, as well as to ensure economies of scale, repeatability and a quick time to market.

Even with these concerns, Rolls Royce’s SMR is projected to cost roughly £1.8bn (US$2.4bn) per unit – a significant reduction compared to the estimated £9bn (US$12bn) price tag for a single PWR unit such as the one planned at Sizewell C in the UK. Whether that projection can be met won’t be known until the design completes a Generic Design Assessment process and is constructed. The design is currently in Step 3 of the UK GDA and the first unit is planned for the Wylfa site on Anglesey in Wales with this first unit expected to become operational in the early 2030s.

Appeasing all parties

The complex regulatory landscape around SMRs is difficult to ignore. Licenses are required for both design and operation – affecting both vendors and end users, often based in different countries with varying requirements.

With many SMR designs in development, licensing has become a slow and daunting process – in part because regulators are unfamiliar with new reactor types and manufacturing methods. While some of the more mature SMR designs use established coolants like pressurised water, others rely on less conventional options like liquid metal, helium, or molten salts. Any deviation from approved technologies – that is, those known to regulatory agencies – will require rigorous safety and validation ahead of use.

This caution is entirely justified. Public confidence is essential to the industry’s lasting success, especially as SMRs are expected to bring nuclear power closer to where people live and work. Here the success of small reactors on nuclear-powered submarines provides some useful context. The reactors that sit aboard these vessels are situated close to crews and have arguably been the most prominent example of the industry’s success since the fission was first discovered. If the timeline for SMR deployment is to appease investors, regulatory agencies and the general public, it makes sense to choose suppliers that have demonstrable success in this area. It will accelerate delivery but also signal that relevant expertise is being exploited at every level.

Still, cross-border regulation remains a major hurdle. To address this, the IAEA launched the Nuclear Harmonisation and Standardisation Initiative in 2022. Its goal is to streamline international deployment by aligning regulatory standards and construction codes, including acceptance of factory-built components – a move akin to practices seen in aviation and shipping.

Harmonisation in nuclear could significantly reduce costs by enabling parts to be licensed and produced globally. However, it raises new legal and logistical challenges. Modular builds and shared standards will require scrutiny – especially regarding liability for transportable plants and the application of environmental and public participation laws.

Taking what’s known to work

Given the lengthy regulatory process – even for advanced projects – it makes sense to choose proven solutions. This not only helps validate the SMR concept but also offers a reliable way to power new industries, like AI, without risking a shortfall.

Valves and flow control elements are a case in point. Though a small element within an overall build, they’re essential for keeping SMRs within safe operating limits and are critical safety components. Many of these products have already been approved for large-scale reactors and while not directly transferable to SMRs, they bring thousands of hours of proven performance in critical service. This eases the regulatory concerns around bespoke parts. This is especially relevant to SMRs’ passive safety systems, which lower the operational threshold for newer players.

That said, no part can bypass the rigorous testing that defines nuclear safety. Every component must meet the same high standards. Still, if speed and simplicity are key to SMR adoption, it makes sense to work with companies with significant experience in existing nuclear plants. It’s one piece of a complex puzzle – but vital for making ambitious SMR plans become a reality.