Nuclear new-build: costs

Trouble on the horizon

21 January 2011On the surface, the UK’s nuclear new build programme has a serene inevitability about it. But rising construction costs and low and volatile electricity prices are indications that plenty could go wrong. By Tony Roulstone

The plans for new nuclear in the UK are advancing. With the support of the UK government, EDF (with Centrica) is pushing ahead with the preparations to construct four new large pressurised water reactors (EPRs) at Hinkley Point and Sizewell. Also, the German consortium of E.On and RWE (through their joint venture—Horizon Nuclear Power) are following, perhaps with less gusto, a similar path but a few years behind with the aim of constructing 6GWe of new nuclear capacity. These two projects would leave the UK with over 13 GWe of nuclear capacity in 2030 after all the Magnox and AGRs have closed down.

In recent years, the government has acted on a number of fronts to facilitate new build: integrating and streamlining design licensing; setting up a structure for waste and decommissioning costs and changing the process of planning for large infrastructure projects such as nuclear power. The new coalition government has taken a broadly similar position. Most importantly, it has reiterated that there will be no ‘public funds or public subsidy’ for nuclear.

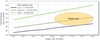

There are indications that plenty could go wrong. Evidence is emerging of rising costs of construction (see Figure 1). Also, there is concern about the electricity price’s volatility and low price. Wholesale electricity prices reached a peak of almost GBP 100/MWh in September 2008. Since then have been below GBP 40/MWh for much of 2009 and 2010.

The behaviour of the electricity market is the result of its design compounded by the effects of multiple overlapping mechanisms put in place during the last 10 or more years. Unless there is wholesale reform of the electricity market, it seems unlikely that any new generation-dependent high capital cost, such as nuclear power, will be built. Capacity margins would be squeezed and new gas- fired generators built (see also pp10-11). This would be cleaner than coal, but still polluting, and would increase dependence on imported gas. It would leave the government’s energy policy in tatters.

(At a suppliers’ forum in September, EDF confirmed that it had not yet made a commercial decision on whether to proceed with the first UK EPR project at Hinkley Point, Somerset. Humphrey Cadoux-Hudson, managing director of the utility's nuclear new-build organisation, said: “It would be ridiculous to make a decision before putting into place market reforms...that we need to make sure that the market works properly as we develop low-carbon energy in the UK.”)

Capital costs are rising

The energy review of 2006 established the economic case for new nuclear construction used costing data collected in the early part of the decade. This data was drawn from a range of sources, but was consistent with the overnight capital costs (that is, excluding interest during construction) of reactors such as those from Westinghouse and Areva being GBP 1400/kWe.

One of the prime sources was the MIT study ‘The Future of Nuclear Power’ (2003) which looked at worldwide experience of nuclear construction unit costs, did not take an overly optimistic view, and arrived at an estimate of $2000/kWe. When that paper was updated in 2009, it noted that worldwide construction costs had risen sharply [1]. Based on a 2007 prices, unit construction costs had doubled to $4000/kWe. It identified three main causes:

- Worldwide cost inflation of specialist components including vessels and forgings

- Increases in the price of materials such as steel and concrete

- Delays in construction of current European projects in Finland and in France.

Overnight capital cost estimates for reactors in Europe, the USA, Japan and Korea are in Fig. 1. From it a number of points are clear:

- None of the Western reactor projects are achieving the energy review target figure for overnight unit capital costs of GBP 1400/kWe

- Only some of the Japanese BWRs and the recent Korean PWRs come close

- BWRs are cheaper to build than PWRs, except for the Korean designs where costs are mature

- Some of the US new build programme (PWRs) have unit capital costs above GBP 2700/kWe

- The trend of Korean reactor costs (decreasing at GBP 40 per year) shows what can be achieved by a long-term focus on cost, which is possible with a series of a standard designs being built.

The investment decision for nuclear is complex, particularly because few nuclear power stations have been built in the west in recent years and any new nuclear power stations in the UK will be financed by the utilities involved employing their own funds. Investment considerations include capital, fuel, operating, waste and decommissioning costs over the life of the plant, which will be in excess of 40 years. High availability of the station is important because it determines the overall power in output and hence the revenue that is generated. The high capital element in nuclear also increases the emphasis of the effective cost of capital and equity discount rate for the project.

Taking all of these factors into account, Figure 2 sets out the average lifetime electricity price required for a specified equity rate of return and for three levels of capital cost—based on the mature build costs of the type of reactors to be built in Europe. This analysis shows that for equity discount rates in the range 10-12%, utilities will require electricity prices to be above GBP 50/MWh for the overnight capital cost of GBP 2200/kWe and perhaps as high as GBP 82/MWh for high capital costs such as those associated with the first in a series of construction.

Looking at the most recent information about costs of the two designs that are being licensed for construction in the UK, we can identify the price level that the utilities EDF/Centrica and Horizon will require, based on the EPR, the costs of the plant being built at Flamanville and on US capital costs for AP1000 (which as they are published for regulatory purposes, may be somewhat high).

The figures shown in Table 1 are mature capital costs and may be representative of the second or third of a series build in the UK, but the first-of-a-kind built here will have large extra costs for special equipment, training and local learning. Based on a programme of four reactors with the first costing up to 40% more than the repeat build unit cost of GBP 2000/kWe, the long-term mean electricity price needs to be above GBP 60/MWh for an EPR-based programme to be viable.

Making a decision

Utilities will make their investment decision based on a range of factors including their expectation of the future electricity prices. Current wholesale prices for electricity are about, or in some cases, below GBP 40/MWh. Therefore an investor in nuclear must expect the long-term price to rise by about GBP 20/MWh. Electricity prices may be increased either by the effect of long-term trends in gas prices or carbon pricing.

Based on its energy reviews, the former government expected that the trading of carbon permits under the EU emissions trading scheme (ETS) would drive up electricity costs for the coal and gas generators. However, the EU scheme operates in five-year periods of time, which is much shorter than the longer investment horizons of nuclear, and to date, the scheme has not been effective in significantly increasing either carbon or electricity prices. The recent traded carbon price is about EUR 15/tonne CO2. Based on the increase in costs for nuclear construction identified above, the traded price of carbon would have to be increased to above EUR 75/tonne CO2 to make nuclear cost-effective (see also pp 32-4).

If this price was applied across the board, it would increase electricity prices by 50%, provide a massive windfall for existing clean generators and would distort a market already replete with revenue support mechanisms. If the carbon floor price was targeted at new nuclear alone, it would look like a massive subsidy for nuclear and it would require a new mechanism to recycle funds from polluters to ‘clean’ producers, separate from EU ETS carbon trading.

Both power utility regulator Ofgem with its Project Discovery, and the Department of Energy and Climate Change (DECC) with its Energy Markets Assessment, are looking at how the energy markets should be modified. Any changes to the market must provide the right incentives for nuclear utilities to drive down construction costs in the medium term.

How can we overcome the dilemma of ensuring investment in clean electricity while protecting the consumer? We must recognise:

- The nuclear industry has to take responsibility for getting the trend of its construction costs down in the way that the Koreans have shown can be achieved

- Longer-term certainty of electricity price would allow access to lower rates of return and lower the viable electricity prices required in the investment case

- Other clean forms of electricity may well cost more than nuclear even if some of this may be disguised by transfer prices for Renewables Obligation Certificates, or other forms of environmental levy.

There is plenty for the government to do to reform the power market, and to avoid both the nuclear cost and electricity price troubles on the horizon, before EDF and Centrica make firm nuclear investment decisions in 2011.

Author Info:

Tony Roulstone, director, Bracchium Ltd, 4 Spinney Lodge, Repton, Derbyshire DE65 6PH, UK.

| References |

| [1] Yangbo D., Parsons, J.E., ‘Update on the Cost of Nuclear Power’, MIT Center for Energy and Environmental Policy Research Working Paper 09-004. |