Fuel review: enrichment

The coming oversupply

3 November 2009Several trade issues were resolved and enrichment suppliers moved to implement technology evolution and expansion plans; market prices continued their climb. By Gene Clark and Treva Klingbiel

Enrichment requirements for the world’s growing fleet of nuclear power plants are expected to expand significantly. Current enrichment capacity on a world-wide basis is just sufficient to meet requirements, but the potential pace of enrichment capacity expansion is expected to out-strip the growth in requirements. Thus, it is not likely that all this expansion potential will come to fruition. The continuation of enrichment trade restrictions in the USA and European Union (EU) will have a major bearing on which projects go forward. Perhaps the biggest uncertainties are the status of USEC’s American Centrifuge Project (ACP) and the feasibility of GE Hitachi-Global Laser Enrichment LLC’s (GLE) laser-based SILEX process.

The SWU Market

The enrichment market is comprised of two general segments: spot and long-term. The spot market refers to the market for transactions under which all deliveries are made within a year of the transaction date, where the transaction date is the date at which the buyer and seller agree to the major commercial terms (quantity, price, delivery schedule and location).

Because of trade restrictions from 1992 to the present in the USA and EU, the spot market has been bifurcated, with one prevalent (‘restricted’) price in those buyer markets and a different (‘unrestricted’) price outside those two regions.

The second general segment is the long-term market, characterized by multi-year deliveries under the transaction, usually starting beyond the one-year time frame. Long-term base prices are the equivalent base prices in new transactions in the month indicated, for which the settled price at delivery is determined by escalating this base price by one or a combination of generic inflation indexes, like the US Implicit Price Deflator.

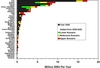

As shown in Figure 1, in recent months periods of climbing spot market prices have alternated with stalls.

The reasons for this upward price trend with several stalls are multiple, and include the following. For the long-term price, most of the transactions have been in the USA, which has restrictions on imports of enriched uranium from Russia and France due to anti-dumping concerns. Because Urenco supplies are essentially sold out, the most active supplier has been USEC, Inc., which needs higher prices to justify its ACP.

For spot prices, supply has become rather tight compared to demand and exacerbated by the movement toward lower enrichment tails assays, driven by the higher delivered uranium prices to utility companies recently. The periods of moderation in spot prices over the past year may be attributed to expectations of further spot supplies from Russia (due to the finalizing of the modification to its Suspension Agreement with the USA, thus giving Russia some near-term quota for imports) and from the US Department of Energy (DOE). However, Russia has followed a policy of sales to US utilities only under long-term contracts, and DOE has not been forthcoming with further supplies to the market.

It remains to be seen what the future will hold for market prices, but the weakening of the US dollar against the European in richer countries’ currencies over the past few months has tended to drive up those enrichers’ costs in US Dollar terms, which is the pricing basis for most new long-term enrichment contracting. The financial position of USEC (see box panel) could have a major impact on future prices, as well.

Demand Status and Outlook

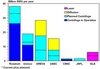

Total world requirements for enrichment services in 2008 are estimated by the World Nuclear Association to have been about 51 million SWU, distributed among countries as shown in Figure 2. The USA currently accounts for about 30% of world requirements of 51 million SWU, followed by France, Japan and Russia. But the picture might look very different in 2020.

Most of the growth in annual enrichment requirements is concentrated in Asia (China, Japan, India and South Korea), Russia and the USA. These six countries account for almost 70 percent of the projected growth in annual requirements from 2008 to 2020 for the upper, or most optimistic, scenario.

Supply Status and Outlook

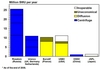

The current status of the world’s enrichment production capacity is shown in Figure 3 for the major commercial suppliers. Eurodif in France and USEC in the USA currently rely on the gaseous diffusion, an older technology that requires significant amounts of electricity for production. In fact, electric power is typically 60-75 percent of the operating cost of a diffusion plant.

Because of the high cost of electricity during peak periods, gaseous diffusion plants are not typically run at full capacity for the whole year; thus, a portion of the plant’s nameplate capacity is rendered uneconomical.

Rosatom in Russia; CNNC in China; and Urenco in the United Kingdom, Germany, and the Netherlands all employ the gas centrifuge technology, the more modern technology that requires only 3-5 percent of the electricity consumption per SWU of the diffusion technology. Russia installed its first centrifuge cascades in 1962, and Urenco has been installing its own variation of the centrifuge technology since the early 1980s. The CNNC plant in China uses Russian-supplied centrifuges.

The potential outlook for primary production, shown in Figure 4, points toward a large increase in capacity. Russia’s Rosatom plans to increase capacity, between expansion at its existing four facilities and the International Uranium Enrichment Center, by almost 50 percent – up to an eventual level of about 38 million SWU per year. CNNC in China is increasing its capacity of Russian-supplied centrifuges by 50 percent.

AREVA (the majority owner and operator of the Eurodif diffusion plant) is planning an initial-capacity gas centrifuge plant, based on the Urenco technology, of 7.5 million SWU per year, with potential expansion at the same site up to 11 million SWU per year. At the appropriate stage of centrifuge startup, AREVA will phase out its gaseous diffusion plant.

USEC in the USA is planning to phase out the use of gas diffusion by building the American Centrifuge Plant, based on modified technology originally developed by the DOE.

Japan Nuclear Fuel Limited (JNFL) has constructed a centrifuge plant based on a domestic design, but is in the process of final shutdown and evaluation, as the centrifuge machines have not performed reliably. Thus, JNFL is redesigning the machines, with a target of installing about 1.5 million SWU of annual capacity for the Japanese nuclear power program’s needs.

Finally, the Global Laser Enrichment consortium is currently in the demonstration stages of its laser-based system known historically as SILEX.

The capacity of all these potential centrifuge and laser projects totals almost 90 million SWU per year, sufficient to meet the needs of WNA’s Upper Scenario for the year 2024, and well in excess of requirements before that year and for the other two scenarios. Accordingly, it is not likely that all these projects will be developed on the schedules espoused by their owners.

Service or product?

Trade restrictions and other government market intervention have been hallmarks of the nuclear fuel market almost since its inception. Such activities are as prevalent and pervasive as ever today. This market intervention takes two major forms: import restrictions and disposition of excess military enriched uranium stocks.

The US Supreme Court ruled unanimously on January 26, 2009, that imports of low-enriched uranium (LEU) under enrichment services (or SWU) contracts are subject to US antidumping law.

In 2001, the US Department of Commerce (DOC) determined that Eurodif of France had dumped LEU into the USA, and in 2002, the Department issued an order imposing duties on French imports to offset the dumping. In March 2005, the US Court of Appeals for the Federal Circuit ruled that LEU sold under SWU contracts constituted the sale of a service, not a product, and therefore was not covered by US antidumping laws.

Both the US government and USEC, the sole current US uranium enricher, sought reversal of the Federal Circuit decision. The Solicitor General’s appeal to the Supreme Court was supported by DOC, as well as the US Departments of Energy, State, and Defence.

The Supreme Court opinion reverses the Federal Circuit’s ruling and gives DOC the ability to enforce its dumping finding against all LEU regardless of the type of contract involved. As such, and given the Supreme Court’s status as the highest court in the USA, this issue of service vs. product seems to be now resolved, unless an aggrieved party can establish that such a finding violates some international treaty to which the USA is a party.

As part of a subsequent settlement of the dumping complaint filed by USEC against French exports to the USA, USEC announced in May 2009 that it had agreed to sell commercial SWU to EURODIF in 2009 and 2010.

In February 2008, Rosatom Director General Sergey Kiriyenko and US Department of Commerce Secretary Carlos Gutierrez signed the latest amendment to the 15-year-old agreement suspending the dumping investigation initiated by DOC in November 1991. This amendment acknowledges that after 2013 Russia will no longer have its indirect market share for LEU in the USA, because of fulfillment of the terms of the Megatons-to-Megawatts programme (discussed below) and that Russia has had no direct retail sales (other than deliveries under enrichment contracts ‘grandfathered’ under the original suspension agreement) since the dumping investigation was initiated.

In essence, the new amendment allows Russia to sell LEU (uranium and enrichment) directly to US utilities an amount equal to about 20 percent of US utility requirements starting in 2014 – a level equivalent to about half the level currently enjoyed by Russia under the Megatons-to-Megawatts program – with some very small quantities allowed in 2011-2013.

On July 21, 2009, TENEX (the Russian LEU export firm) announced it had signed its sixth long-term contract to supply LEU to a US utility – this one with Constellation Energy Nuclear Group. The contract covers a portion of Constellation’s needs over the 2015-2025 time frame. This contract follows earlier long-term contracts TENEX signed with Exelon and the Fuelco group (AmerenUE, Pacific Gas & Electric and Luminant) in May and June 2009, respectively.

Megatons-to-megawatts

This very successful program, of dismantling Russian nuclear warheads and downblending the extracted highly-enriched uranium (HEU) to make commercial nuclear fuel, currently supplies about half the US utility industry’s fuel consumption, the equivalent of 10 percent of all US electricity consumption. The program, initiated by a government-to-government agreement in 1993 and followed by several commercial agreements, is set to expire after 2013, at which time 500 tonnes of HEU will have been extracted and turned to commercial nuclear fuel.

One of the ongoing issues has been the pricing level for the SWU component (sold on a wholesale basis to USEC). In February 2009, USEC and TENEX (the Executive Agents for the US and Russian governments, respectively) signed an amendment to their commercial contract, setting up a new price mechanism to be used for SWU deliveries in 2010-2013 (last four years of the contract).

As a follow-on enticement to the Russian side of this program, the US Senate passed in late September 2008, a House measure that includes an amendment by retiring Senator Pete Domenici to create new incentives for Russia to keep blending excess military stocks of weapons-usable HEU down to civil LEU fuel after 2013. President Bush signed the bill into law on September 30, 2008.

The amendment would allow Russia an extra five percentage points of US market share for LEU under the recent Suspension Agreement amendment, provided the extra LEU is derived from dismantled Russian nuclear warheads. It remains to be seen whether the Russian side will modify its previous stance as it has stated it would not be willing to extend the downblending program.

Author Info:

Gene Clark, Chief Executive Officer, TradeTech, 1289 N. Fordham Blvd, Chapel Hill, NC 27514 USA; Treva Klingbiel, President, TradeTech, Dominion Towers, Suite 720 South, 600 Seventeenth Street, Denver, CO 80202 USA

Related ArticlesNuclear fuel market to double by 2020 Stability in tough times Enough for today Russia set to sell shares in enrichment center USEC reassembles lead cascade at American Centrifuge Incident at Gronau enrichment plant| Supplier movements |

| Supplier movements |