Fuel review | Enrichment

Supply satisfactory–excepting surprises

6 October 2010The enrichment market is expected to remain relatively in balance for the long term. A number of suppliers are capable of adding new capacity as needed, though the capital-intensive nature of enrichment technology will prevent significant oversupply. Small shortages are certainly possible during the next several years, in the event of delays in new plant commissioning. By Thomas Meade and Michael H. Schwartz

The enrichment market slowed during 2009, but was still strong by historical standards. ERI’s estimate of new commitments executed during 2009 was still considerable at 70 million separative work units (SWU). For comparison, contracting during 2008 and 2007 was estimated at 139 and 77 million SWU, respectively. Contracting in 2009 was well-diversified, which has not always been the case in the recent past. Particularly notable was Rosatom’s return to the US market, with nine new contracts signed in 2009 and the first half of 2010, and its success in Japan, where long-term relationships were formed following years of short-term deals.

Enrichment market term prices have risen steadily since December 2005, with the long-term price indicator reported by TradeTech peaking at $165 per SWU at the end of May 2009. The reported term price then stabilized, holding steady for most of the last year, before declining to $160 per SWU in April 2010, where it remains as of 30 June 2010. This represents a 3% price decline from last year compared to an average annual increase of 11% over the preceding four years. When evaluated in Euros, the overall increase in enrichment prices over the past five years has not been as significant. The reported gap between spot and long-term price indicators has recently widened to a 4% spot discount. Factors that led to the price run-up include: market realization that increasing requirements will mean tight supply and that needed additional new supply must be supported by market prices; lower transaction tails assays; the importance of long-term supply security for many fuel buyers; increased supplier costs.

Requirements

Nuclear power plant requirements in 2009 were 45.8 million SWU, about the same as observed in 2008. The ERI reference nuclear power growth forecast projects that annual world requirements for enrichment services will steadily increase between 2010 and 2030 at an average annual rate of 2.5% per year. As a result, world enrichment requirements are forecast to rise 21% to 55.9 million SWU by 2015 and an additional 36% to 76.1 million SWU by 2030. On a relative basis, growth in enrichment services requirements in the reference forecast is greatest in East Asia and the ‘other’ region (which includes South America, the Middle East and Africa), but is significant in the Commonwealth of Independent States (CIS)/Eastern Europe as well. The US and Western Europe are expected to demonstrate more modest growth. World requirements are highly committed (>95%) through 2012. Uncommitted requirements then rise steadily to 6% of world requirements in 2013, 13% in 2015, 25% in 2020 and 45% by 2025.

Supplier profiles

The Areva Georges Besse I (GB I) gas diffusion plant near Pierrelatte, France, has a nameplate rating of 10.8 million SWU per year. As a result of high power costs, GB I annual production is typically limited to 8 million SWU or less, as was the case in 2009. Although shutdown of GB I was originally planned for 2012, it may in fact stop production at the end of 2010. The possibility of the earlier closure is the result of utility EDF’s decision to end its offtake from GB I. If EDF is forced to take deliveries from GB I in 2011 and 2012, which it does not need, the plant will stay open longer.

Areva is presently building a new enrichment plant near Pierrelatte, Georges Besse II (GB II), which will result in the replacement of its existing plant with a new 7.5 million SWU per year enrichment plant that utilizes Enrichment Technology Corporation (ETC) centrifuge technology. Over-production from GB I will contribute to market supply in the years following the plant’s closure, and before GB II reaches full production volumes. Areva has built up inventory to supplement centrifuge production as it ramps up. The current schedule brings GB II into commercial operation in 2010 with nameplate capacity of 7.5 million SWU per year installed by 2016.

Areva is also pursuing a US Nuclear Regulatory Commission (NRC) license that will allow it to build and operate a nominal6 million SWU per year centrifuge enrichment plant in the US, the Eagle Rock Enrichment Facility (EREF), using the same technology as GB II. The US Department of Energy granted conditional approval for a $2 billion loan guarantee for the EREF in May 2010. The EREF will have a maximum annual enrichment capacity of 6.6 million SWU, which yields 6.4 million SWU per year when operating at a 97% capacity factor. Areva is committed to building the first half of the EREF, with initial production expected to occur in 2014. Capacity is expected to reach 3.2 million SWU in 2018. The EREF could be further expanded to 6.4 million SWU by 2021 if warranted by market conditions.

Urenco’s current and future enrichment capacity in Europe is obtained from ETC centrifuge enrichment technology that is presently in operation or expected to be installed at Urenco’s three European enrichment plants in Gronau, Germany, Almelo, Netherlands and Capenhurst, UK. These plants had a combined annual production capability of 12.2 million SWU at the end of 2009, which is expected to increase to an estimated 13.0 million SWU per year by the end of 2011.

Urenco subsidiary Louisiana Energy Services (LES) is moving forward with construction and operation of the 5.9 million SWU per year Urenco USA plant (previously known as the National Enrichment Facility) in Lea County, New Mexico, using ETC centrifuge technology. An NRC license was issued in June 2006 for a nominal 3 million SWU per year capacity for Urenco USA. In November 2008, plans were announced to increase the capacity to 5.9 million SWU per year. LES brought Urenco USA into commercial operation in June 2010 and expects to achieve the full 5.9 million SWU per year enrichment capability in 2015.

USEC’s present enrichment capability comes from the 8 million SWU per year gas diffusion plant located in Paducah, Kentucky. The Tennessee Valley Authority (TVA) supplies electric power under a contract that runs through May 2012. Paducah production was 6.4 million SWU in 2009. Production is expected to decrease somewhat in 2010 as the power supplied under the TVA contract decreases. A portion of the Paducah plant’s capacity is devoted to underfeeding operations, leaving about 5 million SWU for commercial enrichment sales. (Underfed enrichment operations run at lower-than-contractually-specified tails assay by using additional SWU instead of a customer’s uranium feed). The Paducah plant is expected to shut down in June 2012, although it may remain open several years longer if competitive power contract extensions can be negotiated. SWU inventory is expected to contribute to supply after the plant’s closure.

USEC plans to replace the Paducah plant with a new 3.8 million SWU per year enrichment plant known as the American Centrifuge Plant (ACP). USEC has been conducting demonstration testing of its AC100 centrifuge machines since the beginning of 2008, but has been forced to slow ACP spending until a positive decision is made by the DOE under the loan guarantee programme. If a positive loan guarantee decision is made by DOE before the end of 2010, then it is presently expected that the ACP could begin commercial operations in late 2012 and reach full nameplate capacity by the end of 2015. USEC expects to submit a revised application to the DOE during 2010. USEC’s prospects for a positive decision improved greatly in early May when DOE decided to reprogramme an additional $2 billion so that both the USEC ACP and Areva EREF could be funded. Largely contingent on USEC’s success in obtaining the loan guarantee, Toshiba and B&W have decided to make a $200 million equity investment in USEC and the Japanese government appears willing to guarantee $500 million in ACP loans. Cost, schedule and performance issues still carry risks and uncertainties for successful ACP deployment.

State-owned Rosatom uranium enrichment plant production capability refers to the production at four plants in Russia, but production is reduced approximately 5% from nameplate capacity due to the low operating tails assay employed. Resulting production for 2009 is estimated to be 25.2 million SWU. As a result of centrifuge replacements, total Russian enrichment production is projected to increase to 28.6 million SWU by 2014, hold steady for five years, and then steadily increase to 34.5 million SWU by 2030 using a 95% capacity factor.

For 2009, Rosatom devoted approximately 7.4 million SWU to CIS and Eastern European requirements at 0.11 weight percent (w/o) 235U operating tails assay, which is referred to herein as 'Rosatom Internal'.

Rosatom also provides enrichment services to Western customers and China through its marketing subsidiary Techsnabexport, known as Tenex, primarily in the form of enriched uranium product (EUP) produced at its enrichment plants, which is referred to herein as 'Rosatom Export' and totaled 5.7 million SWU in 2009. The wholesaling arrangement with European suppliers is declining, but direct exports to Western customers (and China) are forecast to have the potential to increase to 9.2 million SWU/year by 2015, and 13.4 million SWU by 2030. A proposed Kazatomprom equity investment in one of Rosatom’s existing enrichment plants will not lead to an increase in capacity, but could lead to a new seller of Russian enrichment services tied to uranium mined in Kazakhstan.

A major increase begins in 2014 with the direct delivery of at least 3 million SWU per year to the US market, with smaller amounts beginning in 2011, consistent with the terms of current US law. The Russian Suspension Agreement was amended in February 2008 to allow the import of enriched uranium product (EUP) into the US that is equivalent to 20% of nuclear power plant requirements (about 3 million SWU) starting in 2014. In addition, a total of 0.5 million SWU can be imported between 2011 and 2013. Tenex has contracted 40% of its US quota to date. Subsequent legislation allows Russia’s share of the US market to increase to 25% if additional HEU is blended down, but this is considered unlikely.

The Russian HEU-derived low enriched uranium (LEU) mainly originates from the US-Russia Agreement for the downblending of 500 million tonnes (MT) HEU. The enrichment content is expected to remain at 5.5 million SWU per year through 2012, dropping to 5.3 million SWU in 2013 when the term of the current agreement concludes. The 5.5 million SWU figure was equivalent to approximately 6.1 million SWU in 2009 when evaluated at the average Western transaction tails assay (about 0.25 w/o 235U). ERI expects that this arrangement will end in 2013 as scheduled. In addition to the US-Russia Agreement, a small quantity of SWU is derived from Russian HEU (at 15 to 20 w/o 235U) directly blended with European utility reprocessed uranium (RepU). The programme has gradually expanded and now provides an estimated 0.7 million SWU per year, but is expected to gradually decline after 2010, and disappear by 2025 as the availability of HEU for mixing with RepU decreases.

China's CNEIC has approximately 1.0 million SWU per year of centrifuge enrichment capability located at two sites. The majority of this enrichment is used internally. CNEIC uses centrifuges that are imported from Russia and will complete expansion to 1.5 million SWU by 2011. Senior officials have indicated that China plans to significantly increase its future enrichment supply capability, and even attempt to become a regional supplier. No details concerning how CNEIC will expand enrichment supply to keep pace with China’s rapidly increasing requirements have been made public.

In Figure 1, 'Other' refers to limited centrifuge enrichment capability in several additional countries that is used internally. The original Japanese centrifuge capability of 1.05 million SWU has been fully retired, but development of a next-generation centrifuge has been completed and is now expected to result in a commercial plant with initial capacity of 0.15 million SWU in 2011 and full capacity of 1.5 million SWU in 2020. Brazil is beginning operation of a small uranium enrichment facility, which is scheduled to gradually ramp up to 0.2 million SWU by 2015 and will be devoted to internal requirements. Despite international efforts against it, Iran continues to install centrifuges and could have 0.1 million SWU of capacity in operation within a year or two.

Recycle materials, primarily plutonium in the form of mixed oxide (MOX) fuel, contributed about 1.6 million SWU-equivalent in 2009, equivalent to 3.5% of annual enrichment services requirements. Recycle materials are projected to supply a total of 2.5 million SWU per year by 2019, averaging 3.5% of requirements between 2010 and 2030 for the reference forecast.

The US trade cases brought by USEC against Urenco and Areva came to a conclusion after Areva and USEC reached a settlement in May 2009. The antidumping order and duties on French LEU remain in place until the next 'sunset' review by US trade authorities in 2012. The settlement followed the Supreme Court's January 2009 ruling that enrichment is a good, not a service, and therefore subject to US trade law.

Market outlook

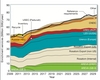

Supply almost exactly equals requirements at present (see Figure 1). In 2009, a total of 48.9 million SWU was the average annual economically competitive and physically usable production capacity that was not constrained by international trade agreements, together with the equivalent enrichment services that were derived from Russian HEU and other sources reflected in the discussion just provided. This figure was only 3.1 million SWU (7.0%) more than nuclear power plant operating requirements of 45.8 million SWU. About half of the excess supply was purchased for inventory-building purposes.

A close balance between available supply and power plant requirements is forecast to continue well into the future. During the 2010 to 2012 period, an average annual supply excess under the reference nuclear power growth forecast of 1.5 million SWU per year (3.0% of requirements) is projected. However, an annual supply deficit averaging 0.8 million SWU (1.5% of requirements) is projected for 2013-2015. As new capacity comes online in 2016, supply once again will be able to meet requirements. For the following decade, supply is forecast to exceed requirements by an average of 1.8 million SWU per year. A small annual supply deficit reappears in 2027.

It should be emphasized that this level of supply, which barely meets projected requirements under the reference nuclear power growth forecast, is dependent on the timely startup and expansion of four new enrichment plants. However, it is worth noting that there are a number of sources that could potentially fill any supply deficits in the long term. Among them are:

Enrichment Technology Corporation (ETC). The company, which is owned equally by Areva and Urenco, appears to have sufficient excess centrifuge manufacturing capability during the 2016 to 2027 time frame to support further expansion of European and US enrichment capacity by Urenco and Areva, if needed. It is also possible that another supplier could purchase ETC centrifuges.

Global Laser Enrichment. GE-Hitachi (GEH) Global Laser Enrichment (GLE) has published a phased commercialization plan for testing and implementation of the Silex laser enrichment technology. The GLE venture added a third partner in June 2008, when Cameco purchased a 24% interest. In April 2010 GLE announced the successful completion of its initial test loop measurement programme. GLE stated that great progress was being made in demonstrating the capability of the technology. Test loop operation and measurements are to continue through 2010, with increasing focus on the engineering design effort. A commercialization decision, which has not yet been made, could lead to initial production of 0.5 million SWU as early as 2013, with total annual production capacity of 3.5 to 6 million SWU. The NRC is currently evaluating GLE’s license application for a commercial facility to be located next to GEH’s fuel fabrication facility in Wilmington, North Carolina.

Rosatom. Additional supply from Rosatom could be obtained if trade constraints are relaxed. This would support Rosatom’s plans for expanded enrichment capacity by redirecting some of its existing enrichment capacity from tails enrichment to create natural uranium equivalent material, to the enrichment of natural uranium for NPP fuel.

Author Info:

Thomas Meade and Michael H. Schwartz, ERI, (Energy Resources International), 1015 18th St NW, Suite 650, Washington DC 20036, USA