Hydrogen

Launching hydrogen

28 July 2005Switching to hydrogen-fuelled transport is an obvious and widely-acclaimed fix for the problems now associated with burning oil. Before this transformation can be realised, the biggest issue that must be resolved is where the hydrogen is actually going to come from. By Alistair I Miller

To launch the ‘hydrogen age’, there is a strong case for using conventional water electrolysis and off-peak energy from Generation III+ reactors to produce the hydrogen where it is initially needed in comparatively small quantities. Implementation of large-scale, centralised production for extensive transport use and for chemical manufacture follows logically.

WHY WE SHOULD CARE

With the coming into effect of the Kyoto accord to curb greenhouse gas emissions, the countries of the developed world – with the exceptions of the USA and Australia – have committed to emissions reductions by 2012 of around 8% from 1990 levels. European and Eurasian countries dominate the Kyoto-committed group: data for 2003 shows that they had reduced carbon-based fuel use by 14% and CO2 emissions by 18%. Collectively, they are well on target to deliver on their commitments. The apparent good news ends there because the achievement of the Europeans largely came from one-

off shifts from coal to gas in energy sourcing in the early 1990s; the rest of the world has added 4.5t of CO2 emissions to every one that the Europeans cut; European emissions then began to climb again; and, most importantly of all, ultimate stabilisation of CO2 levels in the atmosphere requires a 60% reduction below the 1990 level, rather than the 18% increase that has meanwhile occurred globally.

We should care because CO2 remains in the atmosphere for over 100 years – always assuming that the mechanisms that remove it to the deep oceans do not break down – which is an unsettling unknown. So CO2 addition may effectively be an irreversible act by our generation and the evidence of it already causing temperature rise is compelling.

More recently, a second effect has been perceived: rising acidity in the oceans’ surface waters. Some climatologists have suggested that 600ppm of CO2 in the atmosphere is the level that will trigger irreversible climate changes but the figure is highly speculative. However, by lowering pH by 0.4 units, 600ppm is a level almost certain to cause marked disruption of the capacity of the oceans’ phytoplankton to form their calcium carbonate exoskeletons. We are currently on track to pass 600ppm soon after the middle of this century.

In short, the prospects for stable survival of mankind as the dominant species on our planet are grim, and neither conservation nor Kyoto offer appreciable remediation. A massive switch to energy sources that do not emit CO2 is essential and nuclear power is the only demonstrated technology offering sufficient capacity. Included within that switch, nuclear power must be adapted to supply the almost 30% of energy used in transportation. Unless there is a notable improvement in battery technology, the new fuel will be hydrogen.

PRODUCTION TECHNOLOGIES

To be effective for planetary CO2 abatement, hydrogen production must satisfy three criteria: near-zero associated CO2 emissions, wide availability, and affordability. What are the near-term options? Two main hydrogen-producing technologies currently exist: steam-methane reforming (SMR) dominates large-scale hydrogen production and water electrolysis is confined to small-scale applications. However, the cost of natural gas is the major component of SMR-produced hydrogen and growing worldwide energy demand and broadening applications for natural gas have recently ended a 20-year period of relative stability in natural gas prices, which have risen by over a factor of three.

After around 2025, widespread deployment of high-temperature Generation IV nuclear reactors could offer a new option of producing hydrogen using high-temperature heat with little or reduced electrical input. For the proponents of highly efficient energy conversions, these high-temperature processes are an elegant prospect, well worth the international efforts currently directed to delivery of affordable hydrogen from either indirect thermochemical water-splitting (for example, from the sulphur-iodine cycle) or high-temperature electrolysis. This technical prospect is very enticing but is still far from practical realisation. Hence it should not be justification for 20 years of inaction on transport and the consequent addition of a further 15ppm of CO2 to the atmosphere. Moreover, thermochemical methods are intrinsically centralised and large-scale while the initial need is for small-scale, distributed production matched to the gradual emergence of hydrogen-fuelled vehicles. Assuming thermochemical processes do deliver their projected efficiency, they could start to penetrate the market just when its growth starts to justify centralised production. Prior to that, hydrogen will have to be supplied either by SMR technology with CO2 sequestration or by electrolysis. If the latter prevails, it will create a window of great opportunity within the next 15 years for nuclear energy. Can it compete?

ECONOMICS OF DISTRIBUTED ELECTROLYSIS

About half the transportation market is accounted for by light vehicles and, for these, service stations would likely supply hydrogen – home electrolysers are technically practicable but are probably constrained by cost, safety and the need for flexible supply. Assuming the price of fuel cells drops sufficiently for these to be the preferred power generator (rather than an adapted diesel engine), the expected conversion efficiency of hydrogen to electricity would be around 55% and the average North American car would consume about 0.7kg per day (kg/d) of hydrogen. For similar range to today’s automobiles, a typical 40-litre gasoline or diesel fill-up (~28kg) will be replaced by 3kg of hydrogen (since the fuel cell has three times the efficiency and hydrogen has three times the energy density per unit of mass). So, envisage a service station dispensing 300 fuellings per day – about one every five minutes and quite a high number. (This choice fits the 1t capacity of a typical tube trailer making one hydrogen delivery a day.) Table 1 shows that four large electrolysers would provide this by on-site production.

Providing hydrogen at these local outlets would have three main cost elements: hydrogen production; sequestration where CO2 is also produced (or, much less desirably, an equivalent carbon-emission charge); and energy distribution either as hydrogen or as electricity for hydrogen production. The three options to consider are on-site electrolysis, an on-site SMR, and a larger SMR serving a number of service stations.

A city case-study

Envisage a typical city of about 1 million light vehicles covering a diameter of 40km. If one were to provide a hydrogen fuelling service to this city through ten service stations, it would require roughly the pattern of Figure 1 – a ring of nine stations plus one central station, each serving a 7km radius. At 1t/d of hydrogen from each station, about 14,000 vehicles are supplied – about one in 70 vehicles are operating on hydrogen. At 10t/d, the total demand for hydrogen is within the practicable scale of a small SMR. Expressed in energy terms, hydrogen is being supplied with an energy content of 17MW.

Option 1: Production by SMR

A single SMR could supply hydrogen by pipeline or by road. Figure 1 shows a plausible arrangement of an SMR on the edge of the city, a supply pipeline to the central station and a ring-line linking the other stations. The total length is around 133km. Alternatively, a trucking option must cover around 540km (assuming straight-line delivery and including return journeys). Two trucks operating 16 hours per day should be able to handle this distribution.

Costs for hydrogen distribution by pipeline and by truck have been estimated by C E G Padró and V Putsche of the National Renewable Energy Laboratory. They show that the cost of pipelines becomes virtually constant below 0.13GW. (For consistency with the rest of this discussion, hydrogen energy is converted to the higher heating value, HHV.) This smallest pipeline size is capable of fuelling over 100,000 cars, suited to supply the city when hydrogen-fuelled vehicles penetrate 10% of the market but overly large for early stages of hydrogen deployment. The total cost for a 133km pipeline network of this minimum size is $1875/t for the example’s 17MW system.

The truck transport alternative would likely operate with compressed gas. For compressed gas transport by tube trailer, the expected cost ranges from $700-1400/t ($6-12/GJ lower heating value) range for distances of 16km and 160km, respectively. By simple proportion, for the average trucking distance of 13.3km from a single SMR, the cost should be $580/t. Trucking appears to be the better choice until the magnitude of the operation rises by a factor of three since hydrogen supply by pipeline could expand by an order of magnitude with no additional cost, but a proportionate fall in unit cost.

The cost of CO2 sequestration will vary depending on accessibility of suitable underground storage opportunities and is quite an uncertain cost. The UK’s Department of Trade and Industry (DTI) has estimated a cost of $30/t of CO2 for sequestration in a deep geological aquifer 300km from the source. Since 1t of hydrogen by SMR produces 7.75t of CO2, this cost estimate for sequestration adds $230/t. Other estimates of the cost of CO2 separation suggest that the DTI estimate may be optimistic; it is surely too low for smaller installations and SMRs at every service station would incur a much higher cost.

The capital cost of SMRs varies with size in proportion to about 0.66 of power. A 250t/d (world-scale) plant costs about $75 million. So a 10t/d plant would cost about $18 million, and a 1t/d plant would cost $4 million. (For all technologies, capital costs are recovered assuming 20% per year.)

The largest cost component for hydrogen produced by either SMR or electrolysis is for the input energy. In recent years, the wholesale price of natural gas in North America has been very volatile and there is no simple way to assign a value that would be comparable with electricity prices. One rough approach is to consider conversion of natural gas to electricity at an efficiency of around 60% using a combined-cycle gas turbine. Thus electricity in the Canadian province of Alberta in 2003 and 2004 at around $38/MWh is equal to $10.6/GJ. So natural gas would be worth converting at $6.36/GJ. Though the SMRs considered here are small, they should still come close to achieving 90% conversion efficiency on the basis of energy input to energy content of the output hydrogen. Hence a fuel cost of $7/GJ of hydrogen output is appropriate on this basis. That does produce a value in reasonable agreement with Alberta gas prices at the time.

For pipeline supply, there still has to be a matching of the continuous operation of the SMR with the diurnal variation in demand – 12-hour local storage is assumed, though the storage could be at the SMR since the pipeline has ample capacity for higher transmission rates. Local SMRs also need 12-hour storage. For truck supply, once-a-day delivery is assumed so 24-hour storage is needed.

The total estimated costs of hydrogen for the various options at our model service station are summarised in Table 2. SMRs can be presumed to run continuously at near full capacity since there is no rational basis for time-of-day natural gas prices and SMRs do not startup or shutdown easily. The city-wide system is designed to dispense 10t/d.

Table 2 shows the expected advantage of truck versus pipeline distribution on this scale. It also appears to show that local SMR production is inferior to trucking from a remote SMR. Moreover, the small local SMR would surely incur a much higher carbon charge if it were required to practise actual sequestration.

Option 2: Electrolytic production

Can conventional water electrolysis compete? Since high reliability is also needed, the obvious source is nuclear power.

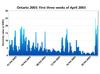

As with SMRs, the cost of energy input is of pivotal importance. Two Canadian provinces – Alberta and Ontario – use a power market bidding system to set the hourly price to be paid for electricity supplied to their grids. The average prices paid (converted to the average for the years) are given in Table 3. But the typical variation illustrated in Figure 2 and summarised in Table 3 show that the averages contain huge fluctuations. Price fluctuations are likely to grow even larger if nuclear displaces coal-fired generation, since an interruptible source will have been replaced by one that strongly favours baseloading.

The cost of electricity generation is taken as that of nuclear electricity from a Generation III+ reactor such as AECL’s ACR-1000. This is expected to cost 3-4¢/kWh (3¢/kWh is used below) and would have supplied these markets profitably – which is important since the electricity for electrolysis has to come from a source with near-zero CO2 emissions.

For comparison with the three SMR cost components, electrolytic hydrogen has four cost elements: the cost of electricity supplied to the grid, the cost of electricity distribution, the electrolysis equipment, and hydrogen storage. Storage is treated in the same way as for SMRs. Electrolysis cells are assumed to cost $300/kW. This is judged by cell manufacturers to be a reasonable price for a basic bipolar cell supplied in large quantities and without special features aimed at lowering voltage. It includes gas compression and power conditioning and leads to the use of 55.3kWh per kg of H2 – equivalent overall to 2.1V.

The key to producing hydrogen competitively by electrolysis lies in actually exploiting the variability of electricity price. If one thinks of electricity and hydrogen as co-products, several advantages emerge: electrical energy is effectively being stored; electrolysis can become a constructive replacement for grids’ spinning reserves, able to be interrupted instantly; and electricity is not supplied through the grid to electrolysers at times of peak demand when the grid is heavily loaded. All of these points should justify a low distribution mark-up, which is an essential cost component for distributed electrolysis. By converting only a fraction of the electricity to hydrogen, one can predominantly use electricity of low value to the grid. Furthermore, by oversizing the electrolysis cell relative to the amount of hydrogen production, one can accentuate the use of low-cost electricity. The utility now becomes a seller of hydrogen and electricity rather than of only electricity.

In estimating the cost of electrolytic hydrogen, actual hourly costs for electricity for the two grids were used. A mark-up of only 1¢/kWh was applied – far below the usual mark-up but with the justification that it would occupy only unused distribution capacity as well as conferring the advantages to grid management outlined above.

To examine the economics of this approach, actual hourly market data for electricity costs (converted to the average prevailing in the year) for 2003 and 2004 and for each province were imported into spreadsheets, which were then used to compute the lowest possible cost for hydrogen production for any fraction of overall conversion to hydrogen. Within the spreadsheets – each holding one year’s data, a number of variables were set: a threshold electricity price above which electrolysis would usually be switched off; a higher threshold that would apply if hydrogen in storage was below a set low level; electrolysis capacity (obviously exceeding that needed for the set fraction of overall conversion since it would be interrupted); and a level of hydrogen storage (not less than 12 hours to allow, very approximately, for the daily cycle of demand). The hourly behaviour of the system could then be computed and variables optimised for the lowest cost of hydrogen production with two constraints: firstly that hydrogen in storage would never be exhausted; and secondly that the year would start and end with full storage. The value of electricity sales is known precisely but no absolute value was assigned to the hydrogen. Instead, the optimisation focused on the selling price needed for the hydrogen to provide net revenue from electricity and hydrogen equivalent to the assumed 3¢/kWh cost of electricity generation. The profitability of hydrogen production can then be easily calculated for any value placed on hydrogen.

Economic comparison: the nuclear advantage

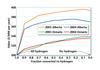

The competitiveness of making hydrogen by electrolysis is best seen by comparing it with the estimated cost of SMR production plus truck distribution. Figure 3 shows the optimised results if hydrogen is valued at $2500/t – about the minimum value at which this conversion becomes competitive.

The results show that intermittent electrolysis would generally have yielded more profit than selling electricity if 10-20% of the electricity were converted into hydrogen at $2500/t, with Ontario in 2004 being a slight exception. Converting all of the electricity to hydrogen would always have been far less profitable.

Valuing the hydrogen at $3300/t is comparable with the centralised SMR and truck distribution and is a competitive basis for comparison. Conversion to hydrogen is now the more profitable option on all scales of conversion for both provinces and both years.

GLOBAL IMPLICATIONS

A common objection to making hydrogen electrolytically is that it is only economic in countries like Canada, where the selling price (and generating cost) of electricity is atypically low. This is simplistic: the more expensive electricity of Alberta in these two years makes electrolytic hydrogen a more profitable co-product than in Ontario with lower average electricity costs. The economics of adding hydrogen as a co-product alongside electricity is a complex function of the value of hydrogen, the cost of producing the electricity, and the price structure of electricity sales. High selling prices for electricity at peak periods provide higher margins for new nuclear electricity production through higher margins.

SENSITIVITY OF COSTS

For SMR-produced hydrogen, each additional $1/GJ to the cost of natural gas adds $148 to the cost of a tonne of hydrogen. Each additional $10/t of CO2 for sequestration adds $78/t to the price of hydrogen.

For electrolytic hydrogen, the key cost uncertainty is over the charge for electricity distribution. Each additional ¢/kWh charge adds $553/t to the price of H2. Charging typical mark-ups of

4-8¢/kWh completely destroys the competitiveness of electrolytic hydrogen. However, as argued above, there are good reasons why both electricity generators and grid operators should view the cost of distribution for this off-peak, interruptible power far more favourably than for normal distribution.

LARGER-SCALE PRODUCTION AFTER 2020

This hypothetical case of under 2% of light vehicles fuelled by hydrogen may reasonably be projected to exist around 2020. While conversion to this level would be a substantial undertaking, it is only a stepping stone to much larger scales of hydrogen use. As the scale of hydrogen consumption grows, pipeline delivery will displace truck delivery and the cost of distribution will become far less important.

To produce hydrogen, a wider range of processes could now enter the picture. As well as the existing processes, high-temperature nuclear reactors operating around 800-850°C could supply energy to: indirect thermochemical processes (such as the sulphur-iodine process); SMRs using nuclear rather than chemical heat; and high-temperature electrolysis in which some of the energy would be supplied by heat. The capital cost component for a world-scale SMR would be about $850/t less than for the small, 10t/d unit. But the economics of conventional electrolysis will not have stood still either in capital cost or power use and new installations could be located close to reactor sites, avoiding the $550/t cost of distribution – the major uncertainty in costing distributed electrolysis.

OUTLOOK FOR TRANSPORT PENETRATION

So what prospect has hydrogen of ousting oil-based fuels? While one can simply argue that hydrogen is the only choice – barring an unforeseen breakthrough in electricity storage – because CO2 emissions from vehicles are far too large to remain acceptable, the economics for a hydrogen economy also look favorable. Although the production cost at a service station is not the complete cost, hydrogen at $2500/t would contribute about $640/y for operation of a typical North American light vehicle using 0.7kg/d. While already containing profits in the hydrogen-plus-electricity revenue stream, it does not include the costs for operation of the service station. Nonetheless, the total is not likely to be so large as to deter conversion to hydrogen.

For comparison, today’s typical 21,000km/y automobile uses about 2400 litres of gasoline costing close to $1500/y, even with the (low) taxes hidden in North American pump prices. Even though the future competition will likely be highly efficient diesel-electric hybrids and their fuel cost could be lower by a factor of three, the production cost for hydrogen still looks reasonable. And provided the production process does not emit CO2, the hydrogen route is pollution-free. The estimated cost of producing hydrogen strongly suggests that hydrogen will not require massive, sustained government support to displace oil-based fuels.

SCALE OF SUPPLY

In Canada by 2030, total energy demand for all forms of transportation is projected to have increased by 30% from today’s figure to reach around 2900PJ/y. The assumptions on fuel efficiency underlying this figure make it somewhat uncertain, but a gain of a factor of two in efficiency for fuel cells seems reasonable. Thus the requirement is for about 1500PJ/y expressed as hydrogen energy or 48GWe. Allowing 70% conversion efficiency between electricity and hydrogen and assuming it were all manufactured by conventional electrolysis, this would require about thirty-eight 1GWe reactors to supply half the projected demand for transportation fuel in 2030. To place this in context, 22 large-scale reactors with a total capacity of 16GWe have been built in Canada to date. If low-temperature electrolysis were supplanted by thermochemical processes and high-temperature reactors, a comparable numbers of these reactors would be needed.

Hydrogen’s displacement of oil will need political commitment worldwide because it will entail a total rework of the technology underpinning the world’s transport. Along the way, some technical advances would greatly assist the move, with the development of affordable, robust fuel cell technology heading the list. But hydrogen supply is not a problem since the obvious source of affordable hydrogen fuel already exists. Nuclear power can expand its product stream from electricity to electricity plus hydrogen. In the absence of any practical alternative, we have to work to make this transition happen and to refute the delusion that conservation and renewables will suffice.

Author Info:

Alistair I Miller, Atomic Energy of Canada Limited, Chalk River Laboratories, Station 44, Chalk River, Ontario, K0J 1J0, Canada

TablesTable 1: Hydrogen scales in commonly used units Table 2: Hydrogen supply options Table 3: Average prices, average prices when below and above the annual averages (/kWh)