FUEL REVIEW: CONVERSION

Increasing in importance

31 August 2004A number of disruptions to the uranium conversion services market at the end of last year upset the previously established balance of supply and demand, focusing the industry’s attention onto this often-overlooked yet essential component of the nuclear fuel cycle. By Julian Steyn and Thomas Meade

The world uranium concentrate (U3O8) to uranium hexafluoride (UF6) conversion services market during the past five years had been characterised by ‘soft’ demand and adequate supply, a situation that changed dramatically in November 2003 when the Russian government trading company, Techsnabexport (Tenex), announced that it would no longer supply its former marketing agent Globe Nuclear Services & Supply (GNSS) with U3O8 and UF6, leaving a significant-sized group of its customers with a major supply problem. This situation was further exacerbated when the operation of the Honeywell International uranium conversion plant located in Metropolis, Illinois, was disrupted in September and December 2003. These disruptions resulted in an immediate market hardening and an industry-wide realisation that the nuclear fuel cycle front end, including conversion, is vulnerable to serious interruption at any time. The outlook is that primary capacity must be expanded because of diminishing secondary supply and thin supply margins, in order to meet the nuclear industry’s gradually expanding needs.

The events at Metropolis caused the North American spot market price which was $5.00/kgU as UF6 at the end of October 2003, to run up to $7.75 by the end of June 2004. The European conversion services spot market price rose from $6.50 to $9.25 during the same period of time. The gap between North American and European spot market prices widened from $0.35 at the beginning of 2002 to $1.50 during the past year, partly due to the growing imbalance in the availability of secondary supply in the two regions. Other factors in the price difference are the availability of primary supply for long-term commitments and transatlantic transportation costs. Regional supply imbalance and transportation costs are expected to be increasingly important factors during the coming years.

The sustainable capacities of the existing conversion plants when combined with the government and commercial inventories in all forms indicate, on the face of it, that the industry should be able to provide adequate equivalent conversion services supply through the middle of the next decade. However, the supply capability margins are relatively thin and, as already demonstrated, an interruption by any one of the producers or the inventory holders could cause problems for consumers. The Metropolis supply interruptions made it clear that inventories of UF6 cannot always be easily swapped out to separate conversion services from UF6 to meet consumer short-term needs and that borrowing is much more difficult than it used to be in the 1990s. The Metropolis plant interruption also highlighted the geographical issues associated with conversion services supply, particularly between Europe and North America.

There is only one European primary supplier currently offering commercial conversion in a region that has a demand that is 50% greater than the indigenous primary capacity. This situation has prompted that supplier, Areva, to consider providing a significant increase in capacity, albeit at a cost that could result in a price that is greater than currently charged in that region. At least one of the two North American producers is looking to expand capacity by the end of this decade.

It is projected that the scheduled shutdown of the small BNFL plant in 2006 and the continuing drawdown of inventories will result in the need for an expansion of primary production capacity in the second half of this decade if the world’s requirements are to be met. Between now and the middle of the next decade, supply and requirements are projected to be in marginal balance. Because of the foregoing marginal capacity situation and the geographic supply logistics issues later in the decade, it is projected that there could be a further hardening in the market price later in this decade.

The reduction of enrichment production in the USA resulting from heavy reliance on Russian highly enriched uranium (HEU) feed has impacted the international conversion services market flow, particularly for ConverDyn. When the planned Louisiana Energy Services enrichment plant is brought into operation in the USA later in this decade then the prospects for the domestic conversion market could brighten.

THE MARKET

The reference case world requirements for conversion services as UF6, UF4, and UO3, that is, in all forms, are projected to rise gradually from 66,500tU in 2004 to 73,000tU by 2025. The annual reference case requirements for uranium as UF6 for enriched uranium fuelled reactors, that is UF6-only, are projected to rise gradually from 63,100tU in 2004 to 70,000tU by 2025. US requirements are projected to remain relatively constant at approximately 21,000tU through 2025 for the reference case forecast. The difference between the two projections represents projected requirements for natural uranium fuel, primarily UO2, for Canadian and UK reactors.

The conversion services spot and long-term market volumes in 2003 were approximately 4.0 million kgU as UF6 and 85.0 million kgU, respectively, slightly more than half of the long-term volume resulting from a single contract with a large European utility. However, the remaining long-term volume was about twice the level of the previous two years. One-quarter of that volume was for sales to US utilities and the remaining three-quarters were for sales to non-US utilities.

The spot market volume has ranged between 4 and 5 million kgU during the past four years. Last year’s spot market contracting volume was split about 40% and 60% among conversion services and UF6, respectively, with enriched uranium product (EUP) being less than 1%. Utilities purchased 90% of the volume in 2003 and traders sold almost half of the volume with ‘others’ and converters selling about 35% and 15% of the volume, respectively.

THE METROPOLIS SHUTDOWN

The USA has only one conversion plant to convert natural U3O8 into UF6, Honeywell International’s Metropolis Works plant. ConverDyn, an equally owned marketing partnership of Honeywell and General Atomic Energy Services (GAES), performs the UF6 marketing and contract administration functions for the Metropolis plant’s UF6 production.

During 2003, Honeywell had a number of problems at the Metropolis plant. For example, it filed event reports with the US Nuclear Regulatory Commission (NRC) in June, July and August. In addition, there were several pipe leak events in September. On 9 September, a plant worker suffered chemical burns after being splashed with hydrofluoric acid during a pipe repair. On 12 September there was release of gaseous antimony pentafluoride during a sampling procedure. In a 20 September 2003 press release, ConverDyn announced that it was necessary to shut down the Metropolis plant production to “do an extensive review of both plant equipment and procedures and to repair or replace certain equipment.”

On 18 November 2003, ConverDyn announced that the Metropolis plant had resumed operation and was expected to return to full production by mid-December. UF6 operations were resumed on 23 November 2003. At that time it was stated that during the two-month shutdown the plant had undergone a major repair as well as a retraining and recertification programme.

The Metropolis plant has three processing lines, two for production and a standby line for maintenance and facilitation of equipment replacement. The plant was operating on a single train following its November restart. On 22 December 2003, just as Honeywell was preparing to restart the second fluorination train, a UF6 gas off-site release occurred, and the plant was shut down again. To accommodate two trains, the first train had been removed from service temporarily for pipe reconfiguration, which is when the release occurred. Honeywell’s preliminary determination was that human error and malfunctioning equipment caused the release.

ConverDyn stated on 23 December that deliveries of UF6 to customers at all locations would be affected by the latest shutdown. On 30 December, ConverDyn sent force majeure letters to its customers advising them that deliveries would slip. ConverDyn confirmed that its inventory was depleted by about the end of December 2003. Honeywell indicated that the Metropolis plant lost about 95 days of full production in 2003, a loss of approximately 3000-4000tU as UF6 that completely exhausted its working inventory.

On 26 March 2004, the NRC gave its approval for restart of the first stage in the uranium conversion process, ore preparation. It was the plan that when the plant was restarted, it would ramp up and operate only one train for the first two to three months – April through June 2004 – in order to demonstrate and ensure that all personnel and equipment were operating properly and meeting NRC requirements. When management was satisfied with implementation of operating procedures on the first line, the second line was restarted in June. It is expected that the plant will be back to full production rate by the end of the third quarter of 2004.

The Metropolis plant shutdown resulted in more than six months of production being lost, about 9000tU. While ConverDyn met most or all of its customer commitments through the end of 2003 by providing supply from its approximately 4000tU stockpile, it is now confronted with a significant catch-up task. It must also build up its working inventory to its former level, placing material at the three Western enrichers in order to facilitate book transfer deliveries.

In implementing the US-Russian HEU agreement, USEC acts as the executive agent for the US government and Tenex acts as the executive agent for Russia. Through a 1994 commercial implementing contract, USEC purchases EUP downblended from HEU derived from dismantled Russian nuclear warheads. The EUP is then sold by USEC as fuel for commercial nuclear power plants. Under the terms of an agreement signed in March 2001, USEC, Tenex and ConverDyn work cooperatively on USEC’s return of natural uranium feed (as UF6) to Russia in connection with the continuing implementation of the HEU agreement. The terms, which involve transactions of natural uranium feed between USEC, Tenex and ConverDyn, allow for the transfer of natural uranium feed by ConverDyn directly to Tenex for Russian disposition.

When USEC purchases EUP from Russia, it pays for the enrichment content and is obliged to return to Tenex an equivalent amount of natural (non-enriched) uranium. While this involves an intricate process of transfers, documentation and logistics, USEC’s large strategic inventory of natural uranium facilitates account transfers of this fungible natural uranium. Under the terms of the agreement, USEC uses account transfers to assist Tenex by giving it the option to take possession of appropriate quantities of returned natural uranium at the Metropolis conversion facility for either return to Russia or sales in the West by Tenex’s designated Western marketing agents. The problems at Metropolis have interrupted this previously smooth arrangement. However, ConverDyn has apparently worked out catch-up schedules with Tenex and the three Western marketing companies.

Cameco’s Port Hope conversion plant has a nameplate capacity of 12,500tU as UF6 per year

PRIMARY SUPPLIERS

The world currently has five major commercial primary suppliers of conversion services for transforming uranium mine concentrates into either UF6, ceramic grade uranium dioxide (UO2), or uranium metal. Two of these suppliers are in North America, two are in western Europe, and one is in Russia. The suppliers are: BNFL, Cameco, Comurhex, ConverDyn, and the Russian Federal Agency for Atomic Energy (FAAE), formerly Minatom. The FAAE does not export conversion services as such, but has for some years been exporting EUP containing equivalent conversion services to western Europe, the USA, and east Asia. The BNFL plant is scheduled to be permanently shut down early in 2006, and is currently producing at a declining rate.

The status of the major suppliers is as follows:

BNFL

BNFL operates a 6000tU per year UF6 plant located at Springfields, near Preston, Lancashire in the UK. The plant is currently reported to be producing at between 3000 and 4000tU per year. On 9 February 2001, BNFL announced that it planned to end production at Springfields after 31 March 2006. It took this decision based on the fact that fuel production for its Magnox nuclear plants is expected to end shortly after 2005, when its Magnox stations will then be approaching terminal shutdown. Operation of the Springfields plant for UF6 production alone after the Magnox fuel production ends was not considered commercially economic.

Cameco

Cameco operates the 18,000tU per year Blind River, Ontario, UO3 plant, the product of which is converted to UF6 at the company’s Port Hope, Ontario plant which has a nameplate capacity of 12,500tU as UF6 per year. The Port Hope plant is also licensed to produce 2800tU per year as UO2 to meet the conversion requirements of natural uranium fuelled heavy water reactors in Canada and South Korea. Cameco’s 2003 UF6-plus-UO2 production at Port Hope was about 13,270tU, and 2004 production is expected to be about 12,400tU. UF6-only production in 2003 is estimated to have been about 11,200tU. Cameco is one of the three Western companies that receive UF6 supply under the March 1999 Russian HEU feed Commercial Marketing Agreement; the other two companies are Cogema and Nukem. It is believed that any capacity expansion by Cameco would be in the form of new plant at either Blind River or in Saskatchewan.

Comurhex

Comurhex, a wholly owned subsidiary of Cogema, operates the Malvesi UF4 plant whose product is converted at the Pierrelatte UF6 plant. Production of UF6 in 2003 was estimated to have been about 11,000tU. The Malvesi plant also produces uranium metal. Although the UF6 conversion services nameplate capacity of the two-plant system is 14,000tU per year, the sustainable capacity seems to be only about 12,000tU per year, about 85% of the nameplate capacity. While there are indications that Comurhex may be able to increase the sustainable output level to the 14,000tU per year nameplate rating in the future, there has been less incentive to do so since Cogema began taking delivery of significant quantities of UF6 under the March 1999 Russian HEU feed Commercial Marketing Agreement. However, the management of Areva (which owns Cogema) has indicated that the question of expanded capacity is on its agenda.

ConverDyn

ConverDyn, a general partnership of affiliates of Honeywell and General Atomics, is the exclusive agent for conversion services provided by the Metropolis Works plant. Over the past few years work has been done to increase the plant’s full sustainable capacity up to 14,000tU per year. ConverDyn expects that the plant will be operating at that production rate by the end of this summer. In spite of the plant’s shutdown in September 2003, it produced approximately 7000tU during the year. Again, in spite of the plant not being brought back into operation until the end of April, it is expected that it will produce almost 8000tU in 2004. Looking ahead, ConverDyn anticipates expanding annual capacity by a further 3000-4000tU by the end of this decade. There is room at Metropolis to expand capacity since the existing plant occupies only about 60 acres of the current 1000-acre site.

Russia

The Russian FAAE is understood to have conversion plants in three locations: Angarsk, Tomsk and Irkutsk. While the physical annual capacity of the three-plant system has been variously reported to range from 10,000tU to more than 20,000tU, it is estimated that 2003 production was only about 4500tU. This estimate is based on analyses of uranium feed that is coming primarily from Russian and Ukrainian mines, and from uranium enrichment production levels. Since the Russian centrifuge enrichment capacity is reportedly used to clean up conversion plant product, Russia has not historically sold either conversion services or UF6, except as it is contained in EUP. Additional limits exist in the form of trade constraints in the European Union and US markets.

China

China is capable of meeting its own current internal annual demand for UF6 of about 1500tU. Annual capacity is projected to increase in accord with indigenous requirements to 2500tU by the end of the decade, and to 3000tU by 2020.

There are also small conversion facilities operating in Argentina, India, Brazil, and South Korea. The total annual capacity of these small plants is currently about 700tU.

INVENTORIES

There are substantial inventories of UF6-equivalent (UF6e) uranium currently being held by governments, utilities and suppliers in the USA and the rest of the world. There is also projected to be UF6e supply from recycle savings, enrichment plant underfeeding, and from enrichment tails upgrading in Russia. These sources could collectively provide UF6 supply amounting to approximately 20,000tU per year through about 2013, when the current Russian HEU agreement ends. If there is an HEU II agreement then inventory supply at up to about 14,000tU per year could continue through about 2020.

The inventory shown in the Table estimates do not include enrichment plant underfeeding and western European and Russian tails that could be upgraded in Russia using that country’s surplus enrichment capacity. The commercial stocks given above assume that approximately half of the West’s commercial uranium inventories are in UF6e form. The commercial inventories given above do not include material that is believed to be held by Russia because quantities are highly speculative and include material in many forms, some of which may not meet Western fuel specifications. Although some materials such as uranyl nitrate will not need to be converted to UF6, they will displace demand for UF6. The Russian HEU includes the blending of HEU with reprocessed uranium in Europe, a programme that will cumulatively displace about 10,000tU of UF6 demand over the next 20 years. The US Department of Energy’s (DoE’s) residual uranium stockpile noted above and some of USEC’s inventory are contaminated with technetium that will have to be removed before they can used for making nuclear fuel.

SUPPLY/DEMAND BALANCE

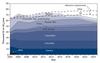

The Figure presents the world supply and requirements balance through 2025 in graphic form. For comparison purposes, reference case requirements projections by both the World Nuclear Association (WNA) and Energy Resources International (ERI) are presented. The WNA projection is more optimistic than ERI’s, projection in that it assumes a higher nuclear power growth, primarily in east Asia during the next decade, to the tune of approximately 21GWe.

No matter which projection is considered, the general outlook is approximately the same, though some people would see the WNA forecast as more alarming. It is projected that while identified existing sustainable capacity should meet ERI-projected requirements in this decade and into the middle of the next decade, the margins will be relatively thin. If the WNA requirements are assumed, then capacity will have to be expanded beyond that shown after 2008. Because of the thin margins and the geographic logistics of supply in the coming years, capacity expansions should be implemented.

Production by the world’s five primary suppliers met approximately 70% of 2003 world requirements. Russian HEU UF6 feed, the secondary market, loans, inventory, enrichment tails upgrading, government stockpile drawdown, and recycle savings in Europe met the remainder. The Russian HEU includes relatively small quantities that are being blended with reprocessed uranium in western Europe.

It can be seen that conversion plant sustainable capacity rises from a current level of about 40,000tU to approximately 50,000tU by the end of the decade. The difference between primary production and requirements is made up by Russian HEU-derived UF6e, inventories in all forms including US HEU, tails upgrading in Russia, and recycle savings supply, until the middle of the next decade. It is projected that non-primary supply in all forms, may collectively provide the equivalent of at least 20,000tU per year through the middle of the next decade. The primary production shown assumes that ConverDyn will expand capacity by 3000tU at the end of this decade and that FAAE and Chinese capacity will be gradually expanded during this and the next decade.

The scenario in the Figure assumes that there will be an extension of the HEU agreement, that is, an HEU II. However, if there is no HEU II supply, then a significant shortfall would begin ten years from now. Supply capacity would drop to 62,800tU as compared to requirements of 67,600tU in 2014, a shortfall of 4800tU. By 2020 there would be a shortfall and need for new capacity of approximately 11,000tU per year.

Because of Russia’s possible perceived need to maintain nuclear weapons parity with the USA, it is possible that there may be no further sales of HEU. The abandonment of START II (Strategic Arms Reduction Treaty) and the recent enlargement of NATO may be factors in this regard. It is most important for the Western markets to have at least five years warning if there is to be no HEU II, in order to make alternative supply arrangements.

Author Info:

Julian Steyn and Thomas Meade, Energy Resources International, Inc., 1015 18th Street, NW, Suite 650, Washington, DC 20036, USA

Tables2004 world total estimated UF6e inventories