FUEL REVIEW: ENRICHMENT

Facing new challenges

31 August 2004The enrichment industry must now contend with higher demands given the movement to lower tails assays in enrichment contracts and continued growth in nuclear power. By Jeff Combs

While there are ongoing efforts to construct three new enrichment plants using centrifuge technology as well as to expand existing centrifuge capacity, the real story in enrichment over the past year has been one of demand more than of supply. China has embarked on an ambitious nuclear power programme, and other countries are expanding their nuclear capacity by a variety of means. Also, with the rapid increase in feed prices, utilities have opted for lower tails assays, increasing the demand for enrichment at the expense of uranium. In fact, since the beginning of last September, the Ux U3O8 price has increased by over 60% to $18.50 while the Ux North American and European conversion prices have increased by about 60% and 40%, respectively.

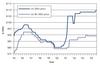

As shown in Figure 1, over several years enrichment prices have been remarkably stable, following their run-up after USEC brought a trade case against Cogema and Urenco. However, these prices have shown some upward movement recently, and the current base price for long-term contracts is of the order of $107 per SWU, while the spot SWU price published by Ux Consulting is $110, a slight premium to the long-term price. In contrast, the tremendous rise in uranium and conversion prices has caused utilities to lower their tails assays in order to optimise their fuel costs, a development which increases their demand for enrichment. In some cases, utilities have reduced their tails assay from 0.35 to 0.30% (weight percent) or below. Further decreases would be forthcoming if feed prices continue to increase relative to SWU prices.

SUPPLY AND DEMAND

On paper, it may appear that there is plenty of enrichment capacity, but some of this capacity is uneconomic or simply not available to the enrichment market. In the past, this lack of availability was dictated by the trade restrictions against Russian enrichment in both the USA and Europe. But, more recently, as market fundamentals have changed, this reduced availability has been due primarily to the reallocation of enrichment capacity to producing uranium. This is particularly the case in Russia, the world’s largest enricher, where 40% of capacity is used to enrich tails for use as blendstock in the HEU deal as well as to create normal uranium for internal consumption and export (see Figure 2).

Because of these changes, the balance between enrichment supply and demand is growing tighter, and promises to do so even more in the future. As shown in Figure 3, enrichment demand is currently quite close to available economic production capacity when depicted on a world basis. Note that as far as enrichment capacity for Russia (Tenex) is concerned, capacity net of that used to enrich tails is shown. Figure 3 also shows the World Nuclear Association’s (WNA’s) reference and upper scenario projection of world enrichment requirements, at both a 0.30% and 0.25% tails assay.

This Figure demonstrates the two fundamental reasons why enrichment demand is likely to increase. One is the underlying growth in the amount of enriched uranium consumed by reactors, as measured by the upper slope of the WNA reference case or by movement from the reference scenario to the upper scenario. The second is the movement to a lower tails assay, which is depicted by the shift from requirements for a given scenario at a 0.30% tails and requirements for the same scenario at a 0.25% tails assay. Of course, if you have a situation where the underlying requirements are exhibiting strong growth and there is movement to a lower tails assay, the effect on enrichment demand is compounded.

At a minimum, this Figure shows that expansion of enrichment capacity is necessary; it is just the degree that is uncertain. While enrichment capacity is clearly expanding, it is doubtful that enrichers had some of the levels indicated in Figure 3 in mind when initially planning their expansion rates. Of course, it remains to be seen whether some of these higher enrichment requirements will develop. Still, the success or lack of success of the various enrichment supply initiatives, discussed next, must now be viewed by a more challenging standard. Similarly, the ability of enrichers to meet these higher targets has an impact on the uranium and conversion markets to the extent that enrichment is able to absorb some of the demand pressures affecting the feed markets.

USEC AND THE AMERICAN CENTRIFUGE

USEC continued to make advancements over the past year in its efforts to build an enrichment plant based on the American Centrifuge, and in doing so continued to exceed milestones set out by the US Department of Energy (DoE). As an example of this, in September of last year, USEC manufactured its first centrifuge rotor tube two months ahead of schedule. Other components are being designed and manufactured at USEC’s Centrifuge Technology Center in Oak Ridge, Tennessee.

In October, USEC received incentive proposals from Ohio and Kentucky to locate the company’s full-scale centrifuge facility in their respective states. Also in October, USEC filed a report with the Securities and Exchange Commission indicating that it could gather information more rapidly by making its test centrifuge facility smaller than the originally-planned 240 centrifuge machines. In December, the US Nuclear Regulatory Commission (NRC) recertified USEC’s Paducah and Portsmouth facilities for five years (to 31 December 2008) finding that both sites were in compliance with safety, safeguards, and security regulations. The Portsmouth facility, located in Piketon, Ohio, which is now on standby, will continue to remain in this status.

As expected, USEC selected the Piketon, Ohio site for its commercial plant in January of this year. The existing infrastructure at the site will allow USEC to maintain its accelerated schedule for deployment of its commercial plant and save costs on the construction of new facilities. Other reasons why Piketon had the edge over Paducah related to the seismic problems associated with the Paducah site (it is located near a major fault line) and the fact that the state of Ohio offered USEC tax incentives exceeding $100 million.

After completing an environmental assessment and concluding that there would be no significant impact to the environment, in February the NRC issued USEC a licence to construct and operate its American Centrifuge Demonstration Facility. As is the case with the planned commercial plant, the demonstration facility will be housed in the existing infrastructure of the abandoned Gas Centrifuge Enrichment Plant programme at Portsmouth. USEC will use this facility to collect cost, scheduling, and performance data that will be used both in the construction of its commercial-scale plant as well as demonstrating the economics to potential investors.

In June, USEC announced that Fluor Enterprises would provide engineering, procurement, and construction management services for the American Centrifuge plant. For the next two years, Fluor will work on the design and engineering details of the plant. In 2006, USEC anticipates an agreement between both parties on fixed-price contracts covering major construction areas with the exception of the centrifuge machines, for which a manufacturer has not yet been named.

USEC submitted a licence application to the NRC for the American Centrifuge plant on 23 August. Production is scheduled to begin at its demonstration centrifuge facility in 2005 and, if all goes well, USEC will bring the commercial plant into production in 2010. The plant is initially being scaled to produce at a target rate of 3.5 million SWU per year, but USEC notes that this capacity can be readily expanded due to the modular design of a centrifuge plant.

Key for USEC will be the successful demonstration of the American Centrifuge. It is not so much whether or not the technology will work, but rather whether it will work well enough to attract investors and thus enable USEC to raise the necessary capital to build a plant. Although the presence of a competing plant in Louisiana Energy Services’ (LES’) National Enrichment Facility (discussed next) may complicate USEC’s ability to raise funds, the fact that enrichment demand is currently showing strong growth means that there is room for two new enrichment facilities in the USA. USEC also enjoyed success in signing new long-term contracts over the past year, providing a basis for future expansion.

LES AND THE NATIONAL ENRICHMENT FACILITY

The past year has proved eventful and productive for LES in its quest to build an enrichment plant using Urenco centrifuge technology in the USA. In our article last year (see NEI September 2003, p12), we noted that LES was encountering difficulty with the local community in siting its plant in Hartsville, Tennessee. However, last September, LES announced that it was abandoning the Hartsville site and would now locate the plant in Eunice, New Mexico, and at the same time naming the project the National Enrichment Facility (NEF). In contrast to the problems it encountered in Tennessee, LES received broad state and community support in New Mexico when it opted to build there.

In December, LES submitted a licence application and environmental report to the NRC. At the same time, it announced it has enough contracts with US utilities to account for 50% of the first ten years of the plant’s output. This contract support is critical in assuring regulators of the need for the plant and convincing investors of the plant’s economic basis. In January, the NRC accepted this application and set a 30-month schedule for its review, meaning that a decision should be forthcoming in June 2006. The NRC also set forth guidelines for the Atomic Safety and Licensing Board (ASLB) to follow while conducting the hearing process, concluding that the recently amended 10 CFR Part 2 will apply to the application hearings.

In March of this year, the NRC held a public scoping meeting in New Mexico to determine issues to consider in the draft Environmental Impact Statement (EIS) for the NEF. A draft EIS is expected in late September, with a final EIS scheduled for 15 June 2005. In mid-April, the NRC accepted LES’ Quality Assurance Program Description portion of the licence application for the construction and operation of the NEF.

In July, the ASLB granted standing in the LES/NEF licensing process to the New Mexico Environment Department, the Attorney General of New Mexico, and jointly to two anti-nuclear groups – the Nuclear Information and Resource Service, and Public Citizen – as the ASLB has found that each of these groups has filed at least one admissible contention in the licensing process. A total of 32 contentions had originally been filed, but some were withdrawn before the ruling. The admitted contentions that will be addressed by the ASLB include, among others, issues dealing with a proposed radiation protection programme, disposal cost estimates, impact on water supply, depleted UF6 storage and disposal, and decommissioning costs.

The ASLB dismissed contentions related to the impact of the plant on national security and non-proliferation, but will evaluate the enrichment market to determine whether additional enrichment capacity is needed in the USA and how LES might play a role. In August, LES announced the selection of Washington Group International to work on the final design and construction planning of the NEF project. LES anticipates construction of the NEF project to begin in the autumn of 2006, with first production from the plant in winter of 2008, after which production is scheduled to ramp up to 3 million SWU.

AREVA AND GEORGES BESSE II

In last year’s article we noted that Areva had decided to base its future enrichment operations on centrifuge technology and had signed a Memorandum of Understanding with Urenco in October 2002 to use the latter’s technology for a replacement facility for the Georges Besse gaseous diffusion plant. An important step in this transition was taken in November of last year when Areva purchased a 50% share in Enrichment Technology Company (ETC), a company set up by Urenco to house all of its research and development, design, and manufacturing of centrifuges. The finalisation of this joint venture is subject to securing the proper competition clearance as well as the development of an intergovernmental agreement between the governments of France, Germany, Netherlands and the UK. Like the case with USEC’s proposed American Centrifuge plant, the new plant, called Georges Besse II (GB II) would be built on the site of a current plant, the Georges Besse I (GB I) gaseous diffusion plant at Tricastin.

The Areva-Urenco agreement deals only with the production of centrifuge machines and not the marketing of SWU, as both companies will continue to compete in the enrichment market. Still, this arrangement has raised antitrust concerns in the European Union (EU) and the European Commission (EC) is now investigating whether Areva’s planned purchase in ETC violates the EU’s competition regulations. The investigation began at the request of France, Germany, and Sweden. (Although the GB II plant will be built in France and Urenco has a plant located in Gronau, Germany, the impetus for investigation came from the consumers in these countries.) Apparently, the EC is concerned that competition could be reduced and SWU prices in Europe could rise since together Areva and Urenco currently account for 80% of the EC market, even though the companies plan to continue to market SWU separately. Another concern is that the ETC venture could reduce the incentive for Areva to conduct enrichment research and development activities. The investigation is expected to be completed by 22 October.

Current plans are for Areva to start construction of GB II in 2005 and bring the plant online in 2007. While production from GB II is ramping up, GB I would be operated at a rate of 10 million SWU per year, during which inventory would be built up. The shutdown phase of GB I would begin in 2007 and GB II would not be brought up to full production until 2016. During the intervening years (2012-2016), supply would be maintained at around the 10 million SWU level due to the drawdown of previously accumulated inventory. Further, even though the current target capacity for GB II is 7.5 million SWU per year, supply could be maintained at this higher level for some time due to the availability of additional inventory that would have been built up in the previous period. Presumably, GB II capacity could be expanded beyond this 7.5 million SWU per year rate at a later time.

Areva-Cogema has been ramping up production at GB I, with almost a 50% increase over the past five years, bringing output to a point that is much closer to the plant’s nameplate capacity of 10.8 million SWU per year. In this respect, it does not seem that the trade case (discussed separately below) has had much impact on the plant’s output. According to the US Energy Research and Development Administration, Areva-Cogema’s SWU exports to the USA increased by almost 400% over the 1998-2003 period, from 696,000 SWU in 1998 to 2.685 million SWU in 2003. Importantly, SWU exports essentially doubled between 2001, when they were 1.368 million SWU, with this occurring during a period after USEC filed the trade case.

URENCO

Like the other enrichers, Urenco has made considerable progress over the past year, a function of its involvement in the LES and ETC joint ventures as discussed earlier, and growth in its own enrichment facilities in Europe. In addition, it has made further improvements in its centrifuges, the aspect of the company that has given it a competitive advantage in the SWU market.

In October of last year, Urenco formed ETC by splitting off its enrichment design, manufacturing, research and development functions from its other enrichment businesses. Urenco Limited is now structured so it owns 100% of Urenco Enrichment Company, 50% of ETC (with Areva owning the other 50%), and 100% of Urenco Investments Incorporated that in turn owns 100% of Urenco Incorporated, the US marketing arm of Urenco, and with the parent company, 75% of LES (with Westinghouse owning the other 25%).

Through this structure Urenco is able to supply both centrifuges and sell SWU to the worldwide market. Assuming that GB II gets built with Urenco-designed centrifuges, the NEF plant gets built, and Urenco expands its European production to 7.5 million SWU as planned, Urenco centrifuges would contribute at least 18 million SWU of worldwide enrichment capacity by around 2015. Of course, capacity could be more than this, since Urenco is currently planning to achieve the 7.5 million SWU expansion in Europe by 2005, leaving ten years for additional expansion at any one of its three sites in Europe. At the end of 2003 Urenco’s capacity was around 6.5 million SWU while at the end of 2000 it was less than 5 million SWU, indicating that its capacity has been expanding at a steady clip in recent years.

Like Areva-Cogema and consistent with its expansion of capacity, Urenco’s share of the enrichment market has been growing in recent years, especially in the USA. At 2.788 million SWU, its exports to the USA just topped Areva’s for 2003. In addition, these exports have more than doubled since 2001, the year after the trade case was brought. According to the DoE’s Energy Information Administration, Urenco countries exported almost 1.3 million SWU to the USA in 2001. The penetration into the US market gives Urenco confidence of the success of the NEF plant there, confidence that is further bolstered by the commitments that it has received for future NEF output to date.

Given the modular design of its centrifuge plants, Urenco has pursued a marketing strategy where it has opted to add capacity only as it secures new contracts. While some would say that this is a conservative approach, Urenco has been able to closely match SWU capacity with contract commitments, resulting in very little, if any, excess capacity. As its customers opt for lower tails assays, Urenco will likely need to continue to expand capacity to meet this additional demand, or it otherwise would need to buy uranium to overfeed its plants.

RUSSIA

As mentioned earlier, an important function of the Russian enrichment plants is enrichment of tails material to produce blendstock for HEU feed and to produce normal uranium. A 2000 paper indicated that of the estimated 20 million SWU capacity of Russia’s enrichment plants, 5.8 million SWU was used for the production of HEU blendstock, while 2.6 million was used for the enrichment of tails to create normal uranium. Thus, about 40% of Russia’s capacity at that time was devoted to enriching tails.

Russia has the greatest enrichment capacity of any country in the world. Current plans are for the country to expand its enrichment capacity, which is marketed by the joint stock company Tenex, by 6 million SWU to 26 million SWU by 2010. While Russia is expanding its enrichment capacity, it should be noted that this is likely driven as much by the need to continue to create additional uranium supplies as to provide additional enrichment supplies. As tails assays drop, more capacity is needed to produce the same amount of uranium. Since Russia is already enriching at a very low 0.10% tails assay, it is already achieving the maximum practical substitution of enrichment for uranium that it can. Russia’s need for uranium was demonstrated by its decision to terminate its uranium feed sales agreement with Global Nuclear Services & Supply and to convince the other three HEU feed agents – Cameco, Cogema and Nukem – to relinquish their claim on so-called second options for the HEU feed, which gave them the right to buy the HEU feed after it went back to Russia.

The demand for enriched uranium on the part of Russia and its reactor export clients is also growing. Russian production of nuclear-generated electricity has increased by about 50% over the past five years, and additional increases are expected. Russia is also exporting nuclear reactors to China, India, and Iran, and is supplying fuel with these reactors. Thus, the demands on Russian enrichment to produce additional enrichment as well as uranium supplies are substantial. Like the case with Urenco and Areva-Cogema, it is thought that all or nearly all of Russia’s enrichment capacity is currently being used.

Because of the increasing demands of its own programme as well as emerging nuclear programmes in Asia, the fact that the European Union and the USA have restrictions against the import of Russian SWU might not be an important market factor in the future. Currently, Russia is limited to about a 20% share of the European SWU market and essentially has no access to the US market except through the sale of SWU by means of the HEU deal. Although it was believed to expire in March of this year, the US Department of Commerce (DoC) has said that the suspension agreement in the USA remains in place, allowing Russia to deliver the HEU SWU, which meets about half of US domestic needs.

TRADE CASE UPDATE

Over the past year, there have been a number of developments in the trade case that was brought by USEC against the European enrichers in December 2000. The net effect of these has been that antidumping and countervailing duties originally levied have been greatly reduced – or in the case of antidumping duties – potentially eliminated altogether. In September of last year, the US Court of International Trade (CIT) ruled that antidumping laws cannot apply to enrichment transactions, a ruling that, if upheld, has the practical impact of removing antidumping duties against enrichment imports from France. (The antidumping cases against the Urenco countries of Germany, Netherlands and UK had previously been dropped.) In February of this year, the CIT ruling was appealed in the US Court of Appeals for the Federal Circuit.

During the period when the CIT was considering the appeal of the DoC’s initial ruling in the trade case, the DoC was also conducting an administrative review of both the antidumping and countervailing cases on which it originally ruled. These reviews can be requested on an annual basis by interested parties in the case. The final determinations of these administrative reviews had the result of the DoC sharply dropping the antidumping duty against France from its original level of 19.95% to 5.43% and dropping the countervailing duty against France from the original 12.15% to 3.63% for the year 2001 and 0.71% for the year 2002. There were also slight downward adjustments to the countervailing duty against the Urenco countries, but the original duty was quite small (2.23%) to begin with. The current countervailing duty going forward is 0.71% from France and 0% for the Urenco countries because any benefits of the previous subsidy had already been accounted for. The next adjustment to the duties could occur after the completion of the next administrative review in 2005.

As mentioned earlier, the trade case had the initial impact of sharply increasing SWU prices (see Figure 1). However, since the time that USEC filed this case, the US dollar has weakened considerably against the Euro, meaning that European enrichers would have had to raise their dollar denominated prices anyway if they were to keep prices at the same Euro equivalent as before. Also, in retrospect, a higher price level was necessary to support the new enrichment plants proposed for construction in the USA. And, as previously mentioned, both Urenco and Areva were able to expand their exports to the USA despite the existence of the trade case and the duties it precipitated. Thus, the prospect that the duties spawned by the trade case will be phased out is likely not to have much impact on the market.

CHALLENGES REMAIN

Considerable progress has been made over the past year to move the three proposed centrifuge plants – two in the USA and one in France – closer to reality. Also, the existing centrifuge complexes run by Urenco and the Russian government are in the process of expanding their capacity to meet growing needs in the markets that these enrichers supply. After increasing in 2001 following the filing of the trade case, SWU prices have held firm, and have even shown some additional strength recently. Thus, a solid basis appears to be in place to support production going forward.

However, challenges remain and these supply additions are far from guaranteed. Issues of technology, financing, licensing, public acceptance, and competition compliance affect the proposed projects to varying degrees. Developments over the next year should bring a clearer picture if any of these problems are insurmountable. The EC is expected to rule in October on any antitrust issues involved with the Urenco-Areva joint venture. This seems to be the only possible impediment for the GB II plant, which has the support of the French government. USEC should have a better idea of the success of its centrifuge design and operating capability. And, by this time next year, LES should be two-thirds the way through its licensing process with the NRC.

One challenge of another sort that has become more apparent recently is the growing demand for enrichment, a product of both the growth in nuclear power capacity and the movement to lower tails assays, the latter spurred on by increasing uranium and conversion prices. Since enrichment capacity and requirements are in a relatively close balance now, any growth in requirements that exceeds the planned growth in capacity will place additional stress on enrichment supplies. We are possibly seeing the beginning of that stress today, but that picture will also become clearer over the next year, as the trend in nuclear power additions and uranium price movements evolves.

Author Info:

Jeff Combs, Ux Consulting, 1401 Macy Drive, Roswell, Georgia 30076, USA