WORLD SURVEY

The end of decline

31 August 2005In previous editions of the US Energy Information Administration’s International Energy Outlook, a decline in nuclear power before 2025 was projected. The latest edition tells a different story.

The year 2020 has clearly caused a lot of problems for the US Department of Energy’s (DoE’s) Energy Information Administration (EIA), at least when it comes to worldwide nuclear capacity.

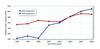

Last year, NEI noted the phenomenal upward revisions in recent editions of the EIA’s International Energy Outlook (IEO) for installed nuclear capacity in 2020 (see NEI June 2004, p33). The 2002 edition of the report (IEO 2002) predicted some 359GWe of nuclear capacity for that year – around 8GWe higher than the IEO 2001 projection, but a staggering 56GWe higher than in IEO 2000. In the two editions that followed, nuclear capacity in 2020 continued to ‘increase’ to around 382GWe in IEO 2003 and 401GWe in IEO 2004. Now, the 2005 edition projects a total of 411GWe of installed worldwide nuclear capacity in 2020 (see Figure 1) – a mere 108 nuclear plants with an average capacity of 1000MWe more than envisaged five years ago!

Figure 1: Changes in world nuclear capacity projections

Even more significantly, whereas past editions of IEO projected declines in nuclear capacity in the mid term, in the IEO 2005 reference scenario the total world nuclear capacity does not decline before 2025. According to this scenario, electricity generation from nuclear power plants around the world is projected to increase from 2560TWh in 2002 to 3032TWh in 2015 and 3270TWh in 2025, and the world’s nuclear-powered generating capacity is projected to increase from 361.2GWe in 2002 to 390.1GWe in 2010, 400.7GWe in 2015, 411.0 in 2020, and to 421.8GWe in 2025. Compare these figures to IEO 2004, where the increase in capacity was assumed to be greater at first, reaching 407GWe in 2015. Thereafter, nuclear was projected to decline, with 401GWe in 2020 and only 385GWe in 2025. What a difference a year makes!

In other sectors, differences between last year’s IEO and this year’s are striking. The IEO 2005 projections are higher than the IEO 2004 projections for each energy source, largely as a result of the unanticipated strong expansion of energy demand in recent years. This year’s reassessment of the near-term forecast is so profound relative to last year’s forecast that the IEO 2004 projections for every fuel type except oil fall below those in the IEO 2005 low economic growth case.

As far as nuclear’s apparent reversal of fortunes is concerned, IEO 2005 attributes this to the fact that, in past editions of the IEO, it was envisaged that few new reactors would be built and that older reactors would be shut down when they reached the end of their operating lives. It is worth noting, however, that those familiar with the nuclear industry have for several years been expecting most (if not all) US units to apply for licence renewals. In addition, the new build plans – particularly in the Far East – have been on the table for quite some time.

PAST PERFORMANCE

IEO 2005 looks at past performance of previous reports, comparing actual historic levels with IEO projections. It suggests that the main reasons for discrepancies between projected and actual data are to do with unpredictable political and social changes. For example, the political and social upheaval in the EE/FSU (Eastern Europe/Former Soviet Union) region dramatically affected the accuracy of earlier IEO projections for the region. In the case of China, had higher economic growth rates been assumed, more accurate forecasts for that region might have been achieved. Failing an ability to predict future volatility in social, political, or economic events, the projections should be viewed as a plausible path or trend for the future and not as a precise prediction of future events.

Within this context, IEO 2005 makes special note of the difficulty in predicting future nuclear capacities. For example, forecasts for the year 2000 for oil, natural gas, and hydropower and other renewable energy sources were generally higher than actual levels. In contrast, projections for nuclear power – even as late as IEO 1999 – were consistently lower than the actual 2000 values.

The pessimism towards nuclear leading up to the millennium is put down to the aftermath of Chernobyl and the problems associated with nuclear waste disposal. In the political climate of the early1990s, it was not possible to anticipate the life extensions and consistently improving efficiencies that have allowed nuclear power plants to generate more electricity and operate with shorter downtimes for maintenance, even without expanding their installed capacities.

Interestingly, the report notes that the underestimation for the year 2000 is largely down to the forecasts for the USA. And a glance at the US projections in this year’s report show that the EIA still maintains a considerable level of doubt towards there being a new nuclear build programme in its own country. IEO 2005 projects that installed nuclear capacity in the USA will increase from 98.9GWe in 2002, to 100.6GWe in 2010, 102.2GWe in 2015, and to 102.7 in both 2020 and 2025. So, not much hope of success for the DoE’s Nuclear Power 2010 programme then!

ALTERNATIVE SCENARIOS

Two opposing alternative nuclear scenarios are presented in IEO 2005 (see Table on next page). In the ‘strong nuclear power revival’ case, few nuclear plants are retired, and new builds increase the world’s total nuclear generating capacity to 570GWe in 2025. In contrast, the ‘weak nuclear power’ case assumes that nuclear power programmes, especially in Western Europe and the EE/FSU, are dismantled, few new plants are constructed, and installed nuclear power capacity falls to 297GWe in 2025.

It would seem that the EIA didn’t feel up to the challenge of coming up with projections for future US nuclear capacities in both the ‘weak nuclear power’ case and the ‘strong nuclear power revival’ case, leaving the projections in these upper and lower scenarios the same as for the reference scenario. This is unfortunate because it would have been interesting to see whether and by how much the EIA projects US nuclear capacity to increase in the strong revival case. In addition, given the impact that the US capacity projections have on the worldwide total, such an omission renders the overall figures in the outer scenarios almost meaningless.

It is possible that the EIA might not have wanted to risk making projections that depended almost exclusively on whether or not the energy bill would include crucial nuclear provisions. The bill was clearing its final stages at exactly the same time as IEO 2005 was published. However, it has been obvious for some time that the provisions encouraging new nuclear are among the least controversial in the bill and were likely to go through in some form sooner or later. And, in any case, such an argument could be applied to provisions pertaining to other sources of energy. Now that the energy bill has been passed, the projections in the next IEO report for all sources of energy in the USA will make very interesting reading.

Some indication about the EIA’s view on a possible new build programme in the USA can be found in its Annual Energy Outlook 2005 (AEO 2005), which was released at the beginning of this year. As in the IEO 2005 projections, the AEO 2005 reference case does not expect any new nuclear units in the USA to become operable before 2025. A capacity increase totalling 3.5GWe by 2025 is however projected, but this is due to other factors such as uprates, rather than new plant.

The EIA reaches the conclusion that there will not be new nuclear build because it believes that electricity costs for new nuclear will be higher than for combined cycle gas, coal and even wind.

However, AEO 2005 presents two alternative nuclear cost cases that analyse the sensitivity of the projections to lower costs for new nuclear plants. The ‘advanced nuclear cost’ case assumes capital and operating costs 20% below the reference case in 2025, reflecting a 28% reduction in overnight capital costs from 2005 to 2025. (Earlier analysis showed that a 10% reduction in capital and operating costs would be insufficient to stimulate new nuclear construction.) The ‘vendor estimate’ case assumes reductions relative to the reference case of 18% initially and 38% in 2025. These costs are consistent with estimates from Westinghouse estimates for its AP1000 design.

Projected nuclear generating costs in the two alternative nuclear cost cases are competitive with the generating costs projected for new coal and natural gas fired units towards the end of the projection period. In the ‘advanced nuclear cost’ case 7GWe of new nuclear capacity is added by 2025, and in the ‘vendor estimate’ case 25GWe is added by 2025.

RISE AND FALL

Turning back to IEO 2005 and, looking closer at the projections for the nuclear industry, in amongst the overall positive picture, there remain regions of concern. In the mature market economies, the IEO 2005 reference case assumes that, in the long term, retirements of existing plants as they reach the end of their operating lives will not be balanced by the construction of new nuclear power capacity, and there will be a slight decline in installed nuclear capacity towards the end of the forecast period (the year 2025). Few new builds are expected in the mature market economies outside of Japan, France, and Finland.

Figure 2: World nuclear power generation capacity by region

Western Europe’s nuclear capacity is projected to drop from 127GWe in 2002 to 115GWe in 2015 and 95GWe in 2025. In Japan, however, nuclear capacity is projected to expand by 9GWe between 2002 and 2025. As noted earlier, US nuclear capacity is projected to increase from 99GWe in 2002 to 103GWe in 2025, in part because of the return of Browns Ferry 1, scheduled for 2007. Life extensions and higher load factors are expected to play a major role in sustaining the US nuclear industry.

In contrast to the mature market economies, rapid growth in nuclear power capacity is projected for Russia and for the world’s emerging economies (see Figure 2). The EE/FSU and emerging economies combined are projected to add 42GWe of nuclear capacity between 2002 and 2015 and another 35GWe between 2015 and 2025. Over the forecast period, the largest additions of nuclear capacity are expected in emerging Asia (China, India and South Korea), and in Russia. China is projected to add 24GWe of nuclear capacity in the IEO 2005 reference case, India 12GWe, South Korea 12GWe, and Russia 14GWe.

Although the overall worldwide picture shows nuclear capacity increasing throughout the forecast period, the role of nuclear power in the world’s electricity markets is projected to lessen. In the IEO 2005 reference case, continued increases in the use of natural gas for electricity generation are expected worldwide. Coal is projected to continue to retain the largest market share for electricity generation, but its importance is expected to be moderated somewhat by a rise in natural gas use. Generation from hydropower and other renewable energy sources is projected to grow by 54% by 2025, but their share of total electricity generation is projected to remain near the current level of 18%.

FilesWorld nuclear capacity by region, reference case World installed electricity generation capacity for three nuclear cases