FUEL & FUEL CYCLE

History as prelude: the outlook for uranium

21 December 2004We are currently entering a new phase in the uranium market, facing the first major change in market fundamentals in two decades, one with challenging implications for fuel production and utility procurement. It is not an understatement to say that we have failed to prepare for these changes. By Thomas L Neff

Uranium prices have recently reversed a 20-year decline, apparently surprising many buyers and sellers, most of which did not experience what is in fact a long history of substantial changes in uranium prices.

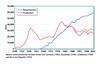

A long-run history of uranium prices is shown in Figure 1. Prices are in constant 2004 US dollars, that is, corrected for inflation. It is best to look at exploration, production and other cost factors in uranium supply in terms of real purchasing power.

The history is broken into three periods:

- 1940-1969: Weapons procurement.

- 1970-1984: Inventory accumulation.

- 1985-2004: Inventory liquidation.

WEAPONS PROCUREMENT ERA

The first reported uranium price data was for US Atomic Energy Commission (AEC) purchases, beginning in 1947. While the AEC purchased uranium before this (primarily small stockpiles from Canada and the Belgian Congo), it was only in fiscal year 1948 that the AEC listed a ‘posted price’ that would be paid to producers who delivered uranium to government buying stations.

The AEC increased or reduced the posted price as necessary to bring forth the amounts of uranium it wished to purchase for its weapons programme. In this sense, the early price data gives an example of how production of uranium responded to price, at least in the geologic environments of the time. The average price for AEC domestic US procurements during this period was $42.59/lb ($111.28/kgU) in constant 2004 dollars. The prices for foreign procurements were generally higher than those in the USA, $56.62/lb ($147.94/kgU).

Figure 2 illustrates the relationship between posted price and production in the AEC purchase programme. In effect, the AEC was jump-starting the uranium mining industry by posting relatively high prices when production was low, and then lowering prices as production increased to levels that gave the government what it wanted in terms of production flow. We face a similar problem today in that uranium production capacity is far below the level needed.

The peak in Cold War production was reached more than a decade after the purchase programme began. The lag time between the peak in price and the peak in production was seven years. This was accomplished in an era in which there were essentially no regulatory or other time-consuming impediments, and when uranium deposits were relatively easy to find through surface manifestations.

At the end of this period, a wave of civil reactor orders encouraged producers to continue, as did financial support from governments. The USA stopped buying abroad, closed its borders to imports and implemented a ‘stretch-out’ of AEC procurements from domestic producers. The Canadian and Australian governments paid to create domestic stockpiles. For example, the Canadian government financed a 6500tU stockpile for Eldorado, a stockpile that was later ‘privatised’ along with the company. Some of these inventories entered the market later, adding to supply.

The amounts of uranium originally accumulated by western governments in this era are shown in Table 1. Total western production through 1969 was nearly 337,000tU. Of this, about 70% was purchased by the USA and 4% was reported purchased by commercial parties. About 87,000tU went into British and French stocks or cannot be otherwise accounted for. Some of the government inventories were used — through loans, leases, or outright gifts — for early nuclear power plants. We estimate that between 30,000 and 80,000tU of production prior to 1970 eventually was used in civil power plants. This will be important when we look at how inventories from prior eras affected uranium production and prices in a much later period.

COMMERCIAL INVENTORY ACCUMULATION ERA

Until the late 1960s, it was generally the case that private parties could not or did not own uranium; it was even illegal in the USA until 1967. But the late 1960s saw the first significant orders for civil nuclear power plants, and the beginnings of commercial demand for uranium. At the time, production capacity for uranium greatly exceeded uranium requirements for actual plants, but needed to expand if early expectations for a rapid growth of nuclear power were to be realised.

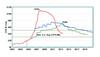

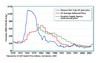

The history of western production since 1947 is shown in Figure 3, along with estimates by the World Nuclear Association (WNA) of commercial reactor requirements. The early production numbers are based on research done for my 1984 book, The International Uranium Market.

Looking ahead, the production figures in the 1990s include uranium sold into western markets from former producers in the Soviet Union, from the date at which deliveries to the West began.

Nuexco began publishing an ‘exchange value’ or the company’s estimate of current uranium price in August 1968 (the company only began reporting transaction data — the ‘transaction value’ — in 1976).

The commercial era began with severely depressed prices. The historic low was reached in January 1973, at $20.90/lb ($54.60/kgU) in constant 2004 dollar terms.

As has recurrently been the case in the commercial history of uranium, expectations have proven more important than reality in setting uranium prices. In the late 1970s, the newly-reported spot uranium price rocketed upward, despite the fact that production was expanding even more rapidly than actual near-term requirements. The price reached a peak of nearly $110/lb U3O8 ($287/kgU) in September 1976.

By late 1980, the constant dollar spot price had fallen to half this level as production peaked and more realistic expectations about nuclear growth prevailed in the wake of reactor cancellations and the Three Mile Island accident. By July 1988, the spot price fell to the low it had reached in 1973, 15 years earlier.

Of course, the spot price is not the whole story, as most deliveries occur under long-term contracts, some of which have prices not linked to spot prices at the time of delivery.

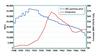

Figure 4 shows the average prices reported by the Euratom Supply Agency since 1980, and the US Average Delivered Price since 1970. As is evident, long-term contracts evened out the prices paid over time. Note that until about 1986, Euratom utilities paid less than US utilities, a situation that was later reversed. This reflects a greater emphasis on shorter-term contracts and spot-indexed contracts in the USA.

As noted earlier, it is remarkable that prices rose so significantly during a period in which uranium production significantly exceeded reactor requirements. Utilities were effectively buying at high prices for inventory, despite the fact that commercial users went into the period of rising prices with more than two years’ supply on average. In the USA for example, commercial inventories totalled more than 15,000tU at the end of 1974, before the price rise, or more than two years forward reactor requirements at the time.

This pattern has been common in energy crises. Indeed, detailed analysis of the 1973-74 and 1979 oil crises shows that the short-term reductions in supply paled in comparison with the substantially increased demand for inventories — these crises were largely demand driven.

What is also interesting about this period is the rapid increase in uranium production, as shown in Figure 4, with production doubling in only about four years. One might take this as a sign that higher prices today will quickly result in rapid increases in uranium production. However, close examination of the data for the late 1970s reveals that much of the increase in output then came from production centers — in the USA, Canada and South Africa — that had previously produced similarly large amounts of uranium for weapons programmes. The production increase in the 1970s in response to high prices can thus largely be seen as a rebound in known production centres.

The exceptions were a steady increase in production in France, Gabon, and Niger, which had suffered little reduction in the period of low prices, and the startup of Namibia’s Rössing mine in 1976, ten years after Rio Tinto acquired an interest in the deposit during the first large wave of reactor orders.

During this inventory accumulation era, cumulative production exceeded cumulative requirements by a total of 170,000tU, with this material going into industry stocks. At least 30,000tU, and perhaps as much as 80,000tU, of the production prior to 1970 is estimated to have ultimately gone into the commercial sector, directly or through government hands, making the total surplus in the inventory accumulation era greater than 200,000tU, and perhaps as much as 250,000tU.

As summarised in Table 2, US commercial inventories totaled 71,000tU as of the end of 1984, according to US government surveys. This implies that between 130,000tU and 180,000tU of commercial inventories were held in Asia and Europe as of the beginning of 1985.

INVENTORY LIQUIDATION ERA

In 1985, western uranium production fell below reactor requirements for the first time in history and has continued far below consumption for nearly 20 years.

The imbalance between production and requirements was shown in Figure 3. Note that since the early 1990s, supply to the west has been augmented by production from suppliers in theformer Soviet Union; without such supply, the gap between production and reactor requirements would have been even larger. However, Russia lost a similar amount of supply, meaning that the country would need to secure new uranium supplies, presumably from western sources or from its own HEU feed material.

Using the data in Figure 3, cumulative requirements since 1984 are calculated to have exceeded cumulative production by a total of 339,000tU as of the end of 2003. Where has this 339,000tU come from?

It is clear that this deficit has not been made up entirely by commercial inventories accumulated during the previous market phase, as we would have run out some years ago.

Moreover, commercial inventories have not been fully exhausted worldwide, though the USA has come close. At the end of 1984, US commercial inventories stood at nearly 71,000tU. At the end of 2003, US stocks totalled 32,600tU. However, during this period 28,600tU were transferred by the US Department of Energy (DoE) to the US Enrichment Corporation (USEC) and came to be counted as commercial inventory. Without the transfers to USEC, US inventories would be only about 4000tU. The US supply system is thus running nearly on empty, with a significant fraction of remaining inventory held by USEC.

We do not have similarly good data for inventories in Asia and Europe but we do know that inventories have declined since 1984. Fuel loadings reported by Euratom were greater than deliveries to utilities by 44,500tU between 1985 and 2003, implying a substantial drawdown of inventories. We believe that Asian stocks declined by a similar amount, with some acceleration in the past few years.

The WNA estimated that European and Asian stocks at the end of 2002 totalled some 90,000tU, based on survey data and extrapolation, though Euratom stocks appear to have declined by more than 4000tU in 2003, and Asian stocks by more than this. If so, current non-US inventories are of the order of 80,000tU.

The changes in commercial inventory are summarised in Table 3. The net reduction in commercial inventory is not enough to cover the 339,000tU deficit in production relative to requirements. It is thus necessary to look for other material that helped fill the gap between requirements and production.

One source was Russian HEU feed. However, the total entering western markets through 2003 was less than 20,000tU — the remainder was purchased by the US government or returned to Russia.

Perhaps the largest source of feed material consisted of trader-intermediated sales of Russian uranium beginning in the late 1980s. The WNA estimates that the total volume may have been as large as 150,000tU. Indeed, such large volumes would be necessary to explain how supply has been able to meet demand.

Table 4 summarises our estimates of how the production deficit was made up, taking into account inventory drawdown, HEU feed, re-enriched western tails (RET), and MOX. The remainder unaccounted for is 139,000 to 189,000tU, depending on assumed pre-1970 production transferred to the commercial sector. The WNA estimate of Russian supply to the West in the late 1980s and 1990s of 150,000tU is about what is needed to balance the supply-demand picture.

OVERVIEW OF PRICE HISTORY

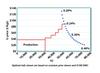

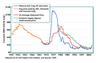

Figure 5 summarises the price history for the past five decades. Note that prices for most of the uranium delivered during this period were significantly higher than those prevailing today. Note also the similarity between long-term prices in the 1970s and early 1980s to the prices paid by the AEC much earlier.

Figure 6 gives the average prices for our chosen time periods. As reported above, the AEC paid the equivalent of $42.59 (domestic US production) and $56.62 (non-US) per pound.

The average commercial spot price over the whole reporting period was $32.04, but during the period in which supply came almost entirely from production, the average was far higher, at $54.18/lb. It was only during a period in which huge quantities of inventory — western and Russian — were sold that the average fell to $14.57/lb.

The Euratom data series began only in 1980, but displays similar characteristics. During the period in which supply came from production, the average multi-annual price was $57.37/lb. During the period of inventory liquidation, the average was $27.45. The average for the entire period was $33.68/lb.

The average US delivered price averaged $31.46/lb over the whole reporting period. However, this was an average of a period in which supply came from production (in which the average was $48.13/lb) and a period in which supply and price formation were dominated by inventory sales (where the average delivered price was $20.92/lb).

What is remarkable about these figures is the long-term average price of about $32/lb independently of the data series chosen, and the average of $48/lb to $57/lb for the periods in which production was the primary determinant of price. There is considerably more variation in prices during the inventory liquidation period.

In looking at the future of uranium prices, it is helpful to keep these figures in mind.

PRICE FORMATION

The term ‘price formation’ refers to how price is set in a market. In the weapons procurement era, price formation was very simple: government set whatever price was needed to bring forth supply. As we saw earlier, this price increased in early years and then declined as sufficient production came into existence.

“” |

In effect, the mistake made in pricing uranium has created a crisis across the fuel supply system |

The situation in the inventory accumulation era was much more complex: A wave of reactor orders in the late 1960s; US government demands that utilities sign up for enrichment contracts before the order books were closed; the Westinghouse default; and efforts by governments of producing countries to assure higher prices – the so-called cartel – all contributed to the rapid increase in price.

As noted earlier, price formation in this period had little to do with production or actual reactor requirements and much more to do with what turned out to be mistaken expectations. In fact, there was no shortfall of uranium, just the perception of one. Moreover, inventories were not only adequate but grew during the period.

Price formation since 1984

The situation today is almost the exact opposite: there is an actual shortfall of uranium production capacity and inventories have been drawn down to dangerous levels, especially in the USA. Nevertheless, expectations have been for continued supplies from inventory and low prices.

Price formation since 1984 has been driven by expectations of continued surplus and low prices. These expectations have led inventory holders to sell far below replacement cost from primary production. Instead of looking at what production might cost from the marginal mine — the highest cost mine needed to supply the last units of demand — inventory sellers have instead looked at the lowest cost mines. In turn, the owners of the low cost mines have competed to sell well below long-run marginal cost for the industry as a whole.

Let us look at this situation more analytically. Figure 7 illustrates how a market, based on production rather than inventory sales, operates to produce a market price. On the right we show the demand curve: the amount that will be purchased at different price levels. In the case of uranium, the only way to vary the amount of uranium purchased is to vary the tails assay in enrichment. At higher uranium prices, a utility will reduce tails assay and purchase less uranium (assuming that SWU prices do not rise). Figure 7 uses the WNA reference case requirements, but recalculates the amount of uranium required at alternative tails assays. The WNA reference case has western requirements of about 59,000tU at a western average tails assay of about 0.31%. This is lower than the optimal tails assay for published uranium and SWU prices at the time of the estimate, which was closer to 0.34%. At the latter tails assay, uranium requirements for the reference case would be about 63,000tU.

In a market balanced between production and requirements, this demand curve will intersect a production supply curve. Different mining centres will have different costs of production and one places them on the supply curve in increasing order of cost. The market price will be the cost of the last bit of uranium needed to satisfy requirements. In Figure 7, the 2003 western production (including central Asia) of about 31,000tU has been lumped together as being producible at or below $35/kgU (as UF6), since this volume was actually being produced at the price level prevailing then.

If there were no long-term inventory liquidation, uranium prices would be higher, at the level of the marginal mine cost. And with higher uranium prices, the tails assay in enrichment would be lower, as would uranium demand. Figure 7 thus provides a dynamic way of looking at supply and demand, with demand adjusting to a higher or lower tails assay depending on the cost of marginal uranium supply.

However, with large-scale inventory liquidation, price formation has been quite different, as shown in Figure 8. In effect, sellers of inventory material sold at prices to compete with the lowest cost producers remaining in business, rather than at the higher replacement cost shown in Figure 7. If one assumes that the production-based price should have been the historical average of about $90/kgU, inventory sellers in 2003 gave up more than $50/kgU in potential profits, for a total opportunity cost of more than $1.5 billion. Producers gave up a similar amount.

Most inventory has been sold on a spot basis. The spot price has thus largely been the inventory liquidation price, rather than the price at which (hypothetical) marginal mines might sell to replace such material. Unfortunately, long-term contract prices for primary production have been linked to spot prices, either directly through indexing or by choice of base or ceiling prices. As a result, current uranium deliveries are at prices that do not reflect the scarcity of uranium but rather are embedded prices from an era of inventory liquidation. This preserves the appearance of low prices for longer than should be the case.

The net result of nearly 20 years of inventory liquidation is that existing higher-cost suppliers were driven out of business, new mines were discouraged from starting, and exploration was neglected. The mines shown in Figure 7 do not exist and most are not even discovered yet. Unlike the situation in the 1970s, when mines active in the weapons programmes could simply ramp back up in production, there is little left to revive now.

To the extent that there is still some inventory to sell, and a need to sell on the part of some players, spot prices should lag behind new long-term contract prices from primary production. The latter should go up faster than spot prices, but will be less apparent to the market.

FILLING THE GAP

In April 2003, I presented a paper at the Nuclear Energy Institute Fuel Cycle 2003 meeting in Baltimore, Maryland, USA entitled Long-term supply: No field of dreams. This talk called attention to the deficit in primary uranium supply, the role of the inventory bubble in decimating uranium production, defects in price formation, myopia on the part of industry participants, and the lack of redundancy in the whole fuel cycle system and its susceptibility to disruption. I also said prices would inevitably go up and when this started, remaining inventories would freeze in place, accelerating the price rise.

Well, we appear to be there now. The question is where to go from here.

There are several alternatives that might help fill the gap between primary production and requirements:

- Increase enrichment capacity and substantially reduce tails assay.

- Expand production of uranium.

- Draw more on Russian or western government inventories.

I have found a new way to do so, with a chart that plots western enrichment requirements against western uranium requirements, at various tails assays. The chart allows us to see how various combinations of SWU and uranium might be used to meet western reactor requirements, now and in later years.

An example of this approach is shown in Figure 9. Uranium requirements are plotted along the horizontal axis and SWU requirements along the vertical axis. The leftmost curve shows the various combinations of SWU and uranium that meet the 2003 WNA reference requirements for western reactors. Each data point is a different tails assay, as indicated by the intersecting lines. The rightmost curve represents SWU and uranium combinations that meet the WNA reference case for the year 2020.

In Figure 9, the ‘X’ in the lower left corner represents current western production of uranium and SWU. This clearly does not reach the requirements curve. The challenge we face is to find a combination of additional uranium and SWU that gets us to one of the points on the requirements curve.

We can get there by using any number of different combinations of uranium and SWU. Note however, that we cannot reach the requirements curve by using more SWU, or more uranium, alone. Trying to do so would require going below 0.10% tails assay, in the case of a SWU-only solution (which is technically impossible due to exponentially diminishing returns), or above 0.40% tails in the case of a uranium-only solution (there is not nearly enough uranium to get there).

How then was enough enriched uranium product produced in 2003? The answer is in Figure 10. First, the West used about 9000tU plus about 7.5 million SWU from Russia — from the HEU deal, direct exports, tails upgrading, and other mechanisms. This gets us closer to the requirements curve, but not all the way there.

Note that the effective tails assay for this mix of supply is about 0.20%, largely because Russia operates at far lower tails assays than the West but also because western enrichers are effectively operating below 0.30% tails assay (returning uranium to the market), by underfeeding or by sending tails to Russia. That is, without inventory use, the effective tails assay would be quite low, if one had to use existing western uranium and SWU production levels.

As shown in Figure 10, the remainder of the supply — nearly 20,000tU — came from western inventories, largely in the form of natural uranium, as shown by the horizontal line in Figure 10. The overall combination of supply results in meeting western requirements with about 30.5 million SWU and 59,000tU at an average tails assay of 0.31%.

It is very difficult to see what will replace the uranium inventory liquidation that allowed us to meet the requirements curve in Figure 10. We need substantially more supply of both uranium and enrichment. To reach the closest point on the 2003 requirements curve would require about 8 million additional SWU and 8000tU additional uranium, even with large volumes continuing to come from Russia.

Effects of uranium under-pricing

Two decades of uranium inventory liquidation at low prices has distorted both uranium and enrichment markets. Uranium production is half of western requirements and there is not enough production capacity in the pipeline to replace inventory use. But uranium pricing mistakes have also affected enrichment.

In effect, low prices for uranium inventories resulted in a relatively high average tails assay for the overall supply system. This has given misleading signals to the enrichment sector, which should have expanded capacity far sooner, to make better use of remaining uranium inventories and the uranium production remaining. If uranium had been properly valued, there would have been higher demand for SWU to operate at lower tails assay and conserve uranium and SWU capacity should have expanded sooner.

In effect, the mistake made in pricing uranium — valuing it far below its replacement cost — has created a crisis across the fuel supply system. There has not only been inadequate investment in uranium, in exploration as well as production, but also in enrichment capacity. As several fuel cycle suppliers have commented, low prices have also led to cost-cutting on repairs and maintenance, making existing supply more fragile and susceptible to disruption.

Existing western facilities can probably be expanded modestly — a few thousand tonnes each of uranium and SWU — but this will not be enough to meet today’s requirements curve shown in Figure 10, let alone catch up with the outward movement of this curve over time.

There are plans for new centrifuge enrichment plants, but these will not even replace the capacity of the diffusion plants that will be shut down.

Russia

Russia is already contributing substantially to western supply, but its own needs are growing. Russia is already making up for its own growing deficit in uranium supply with enrichment—by re-enriching tails and reprocessed uranium. Higher capacity factors, reactor completions, and new export business, as well as blendstock for HEU, seem likely to continue to make full use of the Russian enrichment capacity.

Both Russia and China seem likely to put increasing demands on western uranium supply, rather than contributing to it.

The end of the HEU deal, only nine years from now, may free up Russian enrichment capacity now being used to make blendstock, with only a small net reduction in enrichment supply to the West. However, it will be very difficult to replace from production the uranium supply coming from Russian HEU.

Government inventories

Many will look to governments to solve the supply problem by freeing up additional inventories of uranium and SWU. However, there are at least two problems that limit near-term contributions to western supply.

Firstly, it will be difficult for either the USA or Russia to reach political decisions to sell more material. The USA has declared about 174t HEU surplus, but seems unlikely to make more available for strategic military and naval reactor reasons. Russian imperatives include strategic fuel supply as well as military requirements.

Secondly, such military material requires substantial processing to remove contaminants and dilute and make it into fuel, and there is limited capacity to do so at a significant rate. Most of the capacity is already occupied processing material already assigned to commercial use. I estimate that US processing of HEU is equivalent to about 1100t uranium, 630t SWU, per year (much of this is included in the inventory balance calculations above).

Like new mines or enrichment plants, there is a substantial lead time for bringing new government inventories to market, and the rate of flow is similarly constrained.

There is an important downside to uncertainties about government inventories, just as there was from uncertainties about commercial inventory drawdown: such uncertainties discourage investment in new primary production for uranium and enrichment, leading to a potentially disastrous market failure. The only way out of this dilemma is for governments to be very clear about their plans, and for primary production of either uranium or enrichment to be baseloaded with firm contracts.

PRICE OUTLOOK

If in fact the commercial inventory drawdown is effectively over, we will need to make a transition to a production-based supply system in which prices reflect long-run marginal costs. As we have seen from our analysis of historical prices for uranium, this may be considerably higher than prices during the period in which inventory dominated price formation. Historically, such prices have been in the $30/lb to $50/lb range. The ultimate level depends on a complex tradeoff between expansion of geologic and engineering knowledge and skills, and the higher and uncertain costs of finding and developing new deposits.

The more immediate question is whether the transition to a production-based uranium price will be smooth. Unless there is still substantial inventory that people are willing to use (those with such inventory are unlikely to part with it now), analysis suggests that prices may temporarily overshoot, as they did in earlier periods.

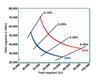

To provide an idea of what this might entail, we take the price curves from the 1940s and the 1970s and add them to the recent price curve, as shown in Figure 11. The US average delivered price for 1974-1988 is also included.

The upward part of the 1940s curve reflects the time and cost of real mining investments, though it should be remembered that peak production lagged behind the price peak by seven years in the 1940s example. Moreover, there was a target amount of uranium needed for weapons. Prices fell when this was eventually met. In the commercial parallel, it is likely that requirements will continue to rise indefinitely.

The 1970s price spike represented something closer to panic, something that is not out of the range of possibility today. The downside to running out of uranium for a reactor is the cost of replacement power, something that is far more expensive than nuclear fuel. The price spike in the late 1970s was limited because production from previous centres could quickly ramp back up and because commercial inventories became very large, allowing buyers to back away from the market. This is not the case today and a longer period of high prices could prevail.

The last curve in Figure 11, the average US delivered price for 1974-1988, indicates how existing long-term contracts might modify average acquisition prices for uranium. Many current contracts include ceiling prices that could result in a curve similar to that from the historical period shown.

The long-term picture for nuclear fuel supply looks good: uranium resources are not a serious issue and enrichment capacity can be expanded. The problem is the one to two decades that will be needed to expand capacity and build the flow of nuclear fuel up to levels that meet the expanding requirements horizon in Figure 10.

Author Info:

Based on a paper presented to the Nuclear Energy Institute ‘International Uranium Fuel Seminar 2004’ held on 10-13 October 2004 in Florida, USA. Thomas L Neff, Center for International Studies, Room E38-600, Massachusetts Institute of Technology, 77 Massachusetts Avenue, Cambridge, Massachusetts 02139-4307, USA

Related ArticlesAreva signs mining deal with Congo| Neff pq |

| In effect, the mistake made in pricing uranium has created a crisis across the fuel supply system |