Fuel review: supply

Entering a new era

27 August 2004The international uranium market has recently been evolving from a buyer’s market into a seller’s market. By Julian Steyn

The most notable recent change in the uranium market has been the doubling of the spot market price since mid-2001, with approximately three-quarters of the increase occurring during the past year. The causes of the increase have been a series of events ranging from a fire in an Australian uranium processing facility to a flood at a Canadian mine; the commercial supply dispute between two Russian entities that resulted in a uranium supply interruption to a significant number of mostly US utilities; the more than half a year interruption of production at the only American uranium hexafluoride (UF6) conversion services production plant; and the realisation by the industry that the domestic and international nuclear fuel cycle front end is very vulnerable to supply interruption. In addition, there has been an industry-wide realisation that even with substantial and varied stocks of already-mined uranium (AMU) currently identifiable supply may be unable to meet requirements by the end of this decade.

The market is concerned about the possible loss of important supply sources during the next ten years. The owner of the large Rössing mine in Namibia has plans to shut down the mine in 2007 if it does not obtain customer commitments to offset the substantial capital investment that would be required to continue production through at least 2015. In Australia, the same owner has agreed to put the large Jabiluka uranium deposit under an indefinite long-term care and maintenance agreement and only develop it at some appropriate future time with the approval of the traditional native people of the region. The underground workings and access decline were backfilled in 2003, and some related rehabilitation work has already taken place.

There is concern that the uranium feed component of Russian highly enriched uranium (HEU) will not be available to the Western market after the current agreement with the USA expires in 2013, that is, there may be no HEU II. In fact, Russia recently reduced the amount of feed available to its Western marketing agents.

As the substantial stocks of AMU decline in this decade, primary production will have to be expanded at existing mines and new mines will have to be developed. The major content of AMU will be government stockpiles, the most significant components of which will be weapons uranium and plutonium, particularly the former. By the end of this decade, an expanding resource base of new uranium deposits will have to be identified as a result of renewed exploration investments.

Industry consolidation has resulted in a reduction in the number of purchasers in the USA, although the buying power of the shrinking number of remaining purchasers has increased. Supply industry consolidation has resulted in increasing corporate concentration, something that has been reason for some concern in the conversion, enrichment, and fabrication market sectors. Though trade regulations in the USA continue to restrict the import of uranium from Russia, there could be some relaxation in the coming years, at least, to the extent that Russia has excess supply capacity and the West badly needs access to it.

While overall world supply may be sufficient to meet demand, there will be increasing consumer competition to obtain it at reasonable cost. There is expected to be increasing upward pressure on market prices in the mid- to longer-term because of this competition and as investments in expanded mine capacity are required, and more intensive exploration and development activities are mounted. While some uncertainty continues to hang over the industry, the outlook is that supply may continue to meet demand through the end of this decade, but capacity will have to be increased as we enter the next decade – all of which assumes that growth in requirements continues at its current slow pace. However, if the industry were to embark on a nuclear resurgence, as some predict, meeting uranium requirements would be a challenge and possibly could be a constraining factor in the mid- to long-term.

THE MARKET

The continuing rise in nuclear plant capacity factors to record levels, and the fact that the majority of the US reactor fleet is opting to undergo power uprating, has resulted in nuclear power forward operating costs reaching an all-time low and being expected to remain low. Nuclear power costs will be further enhanced by the life extension of most US nuclear plants. The high operating level of that nation’s nuclear fleet has resulted in an increase in uranium demand over that previously forecast.

Energy Resources International’s (ERI’s) reference case forecast (see Figure) projects world uranium requirements as rising from their current level of about 174 million pounds U3O8 per year to 192 million pounds by 2016 and then plateauing at that level through 2025. The Figure also compares the ERI forecast with the 2003 World Nuclear Association reference case forecast. It can be seen that the WNA forecast is more optimistic, primarily because it includes an additional 21GWe of nuclear power capacity by the middle of the next decade. While US demand is forecast to remain relatively flat at approximately 56 million pounds per year through 2025, there may be a 60% increase in East Asian requirements and a 8% decline in western European requirements during the same period. Most of the western European decline is projected to take place in this decade as governments continue to bow to anti-nuclear pressures. The Commonwealth of Independent States and Eastern European collective requirements are projected to decline by about 12% by 2025.

The spot market price of uranium, which was at $10.10 per pound U3O8 (Ux U3O8 price) at the end of March 2003, rose to $18.50 by the end of July 2004. The price rise began in the third week of April 2003 following the McArthur River mine flood, increasing to $11.30 by the beginning of August. The price rise received further impetus when Russia’s Techsnabexport (Tenex) announced on 3 November that it would no longer supply natural uranium to its former subsidiary, Globe Nuclear Services & Supply, that in turn claimed it did not have any alternative source of corresponding supply to meet its commitments to US utilities, following which the parties entered into litigation that is still ongoing. The shutdown of ConverDyn’s Metropolis UF6 plant in September 2003, and again in December after a brief restart period, provided further price rise momentum when it was realised that this could result in some Russian HEU-derived UF6 feed being tied up for as much as a year or more. While Metropolis was restarted at the end of April 2004 after an interruption of over six months, the HEU feed supply problem is expected to continue into 2005.

Spot market volume has ranged between 19 and 21 million pounds during the past three years, and was about 11% of world requirements in 2003. Approximately three quarters of the spot market volume in 2003 was in the form of uranium concentrates, and most of the other quarter was UF6. Off-market volume was up and made up more than 40% of the total. Approximately one quarter of the volume involved discretionary purchases. Utilities and suppliers each represented approximately half of the volume transacted. US and non-US utilities sold essentially no material but bought more than 50% of the volume on a two-to-one basis, respectively. The number of sellers’ offers diminished as the year progressed because of the tightening market that was emerging.

Long-term contract volume in 2003 was down from last year’s volume of 67 million pounds to about 45 million pounds. Approximately 60% of the buying volume was US utilities contracted for delivery periods (terms) of between three and four years with about 1.5 year lead times. On average, non-US purchasers decreased their contract terms to about four years with about two years lead time. Almost three quarters of the transactions were off-market, partially a result of utility and supply industry consolidation. The preferred forms were UF6 (45%), U3O8 (40%) and enriched uranium product (EUP) (15%); US buyers preferred UF6 whereas non-US buyers preferred EUP. Producers represented almost half of the selling side of the market in 2003, traders about half the remainder, and enrichers and others the remaining half. While some non-US utility commitments extend through 2012, whereas US commitments end in 2008, some US utilities are now looking to longer-term contracts in order to bridge what is perceived as likely to be the tight market period through 2012. As in the case of the spot market, the number of sellers’ offers diminished as the year progressed.

Spot market volume was down about 20% during the first half of 2004, and off-market transactions continued to increase their market share. Buyers have been increasingly standing back from the market, waiting for prices to stabilise and possibly even decline. Sellers on the other hand are reluctant to sell their product at current prices, believing that buyers will have to come forward soon to cover their needs. While it has always been the buyers’ position that assurance of supply must take priority over market price, this was never a problem in the adequately supplied buyers’ markets of the 1990s and since wherein price was the driving factor. However, now that the market is tightening, assurance of supply is becoming the driving factor.

ALREADY-MINED URANIUM

The West’s nuclear industry currently holds commercial inventories equivalent to about 2.8 years of Western forward requirements. In general, US nuclear power generators only hold fuel cycle process pipeline uranium-equivalent material but very little in the form of strategic inventories. At the beginning of 2004, US utilities held 45.7 million pounds in inventories, an amount equal to about one year of forward demand. While it is believed that Russia may hold about 160 million pounds of uranium-equivalent inventories this is based in large part on information that might be regarded as somewhat speculative. It is thought that Russian inventories may include material that would not meet Western fuel isotopic specifications. There is some concern that because of the tightening market, some utilities may revert back to carrying substantial strategic inventories, for example, as Japanese utilities did in the past. If this should happen then it could tighten the market earlier than expected and put additional upward pressures on prices in this decade.

The 1993 HEU purchase agreement concluded between Russia and the USA resulted in the delivery to the USA of 6377t of low enriched uranium (LEU) derived from 216.5 tonnes HEU, as at 30 June 2004. This equates to approximately 170 million pounds U3O8 equivalent (U3O8e) having already been made available to the world market. Another 228 million pounds is scheduled to be made available between now and 2013, at the rate of 24 million pounds per year. USEC purchases the enrichment component of this LEU and transfers a portion of the uranium feed component to Russia’s uranium marketing agents and returns the remainder to Russia. However, because of the Metropolis conversion plant’s recent lengthy shutdown, and because ConverDyn manages the returns under a trilateral agreement with Tenex and USEC, it will take two or three years for the returns to get back on schedule. Because of Russia’s possible perceived need to maintain nuclear weapons parity with the USA, it is possible that there may be no further sales of HEU.

The blending in Europe of Russian HEU with reprocessed uranium is projected to displace the need for uranium supply by as much as 54 million pounds. While the USA is also blending down HEU to equivalent nuclear fuel materials and services, the quantities are not yet very significant compared to the HEU programme in Russia, but will nonetheless amount to almost 20 million pounds U3O8e during the next 11 years. The US Department of Energy (DoE) also has natural uranium inventories amounting to about 50 million pounds that are expected to enter the market during the next 12 years. However, 14.2 million pounds of this stockpile is contaminated with technetium. It could probably be cleaned at the DoE’s Portsmouth gaseous diffusion plant after 2006 when USEC’s contaminated uranium cleaning is completed. There have been press reports that the DoE might blend down as much as 100tU of HEU in the foreseeable future but the government has not yet provided any concrete plans for doing so.

At the time of USEC’s privatisation in July 1998, the DoE transferred an inventory of about 75 million pounds of uranium in various forms to the new company. Since privatisation, USEC has delivered approximately 48% of that amount to customers. Of the remaining 39 million pounds, approximately 13.4 million pounds is contaminated with technetium and at least 6 million pounds is understood to be required for working inventory. Under a complex June 2002 agreement between USEC and the DoE, USEC has been using the ‘front-end’ of the Portsmouth gaseous diffusion plant to trap (clean up) technetium from the contaminated uranium.

The US and Russian governments entered into ‘umbrella’ agreements that were associated with the HEU uranium feed component 1999 Commercial Agreement between the Federal Agency for Atomic Energy’s (FAAE’s) predecessor, Minatom, and the Western companies. Under one of the umbrella agreements, Russia and the USA each agreed to build up and maintain 58 million pound ‘collateral’ stockpiles of uranium until March 2009, after which they may be disposed.

MINE PRODUCTION

Mines and AMU are expected to meet approximately 65% and 35%, respectively, of world cumulative requirements in this decade, and 75% and 25% in the following 15 years if the Russian HEU agreement is extended beyond 2013. Four countries are expected to provide about 91% of Western mine production in this decade: Canada, Australia, Namibia, and Niger. These four countries along with Russia, Kazakhstan, and Uzbekistan are projected to provide about 93% of world mine production through 2010.

Canada was the world’s largest mine producer of uranium in 2003, producing 27.2 million pounds U3O8. It is expected to maintain this dominant position through 2025 and beyond. If it had not been for the flooding in April at the Cameco operated McArthur River mine, Canadian production would have been about 30 million pounds in 2003, all from the province of Saskatchewan. The majority owners of the province’s uranium projects are Cameco and Cogema Resources (an Areva subsidiary). Canadian production is projected to rise to 46 million pounds per year by 2010. The McArthur River centre produced 15.2 million pounds in 2003 in spite of the flooding incident. It is currently producing at a rate of 18.5 million pounds per year, close to its licensed annual limit of 18.7 million pounds, and is expected to shortly seek a licence expansion to raise its annual production level to 22 million pounds by about 2007. The Cogema operated McClean Lake mines, which produced 6 million pounds in 2003 are to be replaced as a source of ore at the centre by the 6 million pounds per year Midwest Lake mine, which will begin operation in 2006. While it has a licensed limit of 8 million pounds per year it is not known if the output will be taken above 6 million pounds. The Cigar Lake centre, operated by Cameco, is expected to begin production in 2007 and to be ramped up over four years to 18 million pounds per year. Cameco’s Rabbit Lake mine is expected to continue in production at about 6 million pounds per year through 2006 when current reserves will be depleted; the company has identified the prospect for additional reserves that can be developed. Two existing centres, Key Lake and Cluff Lake, came to the end of their resource life last year.

McClean Lake

McClean Lake is operated and majority-owned by Cogema Resources

Australia is currently the world’s second largest uranium producing country with an output of 20 million pounds U3O8 in 2003. It has two large operating production centres, Ranger and Olympic Dam, and a single small solution mining centre, Beverly. While the Ranger mine produced 11.3 million pounds in 2003 and will be depleted by 2008, milling of its stockpiled ore will continue through 2011. If Ranger’s nearby Jabiluka deposit is not developed then operations at the centre will cease at that time. Ranger’s owner, Energy Resources of Australia, majority owned by the UK’s Rio Tinto, has stated that it will acquiesce in the future to the wishes of the native people region who are not in favour of Jabiluka being mined. The large Olympic Dam centre could increase output from its 2003 level of 7.1 million pounds up to its licensed limit of 17 million pounds per year by about 2008. Its owner, Western Mining Corporation (WMC), is considering expanding Olympic Dam’s capacity to about 24 million pounds per year, possibly during the next decade. The Beverly mine, owned by Heathgate Resources (a subsidiary of General Atomics of the USA), produced about 2.6 million pounds in 2003 and is expected to reach its design level of 3.3 million pounds in 2004. WMC, the owner of Yellirrie in Western Australia, has had its mining approvals for that deposit’s development rescinded by the state of Western Australia. It is unlikely that this and many other prospective undeveloped uranium projects will receive permits to go forward in the foreseeable future, since Australia’s ruling political party’s policies do not favour nuclear power.

Total production from the Akouta and Arlit mines in Niger is expected to remain relatively constant during this decade at about its current 8 million pounds per year level. Production at Namibia’s Rio Tinto controlled Rössing centre is scheduled to end in 2007, though this might not occur if the recent market price increase is sustained and there is sufficient utility customer long-term conditional commitment during the coming months. The improved market has already resulted in Rössing production being almost 33% greater than market expectations based on recent historical levels.

While economic difficulties could keep South African production at relatively low levels for the foreseeable future, there are some indications that production could be increased from the current level of about 2 million pounds to at least 4 million pounds per year during the next decade, depending on market conditions. US production has been projected to increase slowly from its current level of 2 million pounds per year to 6 million pounds by 2020. The recent market price increases could result in production rising more quickly though this remains to be seen. For the foreseeable future, China is expected to limit production to meeting the needs of its own gradually increasing national nuclear power programme. While uranium is produced in small quantities in several other countries, total output is only about 2 million pounds and not likely to increase significantly. A possible exception is Brazil, which has significant resources but no extensive current production plans.

Production in Russia is projected to remain relatively constant at about 7.5 million pounds per year throughout this decade and begin expanding in the next decade, as conventional production declines at the Priargunsky centre in Eastern Siberia, and in situ leaching (ISL) production expands. Kazakhstan’s production from several ISL mines is expected to almost double from its 2003 level of about 8.6 million pounds by the middle of the next decade. While Kazakhstan’s government has indicated even greater output levels in the future, it remains to be seen if this can be achieved; substantial ISL reserves have been reported. Two of the country’s new ISL mines are controlled by Cameco and Cogema. Ukrainian production is expected to remain at about 2 million pounds per year through the middle of the decade and then be phased out by the end of the decade because of economics. Uzbekistan is projected to continue production through this decade and the next at between 5 and 6 million pounds per year.

SUPPLY VULNERABILITY

The fuel cycle in the USA and in the rest of the world is vulnerable to potential supply interruptions. Potential supply interruptions could, for example, be the result of: a major industrial accident or terrorist action at a supply facility; significant political differences between the consumer and major supplier countries; or insufficient strategic inventories of either uranium concentrates, natural UF6, or EUP to accommodate potential delays in the transportation infrastructure. The ongoing security of nuclear fuel supply in the USA and other countries such as Japan, South Korea, and Taiwan, to name just one geopolitical region, are highly dependent upon imports of uranium, conversion services and enrichment from other countries.

US requirements for uranium are largely supplied from non-US sources, for example mined uranium from Canada and Australia, and HEU feed from Russia. The European Union is highly dependent on uranium imports from Canada, Australia, Africa, Russia, Kazakhstan, and Uzbekistan. Only one fifth of all US utility enrichment services supply is obtained from domestic production while the remainder is supplied from Russian HEU and imports from the European Union. Most of the US production is exported to East Asia, a region that is averse to Russian sourced supply.

US electric utility companies are dependent upon imports to meet about 80% of their collective U3O8 requirements during the middle of this decade. US uranium production is only expected to meet about 4% of domestic requirements. The DoE holds substantial uranium inventories that have the potential to be a source of supply to backstop the domestic utility industry, subject to pending legislation. However, the DoE has not determined under what circumstances it could make supply available from its various stockpiles, and the utility industry is concerned that under such circumstances, the lead times for emergency supply by the government might turn out to be lengthy. While US electric utility companies collectively hold pipeline uranium inventories equivalent to about nine months of current requirements, the country’s single enricher holds substantial inventories though these are probably only available to its own customers, and will in any case be drawn down in two or three years.

SUPPLY/DEMAND BALANCE

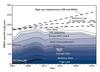

The Figure on page 13 presents the projected world uranium supply and requirements balance through 2025. The balance assumes that there will be HEU I and II uranium feed supply, that Rössing will continue to operate until the middle of the next decade, that there will be substantial AMU supply, and recycle savings. It does not assume that Jabiluka will be developed before 2025. In this scenario, it is assumed that Russian tails upgrading will take advantage of Russian surplus enrichment capacity through 2025.

The production shown is projected to come from the currently identifiable mine production around the world. Identified mine production is projected to rise from about 105 million pounds in 2004 to a plateau of about 130 million pounds extending from 2015 to 2025. The AMU is projected to provide supply that declines gradually from about 71 million pounds in 2004 to approximately 44 million pounds by 2020.

If there is no HEU II there will be a shortfall of at least 30 million pounds by 2015 and 50 million pounds during the 2015-2025 time period. It can be assumed that most of this shortfall would have to be made up from primary production. If the US government were to make 100tU available it could supply 8 million pounds of uranium annually for ten years.

It can be seen that supply could meet ERI-projected reference requirements through about 2011 and WNA-projected reference requirements through about 2010. The difference between the two forecasts rises to about 20 million pounds per year during the 2015-2025 period. It can be seen that expanded mine capacity will be required after 2010 to meet either requirements projection. It is projected that supply could not meet the high case requirements after 2010 unless substantial supply sources became available. At this time the only identifiable source of such large supply is government inventories.

Author Info:

Julian Steyn, Energy Resources International Inc., 1015 18th Street, NW, Suite 650, Washington, DC 20036, USA