Fuel review: supply

Waiting for a rebound

28 September 2012The uranium market has settled into a holding pattern over the past year, with the supply side of the market anticipating a price rebound by 2014. Supply is sufficient that output from planned mines is not needed until around 2018 or until 2023 from prospective mines. By Thomas Meade, Julian Steyn and Eileen Supko

In contrast to the significant volatility demonstrated by the spot market price of uranium over much of the past five years, the long-term price for uranium concentrates has held steady over the past nine months. The Fukushima accident in March 2011 dampened what had been a growing enthusiasm in the uranium concentrates market. While the spot price rebounded slightly and levelled off in the low-fifties by mid June 2011, uncertainty over when Japanese demand will be restored as well as the fear that sizable Japanese inventories might be released to the market have conspired to keep the spot market price in its recent narrow range.

The long-term price followed a similar trajectory to that of the spot market price, but moved much more slowly. While the long-term price managed to hold steady for a few months after the Fukushima accident, the realities of the post-Fukushima market set in and the price then steadily declined to about $60 per pound by early 2012. As of 30 June 2012 the long-term price was $61, according to monthly indicators published by TradeTech LLC.

Suppliers’ professed faith in the longer-term prospects for nuclear power and their belief in a tightening of supply relative to requirements following the end of the US–Russia HEU Agreement in 2013 have prevented a steeper decline. The uranium market has settled into a holding pattern over the past year, with the supply side of the market anticipating a price rebound by 2014. The following examination of the adequacy of supply relative to nuclear power plant requirements may shed further light on future prospects for the uranium market.

Mine production

The primary source of uranium supply for nuclear power plants is uranium from mine production centres around the world, mainly concentrated in 12 countries. Total mine production for 2011 is estimated to have been 139 million pounds, approximately the same as in 2010. Overall, mine production has increased by over 35% since 2006. Primary mine supply as a percentage of nuclear power plant requirements has increased from 65% in 2006 to 87% in 2011. This is primarily due to the increased output of Kazakhstan. Also, 2011 nuclear power plant requirements were down due to Fukushima.

Kazakhstan, Canada, Australia, Niger, Namibia, Russia, Uzbekistan, the United States, China, Ukraine, Malawi and South Africa have been the source of 98% of all uranium mined over the past five years (see Figure 1). The top three countries alone—Kazakhstan, Canada and Australia—accounted for 65% of all uranium mined in 2011.

Uranium mine production can be categorized into four general mining methods: (i) in situ leach (ISL), which is also referred to as in situ recovery (ISR), (ii) underground, (iii) open pit, and (iv) by-product.

ISL mining has grown rapidly over the past five years, primarily due to its use in Kazakhstan, and now accounts for 45% of world mine production (vs. 24% in 2006). Underground and open pit mining methods, sometimes referred to as conventional mining, now account for 30% and 18% of world mine production, respectively. The share of both methods has decreased from 2006 when they accounted for 43% and 24% of mine production. The by-product method refers to production centres using conventional mining methods where another metal is the primary mine product (for example copper at Olympic Dam) and currently accounts for 7% of uranium production.

The uranium industry is fairly concentrated with less than ten suppliers controlling 90% of world uranium production in 2011. The mine production controlled by each supplier reflects arrangements where the mine operator may have the right to market more than its equity share of production from a mining centre that has multiple owners. The top three producers of uranium are Kazatomprom, Cameco and AREVA, with a combined 49% of 2011 mine production. Historically, Rio Tinto’s production has rivalled that of the top three, but it has been down in 2010 and 2011 due to production problems at its flagship Rossing (Namibia) and Ranger (Australia) mines.

Kazakhstan has been the number one uranium producing country since 2009. The explosive rate at which Kazakhstan’s production has expanded is remarkable. Production has increased ten-fold over the past ten years from 5 million pounds in 2001. While the 2011 production represents a healthy 9% increase over 2010, the Kazakh government decided in 2011 that it needed to limit the market pricing impacts of too rapid an expansion, further accentuated by the Fukushima effect, on demand. Further expansion potential exists, with nameplate capability potentially as high as 70 million pounds by 2017. However, current government policy is to stabilize production at around 52 million pounds, with further expansion to 65 million pounds or more when market prices improve from current levels. A major contributing factor in Kazakhstan’s rapid ascent to the rank of world’s largest uranium producing country was the decision to actively court external investment in the form of joint ventures.

The total output of Canada’s operating centres in 2011 was 23.8 million pounds U3O8. Canadian production is projected to rise to 29 million pounds by 2025, assuming that the flooding-delayed Cigar Lake mine is on line by 2013. Due to the unique geological conditions of many of the deposits in the Athabasca Basin, the deposits at McArthur River, Cigar Lake and Rabbit Lake have encountered technical challenges related to the inflow of water into the mines. The Cigar Lake mine suffered severe flooding problems that delayed its start by approximately seven years to 2013.

Increased production in Canada is hardly limited to the development of Cigar Lake, however. The 2008 discovery by Denison of the world-class Phoenix Deposit at Wheeler Lake is one of the most significant findings in recent time. Denison continues exploration of the deposit with a large drilling programme (the project is considered ‘prospective’ in Figure 3).

Cameco’s Millennium deposit is moving into mine development following an environmental assessment. Resources at the Dawn Lake (Cameco), Kiggavik-Sissons (AREVA), and Michelin (Paladin) projects are being delineated on schedules that could see first production after 2015. In late 2011, Rio Tinto outbid Cameco for the purchase of Hathor Exploration and its 52 million pound Roughrider deposit, where first production could occur by 2021.

Australian production in 2011 was 16 million pounds. Annual production capability is projected to climb slowly to 35 million pounds by 2020 and 50 million pounds by 2026 if the Olympic Dam mine output increases as proposed. The expansion has been approved by state and federal regulatory authorities, but still requires BHP Billiton board of director approval. While board approval was originally expected in 2012, BHP in mid-2012 indicated it might curtail its $80 billion capital expansion plans across all mining sectors due to market concerns and is now expected to defer a final investment decision for two years. South Australia’s prime minister is adamant that the mid-December deadline for a commitment that was imposed by the government will not be extended. With operations at Ranger’s Pit 3 approaching the end of mining, Energy Resources Australia (ERA) has embarked on a development programme to provide for future production at Ranger; a key component of which is development of the Ranger 3 Deeps exploration decline. Ranger 3 Deeps is located on the Ranger Project Area, adjacent to Pit 3, and contains an estimated resource of approximately 75 million pounds.

Niger is the world’s fourth largest uranium producer. In 2011, 11.3 million pounds of uranium was produced in three centres: Arlit, Akouta, and Azelik. The output of the Arlit and Akouta centres in 2011 was approximately 7.1 and 3.7 million pounds, respectively. The new Azelik mine, operated by a China/Niger joint venture, began uranium production in December 2010. There is also a large mine under development that AREVA has committed to bring into operation by about 2014, Imouraren. It is the operating-owner participant in the Arlit and Akouta centres as well.

All uranium mining in Russia is controlled by the Atomredmetzoloto Holding Company (ARMZ), which completed consolidation of shares of Russian uranium mining enterprises in 2008. Russian production declined to 7.4 million pounds in 2011 from 9.3 million pounds in 2010. The fall is due to lower output from the large Priargunsky mine centre in Siberia where production declined to 5.7 million pounds in 2011 from 7.6 million pounds in 2010. The drop in production is reportedly due to lower grades, but that information is preliminary. While earlier indications were that the Priargunsky mine would be gradually phased out of production, current plans are for it to continue to operate indefinitely in order to meet Russian requirements. The output from existing centres is projected to increase to about 12 million pounds per year during the remainder of this decade and thereafter. It is also expected that the country’s two ISL mines (Dalur and Khiagda) will be expanded gradually to produce a total of about 4.6 million pounds per year by 2014. The introduction of production from the large Elkon field in the coming decades could increase future Russian output dramatically, limited only by demand and available capital.

There are two large conventional mines operating in Namibia, which produced 8.5 million pounds of uranium in 2011. The first of these is Rio Tinto’s very large, low-grade open pit Rossing mine that has been operating since 1976. The second mine, Paladin Resource Limited’s Langer Heinrich, was brought into production at the beginning of 2007. AREVA’s proposed Trekkopje mine is now considered to be prospective by ERI due to project economics, despite the considerable investment made by AREVA to date. A number of additional mines are under consideration in Namibia. The world-class Husab project has been acquired by China Guangdong Nuclear Power Group (CGNPC) and could be developed for production by about the middle of this decade, with potential production of 15 million pounds per year.

Uzbekistan’s production in 2011 totaled 6.4 million pounds. It is projected that annual production in Uzbekistan may rise to almost 8.0 million pounds by 2016 and remain at about that level thereafter. Production of uranium in Uzbekistan is controlled and managed by the Navoi Mining & Smelting Combine and is obtained from three ISL mines and a central mill.

There are approximately nine existing ISL production centres in the United States—usually referred to as ISR production centres. Some of them have been in operation for a number of years: Cameco Corporation’s Crow Butte and Highland/Smith Ranch centres; and Mestena’s Alta Mesa project. New ISR projects with first production in 2011 include Uranium Energy Corporation’s Palanga (see picture, p21) and Uranium One’s Willow Creek. The Lost Creek and Nichols Ranch ISR projects are about to start up. In addition, Energy Fuels is currently acquiring Denison’s US uranium assets. These include the White Mesa mill, which processes alternate uranium waste feed (not necessarily mine-produced) from other uranium processing facilities, vanadium from some Colorado Plateau ores, and provides ore toll milling for a number of small mines in the region. US production could climb from its 2011 level of about 4.0 million pounds to at least twice that level by 2015.

China’s production in 2011 is estimated to have been approximately 2.3 million pounds. Heap leaching is widely used in China’s uranium mines. While uranium production is expected to increase in China, it is likely to lag far behind the country’s rapidly increasing requirements.

Ukraine’s production, which in 2011 totaled approximately 2.3 million pounds, is projected to increase to about 3.9 million pounds by 2015, and remain at that level thereafter. Production of uranium by Zholty Vody in Ukraine is controlled and managed by the government organization Vostochny Mining & Processing Combine (VostGOK).

The economy of Malawi, a country in southeast Africa bounded by Mozambique, Zambia and Tanzania, has been substantially enhanced by the development of the Kayelekera uranium mine. The Kayelekera sandstone open pit uranium mine project was brought into production by Paladin Resources Limited in late April 2009 and ramped up to production of 2.2 million pounds in 2011. It is expected to reach full production of 3.3 million pounds in 2013.

There is currently one fully commercial project producing uranium in South Africa at AngloGold’s Vaal River where by-product uranium is produced from gold mining operations, resulting in the production of 1.3 million pounds in 2011. First Uranium is in the process of selling two other properties where uranium is a by-product of the primary gold operation. Ezulwini is an underground gold and uranium mine being sold to Gold One, while Mine Waste Solutions is a tailings recovery project being sold to AngloGold. Mine Waste Solutions production, which has so far not yet begun, would be integrated into the Vaal River project in the future. Uranium production at the Ezulwini facility amounted to 0.1 million pounds in 2011; production was halted following several fatal accidents.

In addition, potential production may eventually take place at more than 40 resource projects that have not yet been developed. Prospective mines could potentially provide 150 to 170 million pounds of nameplate capability during the 2020s. The actual development schedule will be determined by many factors, the most important of which is market need. Mine economics and local politics are key factors, as well. In general, ERI expects that only about half of the prospective mines that it has identified will ultimately be developed and brought into production in the foreseeable future and that the actual development schedules will be significantly delayed from the most optimistic schedules put forth by owners.

Secondary supply

Commercial uranium and uranium equivalent inventories held worldwide as of the end of 2011 are estimated to be between 392 million pounds and 502 million pounds U3O8. However, very little of this inventory is expected to become available to the market to support operation of nuclear power plants. Of course, one must acknowledge that following the Fukushima Daiichi accident and the shut down of a significant number of units in Germany and Japan, there is the possibility that some inventory being held by owners of the shutdown plants will eventually be released to the commercial markets. Nonetheless, to date little has appeared. Most adjustments to reduced power plant requirements have been made between the specific power plant operators and their contracted suppliers. This is a situation that will warrant ongoing attention.

Secondary supply also includes U.S. Department of Energy (DOE) excess inventories, Russian high enriched uranium (HEU), Russian tails uranium recovery, enrichment plant underfeeding, and recycle of plutonium and uranium. Secondary sources are projected to supply about 61 million pounds annually between 2011 and 2013, then decline to an average of 38 million pounds per year thereafter. For the next two years, the largest source of secondary supply remains Russian HEU.

In May 2012, DOE released a Secretarial Determination covering all of its planned commercial sales and transfers over the next ten years. The ongoing sale of HEU-derived low enriched uranium (LEU) to the Tennessee Valley Authority (TVA) under the Blended Low Enriched Uranium (BLEU) programme is included. It appears that the transfer of natural uranium hexafluoride (UF6) to pay decontamination and decommissioning contractors is to be continued, potentially at a rate as high as 2400 MTU (metric tons uranium) per year. The UF6 will be released to the market in a mix of spot and term contracts. In addition, approximately 9000 MT of depleted uranium (DU) is to be re-enriched by USEC and delivered to Energy Northwest and TVA under a long-term arrangement. The total natural uranium content of the DU is approximately 10 million pounds. The May 2012 Secretarial Determination covers the release of all remaining DOE inventories of UF6, but some unallocated HEU and DU will still remain after ten years. However, it is assumed that those inventories will be released at an annual rate of 5 million pounds after 2020.

The re-enrichment of Russian tails from an assay of 0.30 weight percent (w/o) to natural (0.711 w/o) or LEU levels (4.0 w/o) will result in residual assays in the range of 0.11 to 0.15 w/o will result in the supply of significant quantities of natural uranium equivalent. Equivalent uranium produced from Russian DU is projected to average 14 million pounds annually over the next ten years, but then decline as the stockpile of DU is exhausted. Underfeeding is also expected at enrichment plants operated by Urenco and AREVA, and is projected to result in the supply of approximately 5 million pounds per year for the long-term.

The total uranium-equivalent world supply from uranium and plutonium recycle for the ERI reference nuclear power growth forecast increases from 7 million pounds U3O8e in 2012 to 10 million pounds annually through 2035.

Forecast requirements

Under the ERI reference forecast (see Figure 2), total world requirements are projected to rise from 160 million pounds in 2011 to 240 million pounds in 2030, and average 250 million pounds per year during the subsequent five years. This represents an increase of approximately 50% in world annual requirements for uranium through 2035. Cumulative world requirements under the ERI reference forecast between 2012 and 2035 are forecast to be around 5.2 billion pounds.

The low forecast indicates that world requirements could potentially decline to 90% of the 2011 level by 2035 (144 million pounds U3O8). Alternatively, world high forecast requirements are projected to increase 116% by 2035 to around 185 million pounds.

Projections of uranium concentrate requirements by region in 2030 are shown in Figure 2.

Market outlook

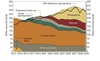

Figure 3 presents the projected world uranium supply and requirements relationship for ERI’s reference nuclear power growth forecast. This forecast represents ERI’s best estimate of the future relationship between uranium supply and requirements. The primary uranium supply shown in Figure 3 is split into five components: current mines, expansion/ramp up, under development, planned, and prospective.

Production from the first three components may be viewed as relatively secure with little uncertainty as to schedule and output. A 90% capacity factor is applied to the nameplate annual production capacity for current mines because of supply interruptions from unforeseen events such as accidents, floods and fires, for example. Production from the last two components—planned and prospective mines—is much less certain and will be highly dependent on actual market need, that is, actual requirements.

For the ERI reference requirements, the new supply does not need to come on line as quickly as presently published plans and/or potential schedules indicate. In fact, an average delay of three years is assumed for mines under development, six years for planned mines, and nine years for prospective mines. ERI assumes that schedules for mines currently in the midst of ramping up to full production are delayed two years.

In addition to these postulated delays, only about 50% of the prospective mines are assumed to proceed at all, to accompany about 75% of planned mines, and 90% of mines under development. Note that the annual production for each of these new mines is also subject to the average 90% production factor used for existing mines.

The figure indicates that first output from planned mines is not needed until around 2018 and is not significant until the 2020s. For example, the output from planned mines reaches 20 million pounds in the year 2024 and 30 million pounds in the year 2027. First output from prospective mines is even further delayed, and is not needed until around the year 2023, but is significant by the year 2025 when production from prospective mines should be 30 million pounds.

The actual future production from mines categorized as planned or prospective is also subject to factors in addition to the market need already mentioned. In particular, individual mine economics, local politics and governmental policies will play key roles in determining which resources are ultimately brought into production. The above discussion indicates that there will be sufficient time to meet the challenges associated with bringing new mine capability into production on a schedule that will maintain uranium supply adequacy. Of course, it is not possible to state with absolute confidence which of the individual planned and prospective new mines will ultimately be brought into production and which will not.

Figure 3 shows that the supply for the reference scenario exceeds requirements. This reflects the fact that actual demand for uranium will be greater than nuclear power plant requirements, as end-users are expected to increase the amount of uranium held in strategic inventory as new units are brought on line and uranium requirements increase. China in particular built significant uranium inventories in 2010 and 2011 and appears to be continuing to build inventory in 2012. Over the long term, the supply assumed for the reference scenario is 5% greater than nuclear power plant requirements, and is equivalent to building strategic inventories of approximately two-and-a-half year’s forward supply for new nuclear power plants.

Author Info:

Thomas Meade, Julian Steyn and Eileen Supko, Energy Resources Intl., Inc., 1015 18th Street N.W., Suite 650, Washington, DC 20036, USA. This article was published in the September 2012 issue of NEI magazine.

Related ArticlesToward market balance Transition almost completeFilesFigure 1: Uranium production by country 2006-2011 Figure 3: Uranium supply adequacy in the reference requirements scenario to 2030