Fuel review: supply

Up, up and up

28 September 2012The 2011 edition of the Red Book ups its estimate of total uranium resources, but warns that the price of production is increasing. Production is up compared with 2009 and demand for uranium is also expected to continue rising.

Spending on uranium exploration and mine development rose by 22% between 2008 and 2010, contributing to a 12.5% increase in identified uranium resources, according to Uranium 2011: Resources, Production and Demand, published in July 2012.

The publication, commonly referred to as the Red Book, is the latest in a series of joint reports released by the OECD Nuclear Energy Agency (NEA) and the International Atomic Energy Agency (IAEA). The latest edition provides a statistical profile of the world uranium industry as of 1 January 2011 (or 1 September 2011 for demand forecasts, which were delayed to reflect policy changes post Fukushima). It is based on official information provided by 34 countries, along with NEA/IAEA estimates for a further eight, including most significantly South Africa and Namibia.

Although the focus of the report remains uranium resources, production and demand, updates on the environmental and social effects of the uranium production cycle are included in the national reports in this edition.

Some country reports, including those from Brazil, the Czech Republic, Hungary, Poland, Portugal, the Slovak Republic and Spain include updates on remediation and closure activities that are being carried out at uranium production facilities that operated in the past without strict environmental regulations.

Resources: up

Uranium 2011 estimates that there are close to 7.1 million tonnes of conventional uranium resources recoverable at costs below $260/kgU; an increase of 790,300 tU (12.5%) on the figure reported in 2009. At 2010 rates of consumption (63,875 tU), identified resources are sufficient for over 100 years of supply for the global nuclear power fleet, the report states.

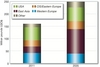

Although total identified resources have increased overall, since 2009 there has been a significant reduction in lower cost resources i.e. those recoverable under $80/kgU (see graph).

Reduced resources in these categories were due to “increased mining costs,” the report said. However it noted that resources in the <$40/kgU cost category are likely higher than reported because detailed estimates are either not available or are confidential for many countries.

In all cost categories, underground mining is the predominant production method. In the lower cost category it accounted for 314,000 tU of reasonably assured resources, mainly from Canada, and 120,000 tU of inferred resources. Resources in the by/co-product category also make a significant contribution to the <$40 /kgU cost category (133,500 tU total), with ISL from China and Kazakhstan making up most of the rest.

In terms of countries, Australia remains by far the country with the leading amount of identified uranium resources recoverable at <$260 /kgU: a total of 1738 million tU in 2011. It is followed by Kazakhstan with identified resources of 820 million tU, Russia with 650 million tU and Canada with 614 million tU, according to the data in Uranium 2011.

The Red Book concluded that the increased resource base, described above, has been achieved thanks to a 22% increase in uranium exploration and mine development expenditures between 2008 and 2010. In 2010, spending reached an all-time high of $2.07 billion.

“The declining uranium price slowed down many exploration and mine development projects in the short term, particularly in the junior uranium mining sector,” the report said.

But it added that: “Most producing countries reported increasing expenditures, particularly in Africa, where significant mine development activities are underway.”

In Canada, overall uranium exploration and development expenditures amounted to $585 million in 2010, compared with $458 million in Niger and $383 million in Russia.

Production: up

Global uranium mine production increased by over 25% between 2008 and 2010 principally because of significantly increased production in Kazakhstan (109%), currently the world’s leading producer.

Output of 54,670 tU was reported from a total of 22 countries in 2010, two more than in 2008 as production began in Malawi in 2009 and Germany resumed uranium recovery through mine remediation efforts, the report said. Eleven new mines opened in 2009-2010; five of which were located in Kazakhstan.

Demand: up

Demand for uranium is expected to continue to rise for the foreseeable future, according to the report.

“Although the Fukushima Daiichi nuclear accident has affected nuclear power projects and policies in some countries, nuclear power remains a key part of the global energy mix,” it said.

By 2035, the joint NEA-IAEA Secretariat projects that world nuclear electricity generating capacity will grow from 375 GWe net (at the end of 2010) to between 540 and 746 GWe net in the low and high cases, respectively. Accordingly, world annual reactor-related uranium requirements are projected to rise from 63,875 tU in 2010 to between 98,000 tU and 136,000 tU by 2035.

Existing, committed, planned and prospective resources could satisfy projected high case requirements through 2030 and low case requirements through 2035, the report notes. “Nonetheless, significant investment and technical expertise will be required to bring these resources to the market and to identify additional resources.”

Uranium 2011 goes slightly further than editions published in the prior several years (in 2006, 2008 and 2010) by saying that “Strengthened market conditions will be required for resources to be developed to meet projected uranium demand within the time frame required.” Earlier publications (2006, 2008 and 2010) simply called for “a strong market” and in some cases “sustained high prices” to support the timely development of resources.

Author Info:

Uranium 2011: Resources, Production and Demand (ISBN 978-92-64-17803-8) can be ordered from the OECD direct, priced €140. This article was published in the September 2012 issue of NEI magazine.