Fuel review: enrichment

Transition almost complete

1 October 2012The transition from gaseous diffusion to centrifuge enrichment technology is nearly complete. Although there is some uncertainty about new centrifuge plant projects, present market prices are sufficient to stimulate their construction. By Thomas Meade and Michael Schwartz

The enrichment services market has witnessed much activity over the past five years, but now appears to entering a somewhat calmer phase. The transfer from gaseous diffusion to centrifuge enrichment technology is nearly complete. During this same period, Rosatom and Urenco have become the two dominant suppliers, while former market-leader USEC is transitioning into a lesser role. The industry appears to be well-equipped to add the new capacity that will be needed to meet the expected growth in enrichment requirements over the next 20 years. New centrifuge supply continues to emerge even as uncertainty grows for some of the proposed projects.

The long-term price indicator was essentially flat from April 2010 through August 2011 at between $158 and $160 per separative work unit (SWU), according to monthly data published by TradeTech LLC. While the long-term price was able to hold firm during the six months initially following the March 2011 accident at Fukushima, the impact of reduced Japanese demand combined with a weakening Euro has caused the price to steadily decline over the last nine months. The current long-term price of $140 per SWU as of 30 June 2012 represents an $18 per SWU or 11% price decline since August 2011. Following a sharp drop in July, the published spot price indicator now demonstrates a $15 per SWU or 11% discount relative to the long-term contract price indicator. The spot price discount is now about twice as large as observed over the prior several years. The discount is driven by the current modest surplus of supplier capacity in conjunction with very low near-term demand, as end-users are highly committed under their long-term contracts.

Requirements

Nuclear power plant requirements declined 13% to 39.2 million SWU in 2011, but are expected to rebound to 41.5 million SWU in 2012 and 51 million SWU by 2015. The decline in 2011 was driven by the inability of Japanese nuclear power plants to return from outages following the Fukushima Daiichi accident, as well the retirement of eight plants in Germany. Requirements for enrichment services under the ERI reference nuclear power growth forecast are projected to climb to 59 million SWU in 2020 and to 72 million SWU in 2030, before levelling off at an average of 74 million SWU per year between 2031 and 2035. The average annual growth rate is 2.2% per year. Led by China, growth is strong in East Asia, but also takes place in the Commonwealth of Independent States (CIS)/Eastern Europe, the United States, and other regions.

World requirements under the ERI high nuclear power growth forecast climb to 70 million SWU per year in 2020 and to 101 million SWU by 2030; and average 106 million SWU per year between 2031 and 2025. The overall average growth rate is 4.1% per year. Under the ERI low forecast, world enrichment services requirements are projected to demonstrate slight growth to 51 SWU per year in 2020, but remain relatively flat for the following ten years, averaging 50 million SWU per year between 2021 and 2030. After that a further decline is forecast and low requirements drop to 44 million SWU by 2035.

Current suppliers

Base enrichment services supply includes active primary suppliers such as AREVA, Rosatom, Urenco and USEC Inc. Regional suppliers include China Nuclear Energy Industry Corporation (CNEIC), Japan Nuclear Fuel Limited (JNFL) and others. It also includes some secondary sources of supply. Secondary supply for enrichment services has been dominated by US and Russian supplies of high-enriched uranium (HEU). The individual elements of base supply as characterized by ERI are summarized below.

There typically is a small amount of commercial inventory (less than 2% of world requirements) made available to the market on an ongoing basis, but this is expected to result from mismatches between contracted supply and actual requirements, and not from the release of strategic inventories. ERI expects inventory use to average 1.8 million SWU per year through 2018, but after that no long-term contribution to world supply can be assumed. Sources over the next six years include enrichment services that result from gaseous diffusion plant (GDP) preproduction prior to their shutdown, some inventory being used this year by EDF, and material originally intended for shut-down reactors in Germany.

The AREVA enrichment capability from the Georges Besse I (GB I) GDP, which is located near Pierrelatte, France, was shut down permanently on 7 June 2012. AREVA is presently building a new centrifuge enrichment plant near Pierrelatte that will result in 7.5 million SWU per year of enrichment capacity, utilizing proven Enrichment Technology Company (ETC) centrifuge technology. The new plant, Georges Besse II (GB II), became operational in April 2011 and ended last year with a capacity of 1 million SWU. GB II enrichment capacity had been increased to 1.5 million SWU as of June 2012, and is continuing to ramp up to its nameplate capacity by 2016.

Urenco Europe includes capability from ETC centrifuges that are presently in operation or expected to be installed at Urenco’s three European enrichment plants, which are located in Gronau (Germany), Almelo (Netherlands) and Capenhurst (United Kingdom). These plants had a combined annual production capability of 14.2 million SWU at the end of 2011. While an additional 0.5 million SWU is to be added to European capacity during 2012, the company’s future expansion is expected to take place in the USA.

The Urenco USA enrichment facility in Lea County, New Mexico, which is owned and operated by Urenco, began operating in 2010. At the end of 2011 it had an annual enrichment capacity of 0.4 million SWU. Urenco continues to add enrichment cascades, with 1 million SWU added during the first half of 2012, as it ramps up to its present licensed capacity of 3.0 million SWU per year. Urenco previously has indicated that it expects to request to increase licensed annual production to 5.7 million SWU.

USEC operates the Paducah gaseous diffusion enrichment plant (PGDP), which is located in Paducah, Kentucky. Following negotiation of a multiparty arrangement that included USEC, the U.S. Department of Energy (DOE), Energy Northwest (ENW) and the Tennessee Valley Authority (TVA), the PGDP is now expected to operate through the middle of 2013 as it enriches DOE high assay tails that will be transferred to ENW under the agreement. The LEU created from the DOE tails will be held by ENW and TVA for use in their respective nuclear power plants between 2015 and 2021.

Rosatom is the state-owned corporation overseeing both commercial and military nuclear activities in Russia. Rosatom’s utilization of its substantial enrichment capacity and the way in which it acts in the world market is much more complex than is the case for any of the other enrichers, warranting a more detailed discussion.

The Rosatom uranium enrichment plant production capability refers to the production at four plants in Russia operating at close to a 100% capacity factor: Ural Electrochemical Combine, Siberian Chemical Combine, Production Association Electrochemical Plant and Angarsk Electrolyzing Chemical Combine. Production is reduced approximately 7% from nameplate capacity due to the low operating tails assay (0.11 to 0.15 weight percent, or w/o) employed, which results in some inefficiencies. Production during 2011 is estimated to have been 26 million SWU. For 2011, nearly 6 million SWU was devoted to CIS and Eastern European requirements, which will be referred to as ‘Rosatom Internal’. Current US and European trade policies effectively limited the quantity of Russian enrichment services that were sold directly and indirectly to Western customers during 2011—referred to as ‘Rosatom Export’—to approximately 5.4 million SWU. Rosatom Exports are expected to increase substantially in 2014 to more than 10 million SWU per year and continue to grow thereafter. The direct sale of almost 3 million SWU per year to the US market begins in 2014, consistent with the terms of the 2008 Amendment to the Agreement Suspending the Antidumping Investigation on Uranium from the Russian Federation. In addition to direct sales to owners and/or operators of nuclear power plants, Rosatom exports include wholesale arrangements with other suppliers. Since Russian enrichment capacity is constrained by US and European trade policies, a substantial amount of this capacity will be used (i) to underfeed the Russian enrichment plants in meeting commercial enrichment contract obligations and (ii) to re-enrich depleted uranium tails, creating natural uranium equivalent material (that is, ‘normal’ uranium) for internal use. An operating tails assay of 0.13 w/o uranium-235 tails has been assumed in this regard. Rosatom is further assumed to maintain its long-term shares of approximately 100% and 25% for internal and export markets, respectively. As older centrifuges reach their design lifetimes, Rosatom has been replacing them with newer designs that have higher outputs. As a result, total Russian enrichment production is expected to increase to 32 million SWU by 2025. Not all of this enrichment capacity may be needed, particularly if Russia’s aggressive plans for nuclear power plant expansion are moderated, as is assumed for the ERI reference nuclear power growth forecast.

The Russian HEU-derived LEU is expected to remain at 5.5 million SWU per year through 2012, dropping to 5.3 million SWU in 2013 when the term of the current US-Russian agreement for 500 MT HEU concludes. These SWU quantities are based on the contractually agreed-upon tails assay of 0.30 w/o uranium-235, but the quantities are higher when evaluated on the same transaction tails basis that is used to determine end-user requirements (currently around 0.25 w/o). All parties expect that this arrangement will end in 2013 as scheduled. In order to create and utilize the LEU that is derived from the Russian HEU, approximately 5.4 million SWU contained in blend stock is required. When the blending of Russian HEU ends, this capacity will become available to Rosatom for use in commercial sales, subject to any trade constraints that may still exist. Note that an additional small quantity of SWU is derived from Russian HEU directly blended with European reprocessed uranium (RepU). This programme has gradually expanded and now provides an estimated 0.6 million SWU per year, but will decline in the future, as supplies of the non-weapons-grade HEU are limited.

At present, US HEU includes material that is being used by TVA in the DOE-TVA Blended Low-Enriched Uranium (BLEU) programme that began in 2005 as well as LEU derived from other HEU down blending operations, a portion of which is used to compensate the blending contractors. The contribution to supply is expected to gradually decline from 1.0 million SWU in 2012 to 0.2 million SWU per year in 2020 and beyond.

China has approximately 1.8 million SWU per year of centrifuge enrichment capability. The majority of this capability is used internally, although China exports modest amounts to the USA and Europe from time to time when it has excess. The Chinese enrichment capability primarily uses centrifuges that are imported from Russia, although a small demonstration facility using indigenous centrifuge technology is believed to be in operation. The Chinese centrifuge enrichment capacity is expected to expand to 7 million SWU per year by 2020, as China endeavours to continue to service a substantial portion of its own requirements. China is expected to make use of a combination of indigenous and Russian centrifuge technology for the expansion, but details remain closely held by the Chinese government.

Other capability is primarily in Japan, where Japan Nuclear Fuel Limited (JNFL) has just put into operation the first half-cascade of its next-generation centrifuge. JNFL capacity will slowly rise to 1.5 million SWU per year just after 2020. Brazil is beginning operation of a small uranium enrichment facility, which is scheduled to gradually ramp up to 0.2 million SWU by 2015 and will be devoted to internal requirements. Despite opposing international efforts, Iran continues to install centrifuges and could have 0.1 million SWU per year of enrichment capacity in operation.

Recycle materials contributed about 1.4 million SWU-equivalent to supply in 2011 and are expected to continue to supply the equivalent of as much as 2.1 million SWU per year for the long term.

Future supplies

In addition to the base supply described above, which is less than ERI reference requirements over the long term (see Figure 1), there are three proposed sources of enrichment services whose sponsors have each made a substantial financial commitment to establishing US-based capability to provide enrichment services on a commercial basis. Two out of the three facilities already have received NRC construction and operating licences, and a third may receive its construction and operating license later this year. Our ‘proposed supply’ category includes these three sources.

AREVA has received a licence from the NRC that will allow it to build and operate a centrifuge enrichment plant—the Eagle Rock Enrichment Facility (EREF), in Idaho—using the same technology being deployed in GB II. Initial production had originally been expected to occur in 2014 with ultimate capacity ranging between 3.3 and 6.6 million SWU based on market conditions. However, in December 2011, AREVA announced that it was cutting jobs and suspending projects around the world, including the EREF in the US, as part of a five-year strategic action plan that would allow it to recover from massive losses in 2011 and return to profit. In February 2012, URS Nuclear LLC, the procurement and construction manager for EREF notified all of its subcontractors that the “project has been placed on indefinite suspension until further notice”. In July 2012, AREVA reconfirmed that absent a partner, it will not start EREF construction before 2014.

Global Laser Enrichment (GLE), a business venture of General Electric-Hitachi Nuclear Energy (GEH) and Cameco Corporation, could decide to build a commercial enrichment plant based on laser enrichment technology that is now being licensed. The planned maximum target annual production capacity for the GLE plant is 6 million SWU. Formal licensing proceedings were completed in July 2012 and the NRC is expected to award the license in August or September 2012. While GLE has not yet updated its schedule, if the decision is made to proceed with construction of a commercial plant next year, then the earliest that it might be expected to begin operation is 2015 or 2016. GLE expects that by the end of the first year of operation it would reach an enrichment capacity of 1 million SWU and that its annual production would increase by one million SWU per year thereafter. The planned maximum target of 6 million SWU could therefore be reached as early as 2022.

USEC plans to replace the PGDP with a new 3.8 million-SWU-per-year centrifuge enrichment plant known as the American Centrifuge Plant (ACP). Even though USEC received a licence from the NRC in 2007 to build and operate the ACP, USEC continues to experience delays in obtaining financing and has acknowledged that it cannot continue to independently fund the project. DOE raised additional concerns about a number of aspects of the project that USEC was not able to overcome to DOE’s satisfaction. As a result, instead of issuing the conditional loan guarantee that USEC had sought from DOE, DOE proposed a two-year cost-share research, development and demonstration (RD&D) programme for the project “to enhance the technical and financial readiness of the centrifuge technology for commercialization.” On 13 June 2012, USEC and DOE executed an agreement to move forward on a cooperative RD&D programme with a total investment of up to $350 million. The agreement calls for DOE to provide 80% ($280 million) and USEC to provide 20% ($70 million) of the total. This RD&D programme will support building, installing, operating and testing commercial plant support systems and a 120-machine cascade that would be incorporated in the full commercial ACP. Initial funding, intended to last through November 2012, will amount to $110 million. DOE will release $87.7 million for the initial phase by taking title to and disposal responsibility for a quantity of depleted uranium tails from USEC; a similar approach was used in March 2012 to provide $44 million in interim funding. Appropriation bills providing FY 2013 (October 2012-September 2013) funding have been approved by the US House of Representatives and the Senate Appropriations Committee, but have not yet been finalized.

The enrichment services that might be expected from these three proposed supply sources rise from less than 1 million SWU in 2015 to 11 million SWU in 2020 and 16 million SWU for the long term.

Market outlook

Base supply is greater than enrichment requirements at present. For 2012, the average annual economically-competitive and physically-usable production capacity that is not constrained by international trade agreements, together with the equivalent enrichment services that are derived from Russian HEU and other sources, is 45 million SWU. However, this is 3 million SWU (8%) more than nuclear power plant operating requirements of 41.5 million SWU. This level of supply excess is consistent with the average of 5% of requirements observed between 2006 and 2010, but well below the 15% supply excess of 2011. Base supply capability is forecast to increase to 61 million SWU per year by 2025 and 69 million SWU per year by 2035.

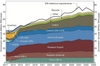

Figure 1 presents ERI’s forecast of uranium enrichment base supply and reference requirements through 2035. In the absence of the enrichment services that could be produced by the three proposed US-based plants, or additional increases in base supply, beginning as early as 2018 supply will not be adequate to meet world requirements.

During the ten-year period 2016-2025, with just base supply under the reference nuclear power growth forecast, world supply is an average of over 1 million SWU per year (2%) short of meeting world average annual requirements. During the subsequent ten-year period, supply is an average of almost 4 million SWU per year (5%) short of meeting world average annual requirements.

It is important to note that the supply shown in Figure 1 assumes that underfeeding will take place at Urenco and AREVA enrichment plants in the future. The underfeeding is assumed to make use of 2-2.5 million SWU per year in the long term.

Also, given the growing uncertainty with regard to the AREVA/EREF and USEC/ACP projects, and the fact that the GEH/GLE project must still receive a construction and operating licence from the NRC, these three proposed sources of enrichment services are not characterized as base supply, and so are not included in Figure 1, to illustrate the impact of their absence on the adequacy of supply in the world market.

Enrichment market activity slowed in 2011, but was still respectable. ERI’s estimate of new commitments executed by end users during 2011 is 39 million SWU, a 17% decline from 2010. Contracting in 2011 was reasonably diversified among the primary suppliers. Note that the wholesale arrangement for the supply of 21 million SWU by Rosatom to USEC is not included.

Each supplier’s regional and world market shares are provided in Table 1. The market shares shown are given as a percentage of total deliveries, including recycle and inventory use by the nuclear power plant operating companies. Note that market shares may include purchases by customers to build inventory, intentionally or otherwise. The sales of Russian HEU-derived enriched uranium product (EUP) under the U.S.-Russian HEU Agreement, which accounted for 14% of the world market in 2011, are included in USEC’s market share. European supplier market shares include 2% from wholesale purchases of Rosatom supply, which are then delivered to their customer base. If the HEU and supplier wholesale sales are directly attributed to Rosatom, then it would be recognized as supplying 41% of world enrichment requirements in 2011. Sales by other producers (for example CNEIC, JNFL, and DOE) fill 6% of total world requirements. Recycle in the form of mixed oxide (MOX) fuel and enriched RepU met about 4% of 2011 world enrichment requirements.

World requirements are essentially fully committed in 2012 and 2013. Uncommitted requirements then rise slowly from 1 million SWU or 2% of world requirements in 2014 to an average of over 2 million SWU (6%) in 2015 to 2017, rising to 9 million SWU (15%) in 2020, and 25 million SWU (39%) in 2025. As implied by these numbers, enrichment service requirements are well covered with many nuclear power plants fully covered through the year 2020.

Trade restrictions continue to be a factor in the enrichment market, but the impact is declining. The Russian Suspension Agreement was amended in February 2008 to allow import of EUP into the USA that is equivalent to 20% of nuclear power plant requirements starting in 2014. Thirteen contracts with US nuclear power plant operators (Ameren, PG&E, Luminant, Exelon, Constellation, Dominion, Northern States Power, First Energy, PSEG and Entergy) valued at over $5.5 billion have been concluded to date, mostly as EUP. Russia will also deliver 21 million SWU to USEC from 2013 through 2022 under a wholesale arrangement announced in early 2011. Russian sales to the EU-15 countries in Europe are expected to continue to be limited to approximately one quarter of requirements, although in some years they may be as high as one third.

Present long-term market prices are believed to provide sufficient stimulus for construction of new centrifuge plant capacity. However, world centrifuge manufacturing capability is expected to remain well in excess of long-term requirements. Incremental expansion at existing sites is lower-cost than building new greenfield capacity, and there is some prospect for the commercial deployment of a new laser-based enrichment technology; these collectively should serve to prevent long-term price increases. Under the ERI reference nuclear power growth requirements forecast, the enrichment services market clearing price is projected to decline modestly over the next year, but remain relatively stable thereafter.

Author Info:

Thomas Meade and Michael Schwartz, Energy Resources International, Inc. 1015 18th St NW, Suite 650, Washington DC 20036 USA. This article was published in the September 2012 issue of Nuclear Engineering International.

Related ArticlesWaiting for a rebound Toward market balanceFilesFigure 1: Enrichment supply adequacy for reference requirements Table 1: 2011 supplier market shares by region