Fuel review: conversion

Toward market balance

1 October 2012The return to balance for the conversion services market was thought to be several years away, with significant oversupply expected to continue through 2013. A shutdown for anticipated safety upgrades at the Metropolis plant in the US may noticeably reduce oversupply in the near term and hasten a return to balance. By Michael Schwartz and Thomas Meade

Just as the primary conversion companies were completing their investments and resolving issues that had been plaguing their operations, including equipment malfunctions, environmental issues and labour disruptions, the industry was confronted with two new events: the Fukushima Daiichi accident and the world economic downturn. Prior to the Fukushima disaster, consensus was slowly evolving that although the availability of secondary supply was able to fill shortfalls, primary conversion capacity was being stressed and the supply margin was very thin with respect to conversion production capacity. Plant interruptions also highlighted the logistical issues associated with transport of conversion services supply, particularly between Europe and North America, which have yet to be fully resolved.

The impact of the Fukushima accident on the spot market for conversion services has been strong. The spot market for conversion services has been highly volatile over the past ten years, marked by rapid price increases and severe declines. Separate market price indicators are reported for the North American and European markets. While the North American market is discussed in detail here, the European market price typically contains a modest premium (currently 4%; down from 7% at the start of 2012) when compared to the North American price.

More recently, the North American conversion services spot market price, based on monthly indicators published by TradeTech LLC, was at a low of $5.00 per kilogram of uranium (kgU) as uranium hexafluoride (UF6) in February 2010, but rose rapidly to $13.00 per kgU by mid-2010. Following the Fukushima accident, a slow but steady decline ensued, bottoming out at about $6.75 per kgU in early 2012.

The North American long-term market price has historically been much less volatile, with the reported term price hovering in a tight range of $11.00 to $12.25 per kgU from January 2005 through mid-2010. Starting in August 2010, the term price steadily increased for over a year, reaching $16.75 in September 2011. The term price has remained unchanged since that time. The labour strike at the Metropolis plant, followed by ConverDyn’s October 2010 announcement regarding its pricing in future contracts, appears to have led to the 46% rise in term market price observed between mid-2010 and mid-2011. It is not apparent that the Fukushima accident has had an impact on the reported term price thus far. It is also interesting to note that two extended shut-downs of the Cameco Port Hope facility between 2007 and 2009 have had virtually no impact on the published long-term market price for conversion services.

With the current spot price trading at a 60% discount to the current long-term price, the large disconnect between the published spot and term market price indicators is striking. The conversion spot price has demonstrated large discounts relative to the long-term price at other times in the past. This behaviour may be due to the small size of the spot market as compared to the term, as well as the predominant use of base price-escalated pricing mechanisms in conversion contracts. In these contracts, the price of future deliveries is calculated from a fixed base price agreed to at contract signing, which is then escalated to the delivery date according to agreed upon indices such as the Gross Domestic Product Implicit Price Deflator.

Requirements

Natural (that is, unenriched) UF6 serves as feed material for the uranium enrichment process to produce the enriched uranium product (EUP)—also referred to as low enriched uranium (LEU)—used to fuel light water reactors (LWRs) that power the majority of commercial nuclear power plants throughout the world. World requirements under the ERI reference nuclear power growth forecast for UF6 conversion services are projected to rise gradually from 56.8 million kgU (that is, 56,800 MTU) in 2011 to 88.9 million kgU by 2035. World requirements for uranium conversion in other forms, primarily for use in pressurized heavy water reactors (PHWR), add another 2.4 to 3.6 million kgU but do not require conversion to UF6.

World requirements for UF6 conversion services under the reference nuclear power growth forecast are projected to increase by about 55% between 2011 and 2035. US annual requirements are projected to remain in a narrow range between 17.5 and 23.0 million kgU through 2035 for the reference forecast. Western European requirements in 2031-2035 are projected to decline 14% from requirements in 2011-2015. However, the projected increases in requirements for UF6 conversion services in the Commonwealth of Independent States (CIS) and Eastern Europe, East Asia and other regions during the 2011 to 2035 period are expected to be 31%, 284% and 520%, respectively. World requirements for UF6 conversion services under the ERI High Nuclear Power Growth forecast climb to 128 million kgU per year by 2035 - an increase of 125% over 2011 requirements. Under the ERI Low forecast, world UF6 conversion services requirements demonstrate modest growth to 64 million kgU by 2020, but then decline to 55 million kgU by 2035, which is 4% below 2011 requirments.

Primary producers

There are four primary commercial suppliers of uranium conversion services. AREVA/Comurhex, located in France; North American suppliers, Cameco Corporation and ConverDyn, located in Canada and the US, respectively; and Rosatom, which operates two conversion plants in Russia. Cameco’s production is also supported by a plant in the United Kingdom. Rosatom does not generally sell conversion services alone, but has for some years been exporting EUP containing equivalent conversion services to Western Europe, the US, and East Asia. The China National Nuclear Corporation also supplies conversion services, but its production is primarily dedicated to internal needs.

AREVA NC’s Malvesi plant produces UF4 and uranium metal. Its Pierrelatte facility produces UF6 from the UF4 produced at Malvesi and from uranyl nitrate (UNH) produced at the La Hague reprocessing plant. While AREVA’s annual UF6 nameplate conversion capacity is approximately 14 million kgU, it announced in 2011 that it would reduce conversion due to the drop in Japanese requirements. Ultimately, it reported producing only 10.5 million kgU during 2011, down from 12.9 kgU during 2010.

Over the last several years, AREVA has been involved in the construction of a new UF6 conversion complex at Malvesi and Pierrelatte, COMURHEX 2. The new complex will be capable of converting 15 million kgU per year. AREVA also has stated that the new complex could ramp up to 21 million kgU per year if warranted by market conditions. The word ‘warranted’ may be interpreted to mean ‘if AREVA can obtain adequate long-term commitments at acceptable long-term prices’. Startup of the new complex is expected either in late 2012 or early 2013.

Approximately half of AREVA’s current commitments are estimated to be in Western Europe, with 33% in the US, 15% in East Asia, and the balance in other regions. It currently holds approximately 21% of the world market. AREVA is one of the three Western companies (along with Cameco and Nukem) that market Russian HEU-derived UF6 under the Russian Commercial Marketing Agreement.

Cameco Corporation produces both UF6 for LWRs and UO2 for PHWRs. Like AREVA, Cameco utilizes the wet solvent extraction process, with some new modifications allowing for recovery of hydrofluoric acid, which substantially reduces the volume of residue generated in UF6 conversion.

Cameco’s Blind River facility in western Ontario produces UO3 from U3O8. The annual licensed capacity of this facility, which replaced an older and smaller facility in 1983, is 18 million kgU as UO3. An application for expansion to 24 million kgU is under evaluation by Canadian regulatory authorities. The UO3 produced at Blind River is transported several hundred kilometres across Ontario to Cameco’s Port Hope conversion facility, which is located about 100 km east of Toronto. The Port Hope conversion facility is licensed for 12.5 million kgU as UF6 per year and 2.8 million kgU as UO2 per year. The UO2 portion of the plant primarily serves CANDU reactors, which are PHWRs.

In 2005, Cameco entered into a ten-year UO3 -to-UF6 toll conversion agreement for 5 million kgU per year from the Springfields Fuels Ltd. facility in the UK. Since March 2006, Cameco has shipped up to 5 million kgU as UO3 per year to Springfields from Blind River. The Canadian and UK facilities together have an annual sustainable capacity of about 15.5 million kgU as UF6. In 2011, the Blind River refinery produced 13.5 million kgU of UO3. Cameco has stated that it does not presently expect to extend the Springfields agreement beyond 2016, but may re-evaluate its decision as market conditions evolve. Cameco has explored potential collaborations in uranium conversion with Kazatomprom; first, consideration of building a uranium conversion facility in Kazakhstan, and later, possible expansion at Springfields. No progress has reportedly been made to date, as market conditions do not appear to support Cameco’s expansion of conversion capacity at present.

Between 2007 and 2009, Cameco’s Port Hope conversion plant was shut down for more than 18 months in total due to the discovery of uranium-bearing effluents leaking into the nearby city harbour, followed by a price dispute with its fluorine supplier. A ten-week planned annual maintenance outage in 2010 reportedly included retraining due to a series of small incidents including a release of UF6. Cameco has made significant capital investments at Port Hope as a result. Production at Port Hope has not yet returned to the levels achieved prior to 2007. Cameco expects production in 2012 to decrease due to unfavourable market conditions.

Approximately half of Cameco’s conversion business is estimated to be in the US, 27% in Europe, 20% in East Asia, and the balance in other regions. Cameco’s present share of the world conversion services business is estimated to be about 24%.

ConverDyn was established by affiliates of General Atomics and Honeywell International Inc. in 1992. ConverDyn is responsible for all marketing and contracting on behalf of Honeywell’s Metropolis conversion plant. Nameplate capacity at Metropolis is 15 million kgU as UF6, while sustainable capacity is closer to 12 million kgU per year.

The Metropolis plant utilizes the dry fluoride volatility process, in which the residual impurities are removed from the UF6 product by fractional distillation as the last step in the conversion process. The dry fluoride volatility conversion process developed by Honeywell and its predecessors delivers a UF6 product with a consistently high 99.99% purity. This unique process is comprised of five main stages: sizing, reduction, hydrofluorination, fluorination and distillation, along with auxiliary processes such as waste treatment and sodium removal.

Over the past decade, the Metropolis plant has been plagued with various labour problems. About 230 United Steelworkers Union (USW) members were on a company-declared ‘lockout’ between 28 June 2010 and 2 August 2011 over safety and seniority issues. During the year of the lockout, Honeywell utilized the Shaw Group to operate and improve the operating process. Following successful conclusion of the labour negotiations, Honeywell slowly transitioned the Shaw workforce out of the Metropolis plant, as they were being replaced with the newly retrained union employees.

Citing cost pressures that were not reflected in prevailing conversion market prices, ConverDyn announced in October 2010 that new contracts would be priced at $15 per kgU or higher, with freight charges for delivery billed separately. ConverDyn stated that production costs had doubled between 2005 and 2010. More recently, Honeywell stated that $70 million in capital investments have been made at the Metropolis plant since 2006. In July 2012, the U.S. Nuclear Regulatory Commission (NRC) completed a regulatory inspection inspired by the Fukushima accident that looked at preparedness for natural disasters such as strong earthquakes and tornadoes (see also article, p. 12). Honeywell subsequently announced that further upgrades to the plant would be required over the next 12 to 15 months as a result. Honeywell has committed to not restarting the plant, which entered a planned annual maintenance in May 2012, until reaching agreement with the NRC on the necessary upgrade projects and timing. The timeline for restart of the Metropolis plant and the cost of the required upgrades will not be known until Honeywell’s discussions with the NRC are completed. Honeywell anticipates that the full-time workforce could be reduced by 50% while the upgrades are being made.

With the improved process and union practices, it is believed that the plant’s annual production should be in the 12 million kgU range once the above-noted upgrades have been completed. However, it is presently unknown whether Metropolis production will increase above this level in the foreseeable future.

ConverDyn’s present share of the world market is estimated to be about 20%. Approximately 46% of ConverDyn’s contract portfolio is estimated to be with US customers. The remainder is primarily with customers in East Asia—estimated at 34% of ConverDyn’s business, and Europe—estimated at 19% of ConverDyn’s business.

Rosatom produces UF6 at conversion plants operated by the Joint Stock Company (JSC) Angarsk Electrolysis Chemical and Combine (AECC) and the Siberian Chemical Combine (SCC) enrichment companies. The SCC conversion plant is located in the city of Seversk in the Tomsk oblast. The Rosatom UF6 plants receive UF4 feedstock from the JSC Chepetsk Mechanical Plant and uranyl nitrate from JSC Novosibirsk, in addition to concentrates from domestic and foreign uranium mining enterprises. SCC also converts reprocessed uranium (RepU) under contract with AREVA. During 2011, Rosatom and TVEL expressed their intention to consolidate UF6 production to only the Seversk site in the future. Plans are to transfer all UF6 conversion activities to Seversk by 2015, which will require a RUR 7.5 billion ($230 million) investment. Public hearings, environmental impact assessments, feasibility studies, investment substantiation and project documentation are ongoing.

While Rosatom’s installed capacity has been routinely reported to be on the order of 25 million kgU per year, current information suggests that for purposes of estimating world conversion capacity, and until Rosatom makes a major capital investment to upgrade and return its older equipment to operational status, that a sustained capacity of 11 million kgU is a more reasonable estimate. Actual production in recent years is estimated to have been about 8.5 million kgU per year. A substantial portion of the ‘conversion services’ that Rosatom delivers is comprised of the natural uranium feed equivalent from downblended HEU.

Because of their design, the Rosatom conversion plants require a very high-purity uranium feed (in terms of trace amounts of other elements and compounds in the concentrates), which is beyond that required by the applicable ASTM specifications. Uranium from Russian and former CIS uranium processing plants meet these quality requirements. Therefore, a major consideration for use of Rosatom conversion capacity may be the availability of high-purity uranium feed.

At present, it is estimated that about 60% of Rosatom’s business is within Eastern Europe and the CIS, and that the balance of its portfolio is distributed fairly uniformly in the US, Western Europe and East Asia. Rosatom’s present share of the world market is estimated to be about 27%.

China National Nuclear Corporation (CNNC) oversees all aspects of the Chinese government’s military and civilian nuclear programmes. It operates a 3.0 million kgU per year (as UF6) conversion plant at the Lanzhou Nuclear Fuel Complex. CNNC conversion capacity is dedicated to meeting domestic requirements, which already exceed current indigenous conversion capacity. While information is limited, CNNC is expected to start expanding its domestic conversion capacity around the year 2015, as domestic conversion requirements are set to increase rapidly. CNNC annual conversion capacity is projected to reach nearly 8 million kgU by 2020 and 16 million kgU by 2030.

Secondary supply sources

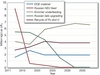

At present there are substantial secondary sources of UF6-equivalent material currently available in the world. These secondary supplies could amount to approximately 24 million kgU per year during 2012 and 2013. Following the conclusion of the US-Russia HEU Agreement in 2013, these supplies are expected to fall to between 15 and 18 million kgU per year during the period 2014 through 2024, and then further decrease to between 12 and 13 million kgU per year by 2026, where they are likely to level off. However, it should be recognized that there are significant uncertainties in these forecasts, since each requires that those who control these secondary supplies continue to take actions that would make this material available to the commercial markets.

These secondary sources do not include the strategic uranium that is being held by owners and operators of nuclear power plants and the commercial suppliers of nuclear fuel materials and services. Release of commercial inventories of conversion services is not expected, although concern remains that Japanese utilities in general, and TEPCO in particular, may decide to do so in the future. Secondary sources include the natural uranium feed and conversion services equivalent of the Russian HEU, DOE HEU and natural uranium, the uranium resulting from underfeeding by the enrichers, plutonium recycle and uranium recycle, and European and Russian tails that could be upgraded in Russia using its surplus enrichment capacity.

As can be seen from Figure 1, supply arising from tails via underfeeding at both Western and Russian enrichment plants, as well as upgrading of Russian stockpiles of tails, comprises a significant portion of conversion secondary supply after 2013.

Additional quantities of relatively high-assay DOE enrichment tails in the form of UF6 could become a source of equivalent conversion services in the future, if economically worth upgrading. Equivalent conversion services arising from the re-enrichment of DOE tails material is included in the DOE secondary supply shown in Figure 1.

Market outlook

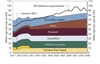

An analysis of the current and future relationship between supply and requirements in the market for conversion services has been performed consistent with the information provided above. Primary production was able to meet approximately 80% of 2011 requirements, and secondary supply, which includes the feed component of Russian HEU, enrichment tails upgrading, and government stockpile draw-down, was more than adequate to meet the remainder of requirements. In fact, total supply, both primary and secondary, exceeded 2011 requirements by 21%.

Figure 2 provides a graphical illustration of the relationship between projected supply and requirements through 2035 for ERI’s reference nuclear power growth forecast. The world’s sustainable primary production capacity is expected to rise from 46 million kgU as UF6 in 2011 up to 58 million kgU in 2015, and then increase gradually to 72 million kgU by 2035. The increase in primary production capacity is largely due to the assumed increase in UF6 production by CNNC to meet a substantial portion of its internal requirements, consistent with the Chinese policy of being largely self-sufficient. As previously discussed, secondary supply, in all forms, together with recycle, is collectively expected to decline between 2014 and 2025 and then stabilize at about 50% of current levels. The requirements for UF6 conversion services are forecast to steadily increase to 89 million kgU by 2035.

The significant oversupply situation that is apparent in Figure 2 is expected to continue through 2013, but does not account for the likely outage at Metropolis.. The near term oversupply of 12 to 13 million kgU will be noticeably reduced if ConverDyn’s production over the next year is significantly curtailed while safety upgrades required by the NRC are implemented. By 2014 the oversupply situation associated with secondary sources is expected to decline, averaging about 6 million kgU between 2014 and 2016. Total primary and secondary supply, including previously-announced plans for facility expansions and an increase in domestic capacity by CNNC, should be able to meet ERI reference forecast requirements through about 2022, although the average annual supply margin relative to world requirements is only about 2 million kgU. However, beginning in 2023 there is a small deficit of supply relative to world requirements that grows to nearly 6 million kgU per year by 2025 and averages 10 million kgU per year between 2028 and 2035.

Note that the supply shown in Figure 2 does not include the potential 6000 MTU expansion of AREVA’s new Comurhex II plant, nor does it include operation of the Springfields conversion plant past 2016. COMURHEX II could be expanded when required by market conditions, which appears to occur shortly after 2020. The decision to extend operation at Springfields is less certain, as supply appears to be adequate, although just barely so, in the years immediately following its currently expected shut down.

Author Info:

Michael Schwartz and Thomas Meade, Energy Resources International, Inc. 1015 18th St NW, Suite 650, Washington DC 20036 USA. This article was published in the September 2012 issue of Nuclear Engineering International.

Related ArticlesWaiting for a rebound Transition almost completeFilesFigure 1: Projected secondary supply of equivalent conversion services Figure 2: Projected conversion services supply and reference nuclear power growth forecast requirements