UK Focus

Not quite carbon-neutral

12 September 2005The UK’s Climate Change Levy could be refocused to give more benefit to the environment – and for nuclear. By Malcolm Grimston

The 1990s were characterised by growing international concern about climate change, and the beginnings of coordinated efforts to reduce emissions of the main gases implicated, notably carbon dioxide. The first major effort in this direction was the Rio Summit (UN Conference on Environment and Development, UNCED) in 1992, at which the developed world pledged not to emit any more carbon dioxide in 2000 than it had in 1990. In the event, this target was missed in practically every developed country (the UK and Germany being the main exceptions, for reasons discussed below). However, in 1997, at the Kyoto Summit on Climate Change, the Kyoto Protocol was concluded, whereby developed nations would be given targets for emissions of a basket of six greenhouse gases (GHGs) – carbon dioxide, methane, nitrous oxide, hydrofluorocarbons, sulphur hexafluoride and perfluorocarbons (PFCs) – in the first ‘compliance period’ of 2008 to 2012, based on a 1990 baseline. Particular national

targets were set depending on factors such as the degree of economic development of the country in question, and it was made possible for developed countries to ‘trade’ carbon dioxide allowances among themselves and to gain credits for helping developing countries to control their emissions. However, developing countries did not have any emission limitation targets of their own. The protocol eventually came into force in February 2005.

The EU signed up to an agreement to reduce GHG emissions by 8% on 1990 levels by the first commitment period. The UK share was a commitment to reduce by 12.5%. In its 1997 election manifesto the incoming Labour government had set itself a target well in excess of this requirement, to reduce carbon dioxide emissions by 20% by the year 2010.

GHG emissions in the UK

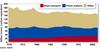

The UK’s emissions of carbon dioxide had been falling through the 1990s. This was mainly a result of the ‘dash for gas’, an artefact of the structure of the newly competitive electricity market which encouraged distribution companies to invest in new gas-fired capacity at the expense of the market share of existing coal-fired plants. The emissions of carbon dioxide per TWh of electricity generated from different fuels are:

• Coal: 955,000t.

• Gas: 446,000t.

• Nuclear: 4000t.

In 1990 coal accounted for 65% of UK electricity production – by 1999 (when total electricity generated was 15% higher) this had fallen to 29%, while gas had grown from practically nothing to 39% . Another factor was improved output from the nuclear power stations, whose market share rose from 20% to 26% owing to the addition of a new station, Sizewell B, and better performance from the advanced gas-cooled reactors.

GHG emissions from electricity production therefore fell significantly. However, the ‘dash for gas’ in effect represented a one-off reduction in emissions – when complete (and in the early years of the 21st century the use of coal actually increased) emissions will begin to rise again unless either a significant proportion of gas is subsequently displaced by nuclear power or by renewables, or reductions in the use of electricity can be achieved.

(The reductions achieved by Germany were a result of the reunification of the country and the subsequent closure of highly inefficient heavy industrial plant in the former GDR. Once again this represents a one-off saving.)

Although new technology can aid reductions in electricity usage, energy efficiency in the absence of a mechanism to increase energy unit costs tends to result in increased economic activity rather than in a pro rata reduction in energy use. (This ‘rebound effect’ of improving energy efficiency was first described in 1865 by Stanley Jevons, who observed that while the introduction of more efficient steam engines initially decreased coal consumption, this then led to a drop in the price of coal. This meant not only that more people could afford coal, but also that coal was now economically viable for new uses, which ultimately greatly increased coal consumption.)

The Climate Change Levy

Attention therefore turned to ways of increasing the price of energy in order to reduce demand and therefore to reduce GHG emissions. However, there were political limitations. The previous Conservative government had introduced Value Added Tax (VAT) on domestic fuel at a rate of 8% in the 1993 budget (to take effect in 1994), with an initial intention to raise it to the standard rate of 17.5% in 1995. This proved unpopular and the second increase was abandoned in the 1994 budget. The Labour manifesto for 1997 pledged to reduce VAT on domestic fuel to 5%. This was duly done but the move made it politically difficult to levy a new tax on domestic energy use under another name.

In March 1998, Lord Marshall was asked to produce a report on economic instruments and the business use of energy. Following the submission of the report in November 1998, the government announced in the 1999 budget its intention to introduce a levy with effect from April 2001. The draft plans underwent a period of consultation, leading to significant revision of the initial proposals and a final draft of the plan being included in the 2000 budget.

The new ‘Climate Change Levy’ (CCL) was imposed on all non-domestic consumers of electricity, with some exclusions such as schools, charities and homes for children, the disabled or the elderly. It was to be collected by the energy supplier on behalf of government. The levy was charged at a flat rate on each kWh of energy consumed, at the following levels:

• Electricity: 0.43p per kWh.

• Natural gas: 0.15p per kWh.

• Coal 1.17p per kg (about 0.15p per kWh).

• Liquefied petroleum gas 0.96p per kg (about 0.07p per kWh).

(Since the conversion of coal to electricity is only about 35% thermally efficient, the rates levied on electricity and on direct use of coal are broadly equivalent.)

Oil products were exempted (as they were already taxed), as were renewable energy, road fuels and ‘good quality’ combined heat and power schemes. Heavily energy-intensive industries could receive a rebate of up to 80% if they agreed to a programme of energy savings.

The levy (expected to raise about £1 billion) was intended to be revenue neutral and was accompanied by a cut in employers’ National Insurance contributions. Some of the proceeds were also made available for research into and promotion of energy efficient technologies. Government estimates suggested that the CCL would result in a decrease in emissions of some 1.5 million tonnes of carbon (5.5 million tonnes of carbon dioxide) per year.

A pollution tax?

The first challenge to the Climate Change Levy is whether it is actually any such thing.

The most efficient way of using taxation to change behaviour or to correct market imperfections is to tax directly the activity which is causing the problem. Here the issue is that carbon dioxide (and other pollutants, including for example the other GHGs and gases connected with acid rain) can be emitted without cost to the companies which produce them, in contravention of the ‘polluter pays’ principle. The costs associated with any damage caused will be picked up by future taxpayers, insurers and so on. The costs of GHG damage are therefore known as ‘externalities’ as far as the companies which create the gases are concerned – in effect these companies are receiving a significant subsidy from future taxpayers or whoever pays the eventual bill.

The most efficient approach would be to tax the emissions of GHGs directly – this is usually (somewhat crudely) referred to as a ‘carbon tax’. Low-carbon and zero-carbon technologies are in competition with reducing energy use as a means of reducing emissions of GHGs. Where it would be more cost effective to reduce emissions of carbon dioxide by switching from coal to nuclear power, say, than to invest in energy efficient technology, a ‘carbon tax’ will ensure that this happens. Therefore whatever resources are made available by society for reducing GHG emissions will have a greater beneficial effect.

The CCL does include an exemption for renewable energy. However, all other forms of electricity production – coal, gas and nuclear – pay the same rate, despite the ratio of their emissions of carbon dioxide (per unit of electricity generated) being roughly 2:1:0 for coal, gas and nuclear. Under the CCL, then, if electricity demand were to reduce to the extent that one power station were redundant, there would be no financial incentive to close a coal station rather than a nuclear station (say), and therefore no incentive to reduce GHG emissions.

A more rational approach, though it might be a little more complex to administer, would be to tax fuels based on their GHG emissions per unit of electricity produced. This would send signals not only to reduce energy use where appropriate (since the average cost of energy would rise) but also to switch fuels where this would be the most cost-effective way of reducing GHG emissions. This approach would be relevant not only when considering new nuclear build but also when decisions are taken about lifetime extension of existing nuclear stations; such extension, with associated savings in carbon dioxide emissions, would be more attractive if the output were not subject to the CCL.

A further difficulty with the CCL is that the elasticity of demand for energy is notoriously low. (For example, the steep increases in pump prices for petrol caused in part by the increase in the oil price in 2004 did not lead to any significant reduction in the number of miles driven.) This is particularly true for electricity: many of its uses are essential and not amenable to switching to alternative fuels. An energy tax such as the CCL, then, may have a relatively limited effect on electricity demand for all but the most intensive users (and perhaps not even there, given that major electricity users tend to be at the forefront of employing technologies to reduce demand, since they gain financially). However, a carbon tax, by encouraging switching to low- or zero-carbon fuels, could deliver significant reductions in emissions even if electricity demand continues to grow at recent modest rates.

Other externalities

Nuclear energy and renewables, however, also involve externalities. Although the costs of waste disposal are largely factored into nuclear energy costs, governments act as the insurer of last resort in case of a major accident. Renewables bring problems such as visual intrusion and disruption of habitat, and there is a major debate about how the costs of retaining back-up plant in a state of ready availability to deal with sudden changes in renewable output should be managed.

One might argue, as some in the environmental movement do, that the externalities associated with nuclear energy, though not connected to climate change, are nevertheless just as great as those associated with use of fossil fuels, and it is therefore appropriate that nuclear energy should also be subject to the CCL. If a rational approach to policy is to be followed this proposition needs to be evaluated.

ExternE, a major EU-funded research study undertaken between 1993 and 2003 undertaken by researchers from all EU member states and the USA to quantify the socio-environmental costs of electricity production, concluded that the cost of producing electricity from coal or oil would double and the cost of electricity production from gas would increase by 30% if external costs such as damage to the environment and to health were taken into account. These figures did not include the potential for climate change-related damage, as these costs are very uncertain at present: had they done so the effect would have been much larger. The report found that nuclear power involved relatively low external costs due to its low GHG emissions and the low probability of accidents in EU power plants. Wind and hydro energy presented the lowest external costs.

Domestic energy use

A further issue associated with the CCL is the exemption for domestic energy users. Under the initial Conservative proposals some of the income from VAT at 17.5% on domestic fuel would have been returned to people in ‘fuel poverty’ through the benefits system, thereby maintaining the incentive for more well-off householders to reduce their energy use where feasible. The domestic sector is an important source of carbon dioxide emissions .

The express exclusion of domestic energy use from the CCL reduces this incentive.

Fiscal neutrality

The effect of the CCL and the associated reduction in National Insurance contributions was to transfer wealth from energy-intensive firms to those employing labour. However, if the levy should be successful in its prime objective of reducing energy use, it would be expected that revenues from the CCL should fall over time. To retain the goal of ‘fiscal neutrality’ presumably the cut in National Insurance contributions would have to be reversed, which could have adverse economic consequences.